|

|

|

|

|||||

|

|

|

Centene Corporation CNC, a leading player in government-sponsored healthcare, finds itself grappling with the same pressures weighing on the broader industry, elevated utilization rates and rising medical costs. Even heavyweights like UnitedHealth Group Incorporated UNH and Elevance Health, Inc. ELV have been forced to trim forecasts as higher expenses eat into profitability.

For Centene, the strain has been pronounced. Membership losses in both Medicaid and Medicare Advantage continue to erode its base. At the same time, operating challenges have pushed the stock’s price down, leaving its valuation below the industry average.

Currently, Centene trades at a forward P/E of 13.25X, undercutting the industry’s 16.16X. Still, the multiple is above its five-year median of 11.24X. In comparison, UnitedHealth trades at 20.19X and Elevance at 10.12X, placing CNC in the middle of the two giants.

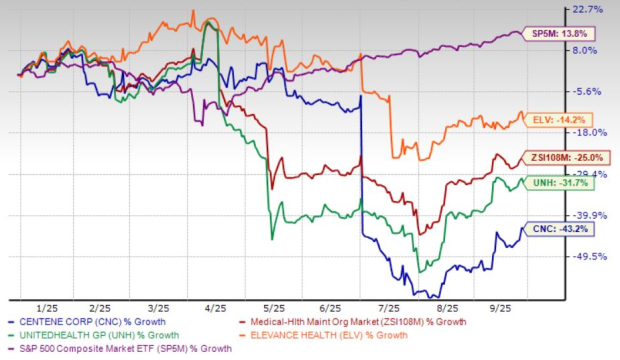

Share price performance, however, tells a harsher story. CNC has tumbled 43.2% year to date, badly trailing not just the industry and the S&P 500, but also UNH and ELV. UnitedHealth is dealing with Justice Department probes into its Medicare billing and Optum Rx operations, while Elevance is restructuring its Medicare business by exiting underperforming markets and pulling out of standalone Part D. Yet Centene’s own challenges have proven more punishing.

Operating expenses climbed 5.5% in 2023, 5.8% in 2024, and then surged 21.1% in the first half of 2025, fueled by mounting medical costs. Its health benefits ratio (HBR) — a key measure of claims payouts — rose from 87.7% in 2023 to 88.3% in 2024, and now stands at 93% as of the second quarter 2025. The higher the ratio, the slimmer the profits left after covering claims.

Margins are under visible stress. Adjusted net margin slipped from 2.3% last year to negative 0.2% in the latest quarter. Management reintroduced 2025 EPS guidance at $1.75, a sharp drop from the previous $7.25 outlook, with a downside risk to $1.25 if trends worsen further.

Meanwhile, commercial membership is growing, but declines in Medicare and traditional Medicaid continue to drag down overall enrollment. Heightened competition will also make securing new contracts tougher in the near term.

Centene’s balance sheet remains debt-heavy, thanks largely to acquisition-driven borrowing. Long-term debt stood at $17.6 billion as of June 30, 2025. On efficiency, the picture is muted: its trailing 12-month return on invested capital of 6.7% trails the industry average of 9%, highlighting less effective capital utilization.

The “One Big Beautiful Bill” has been signed into law, with uncertainty around its eventual impact on healthcare. While subsidy cuts and eligibility verifications could weigh on memberships in government plans, the law can also open the door to expanding Centene’s high-margin commercial footprint.

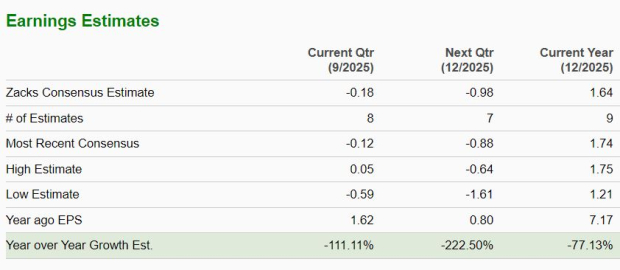

Consensus estimates mirror these headwinds. The Zacks Consensus Estimate for 2025 earnings is currently pegged at $1.64 per share, signaling a 77.1% year-over-year decrease. It witnessed eight downward revisions over the past 60 days and no movement in the opposite direction. On a brighter note, revenues are expected to grow 16.9% in 2025.

Centene does have pockets of strength. Its commercial business is expanding rapidly, with marketplace memberships up 29.4% in the first quarter of 2025 and accelerating to 33.2% in the second quarter. This segment also carries better margins than government-sponsored programs.

CEO Sarah London recently noted that Medicare quality scores, or star ratings, were in line with expectations, with a slightly larger portion of members in four-star plans; a notable development, as these plans qualify for bonus payments.

Looking ahead, regulatory clarity combined with operational improvements could help stabilize performance, unlock value and improve profitability in select areas.

Centene’s lower-than-industry valuation might appear tempting at first glance, but the underlying fundamentals paint a more troubling picture. Escalating medical costs, shrinking Medicaid and Medicare Advantage memberships, margin erosion and a heavy debt continue to weigh heavily on performance. The drastic cut in earnings guidance and a wave of downward analyst revisions underscore the fragile outlook. While commercial membership growth and stable Medicare star ratings provide glimmers of hope, they are not enough to offset the deep operational and financial headwinds in the near term.

Centene currently has a Zacks Rank #5 (Strong Sell), signaling that investors may be better off staying on the sidelines until clearer signs of recovery emerge.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite