|

|

|

|

|||||

|

|

|

Payments powerhouse Mastercard Incorporated MA has long commanded a valuation that seems to live in a world of its own, detached from traditional fundamentals yet supported by a consistent narrative of innovation and dominance. For years, that premium made sense as Mastercard doesn’t merely process transactions; it defines how money moves across the digital economies.

With a massive $523.3 billion market cap, Mastercard enjoys significant network effects and a global reach that few can rival. Yet, the payments space is evolving rapidly. Stiff competition from established peers like Visa Inc. V and American Express Company AXP, alongside nimble fintech disruptors, could challenge its pricing power. Even so, Mastercard’s ability to anticipate trends and adapt its technology keeps it relevant. Its push into the stablecoin ecosystem underscores a forward-looking strategy aimed at maintaining leadership in a rapidly shifting financial landscape.

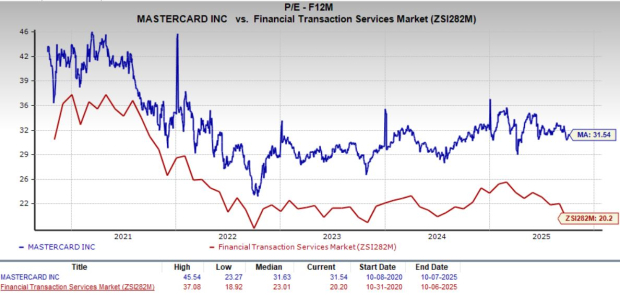

Still, the question remains: are these tailwinds strong enough to justify Mastercard’s lofty price tag? The stock trades at 31.54X forward 12-month earnings, towering above the financial transaction industry average of 20.20X. By comparison, Visa and American Express fetch 27.37X and 19.40X, respectively. Interestingly, Mastercard’s current valuation is only marginally below its five-year median of 31.63X, suggesting the market continues to price in long-term resilience.

At this stage, investors face a choice: double down on Mastercard’s enviable margins and growth potential, or tread cautiously amid emerging risks.

So far in 2025, Mastercard shares are up 10.2%, defying a 3.8% decline across the broader industry. The stock’s resilience underscores investor confidence in its long-term narrative, even though it trails peers Visa and American Express, as well as the S&P 500 Index.

According to The Wall Street Journal, cited in an MSN article, Walmart and Amazon are exploring their own USD-pegged stablecoins, a move aimed at controlling their payment ecosystems and slashing billions in interchange fees traditionally paid to Visa and Mastercard. The passage of the GENIUS Act is expected to put more companies in the race to showcase real-world applications of stablecoins.

Stablecoins promise faster settlements and lower costs, particularly for cross-border transactions, but they fall short in key areas where Mastercard excels, such as fraud protection, credit access and reward programs. These benefits remain essential for both consumers and merchants. Importantly, Mastercard is not standing still. It is integrating stablecoins into its infrastructure through strategic partnerships and technological upgrades.

Alliances with Circle, Paxos, Binance, MetaMask and OKX demonstrate Mastercard’s intent to act as a bridge between traditional finance and the digital asset economy. By positioning itself as the connective tissue between fiat and crypto transactions, Mastercard ensures that even as new forms of money emerge, it remains central to the ecosystem.

Regulatory scrutiny remains one of Mastercard’s biggest overhangs. In June 2025, the London Competition Appeal Tribunal ruled that both Mastercard and Visa’s multilateral interchange fees violated European competition law. The U.K. Payment Systems Regulator is expected to impose fee caps, which could limit revenue growth in the region.

In the United States, the Department of Justice has accused Mastercard and Visa of leveraging their dominance to overcharge merchants. Meanwhile, the proposed Credit Card Competition Act could lead to new routing options, threatening transaction fee margins. Although banks are pushing back against the bill, pressure from lawmakers and regulators is unlikely to ease anytime soon.

Adding to the compliance challenges, Mastercard resolved a workplace pay bias case earlier in 2025, agreeing to conduct internal audits, which is another sign of tightening oversight across its operations.

Despite valuation concerns, Mastercard’s underlying business momentum remains strong. The company continues to deepen relationships with merchants, improve customer engagement, and expand digital offerings. One standout success is the growing adoption of tokenized transactions, which deliver higher approval rates and lower fraud, benefits that strengthen Mastercard’s competitive moat. In the second quarter of 2025, its switched transactions climbed 10% year over year to 43.5 billion, while cross-border volume grew 15%.

A key growth driver is Mastercard’s Value-Added Services business, which has evolved into a powerful diversification engine. Revenues from this segment rose 17.7% in 2023, 16.8% in 2024, and 20% in the first half of 2025, underscoring its rising contribution to overall performance. The company’s acquisition strategy continues to bolster its capabilities in cybersecurity, data analytics and risk management, helping sustain growth beyond traditional payments.

Cash generation remains another hallmark of Mastercard’s strength. The company reported $7 billion in operating cash flow in the first half of 2025, up from $4.8 billion a year earlier. This robust foundation supported $4.8 billion in share buybacks and $1.4 billion in dividends, signaling management’s unwavering confidence in long-term growth prospects.

Analysts seem upbeat about Mastercard’s outlook. The Zacks Consensus Estimate points to 11.8% EPS growth in 2025 and 16.5% in 2026, backed by projected revenue gains of 15.1% and 12.4%, respectively. The stock has seen one upward earnings estimate revision over the past month, against no downward adjustments.

The company has delivered four consecutive earnings beats, averaging a 3.8% surprise, further validating its operational consistency.

Mastercard Incorporated price-consensus-eps-surprise-chart | Mastercard Incorporated Quote

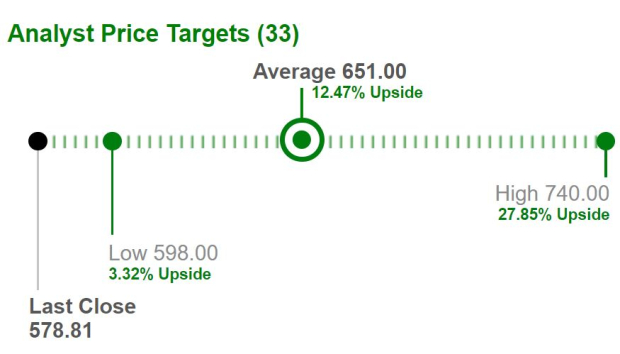

At current levels, Mastercard trades below its average analyst price target of $651, implying roughly 12.5% upside potential. Estimates range from $598 to $740, highlighting a wide spectrum of views but a broadly optimistic consensus.

Mastercard’s consistent growth, strong cash flows, and innovation-driven strategy continue to justify its premium valuation. Despite regulatory risks and rising competition, its expanding digital services and stablecoin initiatives reinforce long-term strength. Backed by steady earnings momentum and positive estimate revisions, Mastercard remains a solid pick for investors seeking quality exposure to digital payments. The stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite