|

|

|

|

|||||

|

|

|

J.B. Hunt Transport Services, Inc. JBHT is scheduled to report third-quarter 2025 results on Oct. 15, after market close.

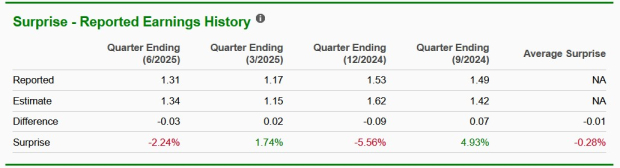

J.B. Hunt’s earnings lagged the Zacks Consensus Estimate in two of the trailing four quarters, the average miss being 0.28%. However, the company outpaced the Zacks Consensus Estimate in the remaining two quarters.

Let’s see how things have shaped up for J.B. Hunt this earnings season.

The Zacks Consensus Estimate for J.B. Hunt’s third-quarter 2025 revenues is pegged at $3.02 billion, indicating a 1.44% decline year over year.

The Zacks Consensus Estimate for the third-quarter Intermodal revenues is pegged at $1.51 billion, indicating a 3.2% decline from the year-ago reported figure. The downside is likely due to a decrease in loads, resulting from changes in customer rates, fuel surcharge revenue and the mix of freight. The consensus mark lies below our estimate of $1.54 billion.

The consensus mark for the Dedicated Contract Services segment revenues is pegged at $858 million, implying a 1.4% increase from the third quarter of 2024 reported number. The upside is likely to have been caused by an increase in productivity (revenue per truck per week).The consensus mark stands below our estimate of $874.2 million.

The Zacks Consensus Estimate for Integrated Capacity Solutions’ revenues is pegged at $271 million, indicating a 2.5% decrease from the year-ago reported figure. Our estimate is pegged at $264.2 million.

The Zacks Consensus Estimate for Truckload revenues is pegged at $175 million, indicating a 1.1% rise from the thirdquarter of 2024 reported number. Truckload revenues are expected to have been aided by an increase inload volume. Our estimate is pegged at $169.6 million.

The Zacks Consensus Estimate for Final Mile Services revenues is pegged at $208 million, indicating a 4.5% decrease from the third quarter of 2024 reported number. General weakness in demand across many of the end markets served might have hurt the segment.Our estimate is pegged at $204.9 million.

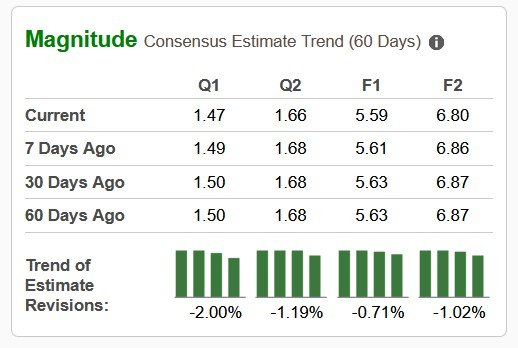

Higher net interest expense is likely to mar J.B. Hunt’s bottom line. JBHT continues to incur higher interest expenses due to higher interest rates. Further, the company’s bottom line might have been hurt by an expected increase in operating expenses due to high purchased transportation costs, salaries, wages and benefit expenses.The Zacks Consensus Estimate for JBHT’s third-quarter 2025 earnings has been revised downward by 2% to $1.47 per share in the past 60 days. The consensus mark implies a decline of 1.34% from the year-ago actual.

Our proven model does not conclusively predict an earnings beat for J.B. Hunt this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. But that’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

J.B. Hunt has an Earnings ESP of -0.12% and a Zacks Rank #4 (Sell) at present.

J.B. Hunt Transport Services, Inc. price-eps-surprise | J.B. Hunt Transport Services, Inc. Quote

J.B. Hunt reported second-quarter 2025 earnings of $1.31 per share, which missed the Zacks Consensus Estimate of $1.34 and declined 0.8% year over year.

Total operating revenues of $2.93 billion missed the Zacks Consensus Estimate of $2.94 billion and were flat year over year. Total operating revenues, excluding fuel surcharge revenue, increased 1% on a year-over-year basis.

Here are a few stocks from the broader Zacks Transportation sector that investors may consider, as our model shows that these have the right combination of elements to beat on earnings this reporting cycle.

United Airlines Holdings, Inc. UAL has an Earnings ESP of +0.47% and a Zacks Rank #3 at present. UAL is scheduled to report third-quarter 2025 results on Oct. 15, after market close. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for third-quarter 2025 earnings has remained stable over the past 60 days. The consensus mark indicates a decline of 20.7% from the third quarter of 2024 actuals.

UAL has an encouraging earnings surprise history, having surpassed the Zacks Consensus Estimate in each of the trailing four quarters. The average beat is 9.3%.

C.H. Robinson Worldwide, Inc. (CHRW)has an Earnings ESP of +0.75% and a Zacks Rank #3 at present. CHRW is scheduled to report third-quarter 2025 results on Oct. 29, after market close.

The Zacks Consensus Estimate for third-quarter 2025 earnings has been revised upward by 0.78% over the past 60 days. The consensus mark indicates growth of 1.56% from the third quarter of 2024 actuals.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 9 hours | |

| 9 hours | |

| 10 hours | |

| 11 hours | |

| 11 hours | |

| 11 hours | |

| 22 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite