|

|

|

|

|||||

|

|

|

Nike NKE will take the spotlight next week, with the iconic apparel leader set to report results for its fiscal first quarter on Tuesday, September 30.

Feeling the high inflationary aftermath that has led to a more cost-conscious consumer, Nike stock has lost considerable mojo in recent years, like other prominent apparel retailers such as Lululemon LULU and Crocs CROX.

However, investor sentiment has started to build again amid Nike’s plan to strategically refocus on product innovation, storytelling marketing campaigns, and wholesale distribution after previously alienating partners like Foot Locker and Macy’s M to build out its direct-to-consumer (DTC) reach.

While NKE has climbed off its 52-week low of $52 a share, Nike stock is still more than 20% from a one-year high of $90.

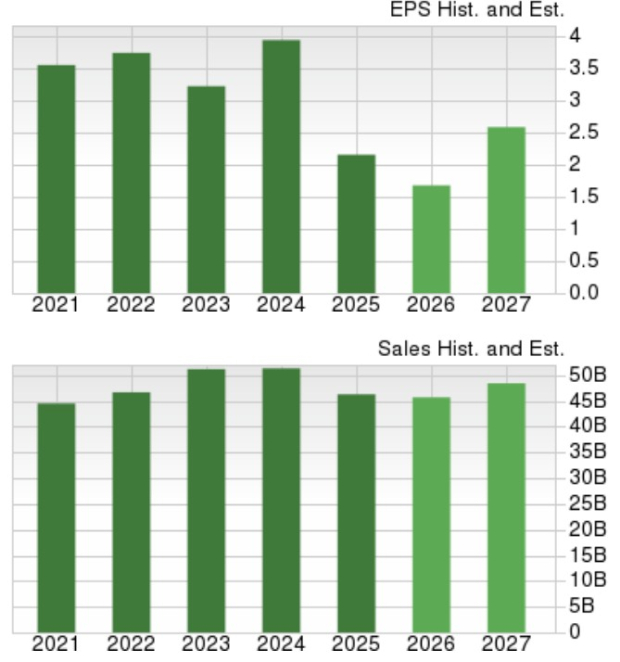

Nike’s Q1 sales are expected to be down 5% to $11 billion versus $11.59 billion in the comparative quarter. That said, a steeper decline is expected on Nike’s bottom line, with Q1 EPS thought to have fallen to $0.28 compared to $0.70 per share a year ago.

Outside of the need to address product innovation, the decline in Nike’s top and bottom line figures is also attributed to tariff headwinds, particularly in China, with quarterly revenue in its Greater China segment projected to drop 14%.

Still, Nike has exceeded the Zacks EPS Consensus for eight consecutive quarters with an impressive average earnings surprise of 41.99% in its last four quarterly reports.

Despite its stronger-than-expected operational performance, Wall Street will be closely monitoring Nike’s guidance and any updates as to how its strategic overhaul will hopefully rectify its downturn.

Making Nike’s outlook more crucial, Lululemon continued an impressive streak of exceeding its quarterly earnings expectations earlier in the month, but saw its stock free-fall to new multi-year lows after slashing its guidance due to tariff impacts.

Fortunately for Nike, the company is better suited to handle tariff headwinds thanks to its supply chain maturity, having a deeper global infrastructure that includes diverse manufacturing from multiple countries outside of China.

Overall, Nike’s total sales are currently slated to dip 1% in its current fiscal 2026 but are projected to rebound and rise 6% in FY27 to $48.41 billion. Nike’s annual earnings are forecasted to drop over 20% in FY26 to $1.68 per share, although FY27 EPS is projected to rebound and spike 58% to $2.59.

Nike’s Q1 report will be critical to what is hopefully a continued rebound in NKE shares, and for now, the apparel leader's stock lands a Zacks Rank #3 (Hold). Undoubtedly, Nike has the brand placement that should eventually reignite its growth, but providing favorable guidance would be reassuring, as NKE is trading at a noticeable premium to the broader market at 41X forward earnings.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 8 hours | |

| 11 hours | |

| 13 hours | |

| 15 hours | |

| 15 hours | |

| 18 hours | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 |

Companies Are Replacing CEOs in Record Numbersand Theyre Getting Younger

LULU

The Wall Street Journal

|

| Feb-15 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite