|

|

|

|

|||||

|

|

|

Two technology titans, Microsoft MSFT and Apple AAPL, command investor attention with combined market capitalizations exceeding $7.5 trillion. Both companies delivered solid quarterly results in fiscal 2025, yet their trajectories increasingly diverge. The investment question facing mega-cap tech investors is clear: which stock offers superior upside potential as AI reshapes enterprise technology?

Let's delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

Microsoft delivered exceptional fourth-quarter fiscal 2025 results with revenues reaching $76.4 billion, up 18% year over year, demonstrating powerful momentum across its cloud and AI portfolio. CEO Satya Nadella emphasized that "Cloud and AI is the driving force of business transformation across every industry," and the company's execution validates this vision. Azure growth accelerated to 39% in the fourth quarter, significantly exceeding analyst expectations of 34% and substantially outpacing competitors AWS and Google Cloud, which posted 17% and 28% growth, respectively.

The AI monetization story progresses from promise to reality. Microsoft announced that in October 2025, its AI business achieved a $13 billion annual revenue run rate, up 175% year over year, validating billions invested in data center infrastructure. Microsoft 365 Copilot experienced its largest quarter of seat additions since launch, with major enterprises like Barclays deploying to 100,000 employees and UBS expanding to all staff. GitHub Copilot now serves 20 million developers with 90 percent of Fortune 100 companies adopting the platform. Azure AI Foundry processed more than 500 trillion tokens in fiscal 2025, up 7x year over year, with 80% of Fortune 500 companies using the service, demonstrating genuine enterprise adoption moving beyond pilot programs into production workloads.

Microsoft's competitive positioning strengthens when examining its contracted backlog of $368 billion and commercial bookings exceeding $100 billion for the first time. Management guided for double-digit revenue and operating income growth in fiscal 2026, with Azure expected to grow approximately 37%. The company deployed over 2 gigawatts of data center capacity in the past year, operating more than 400 data centers across 70 regions, yet remains capacity-constrained due to robust demand. With operating margins expanding to 45 percent despite quarterly capital expenditure exceeding $30 billion, Microsoft demonstrates exceptional ability to balance growth with operational discipline.

The Zacks Consensus Estimate for Microsoft’s first-quarter fiscal 2026 earnings has remained steady at $3.65 per share over the past 30 days, indicating 10.61% growth from the figure reported in the year-ago quarter.

Microsoft Corporation price-consensus-chart | Microsoft Corporation Quote

Apple delivered strong third-quarter fiscal 2025 results with revenues reaching $94 billion, representing 10% year-over-year growth and a June quarter record. iPhone revenues climbed 13% to $44.6 billion as the iPhone 16 lineup drove upgrade demand. Services achieved an all-time high of $27.4 billion, up 13%, with paid subscriptions surpassing 1 billion users. Mac revenues increased 15% to $8 billion, powered by M4 MacBook Air momentum. Active device installations hit new records across all categories and regions, reflecting robust customer loyalty.

Apple's balance sheet remains exceptionally strong. The company generated $27.9 billion in operating cash flow and returned $27 billion to shareholders via dividends and buybacks. With $133 billion in cash and marketable securities, Apple retains substantial financial flexibility. Services’ gross margins of 75.6% provide valuable recurring revenues offsetting lower-margin hardware. Greater China revenues grew 4% to $15.37 billion after previous declines, supported by government subsidies, though geopolitical risks persist.

Apple Intelligence continues its phased rollout. October 2025 saw the M5 chip launch with 4x the AI performance of M4, integrated into MacBook Pro, iPad Pro, and Vision Pro. The Foundation Models framework enables developers to leverage on-device AI, while iOS 26 introduces over 20 Apple Intelligence features, including Live Translation. However, the platform remains in beta with staggered releases and is unavailable in mainland China.

Challenges cloud the outlook. Management projects mid-to-high single-digit revenue growth next quarter, decelerating from recent trends. Tariffs will cost approximately $1.1 billion in September, pressuring margins. Despite diversifying to India, production concentration in China creates supply chain vulnerabilities. Capital expenditure approaches $12 billion annually for AI infrastructure, yet monetization strategies beyond hardware remain unclear.

The Zacks Consensus Estimate for Apple’s fourth-quarter fiscal 2025 earnings has decreased by 1.1% to $1.74 per share over the past 30 days, indicating 6.1% growth from the figure reported in the year-ago quarter.

Apple Inc. price-consensus-chart | Apple Inc. Quote

Both Microsoft and Apple trade at premium valuations relative to historical averages, with trailing P/E ratios of approximately 37.95 and 36.19, respectively. However, Microsoft's premium appears more justified given superior growth fundamentals and clearer AI monetization pathways. Microsoft's AI business represents a tangible $13 billion revenue stream compared to Apple's nascent Apple Intelligence platform, still searching for direct monetization. Microsoft's forward P/E ratio of 33.3 suggests stronger earnings growth expectations than Apple's forward P/E of 32, despite Microsoft demonstrating higher revenue growth rates. Microsoft's contracted backlog provides revenue visibility that Apple lacks, reducing execution risk.

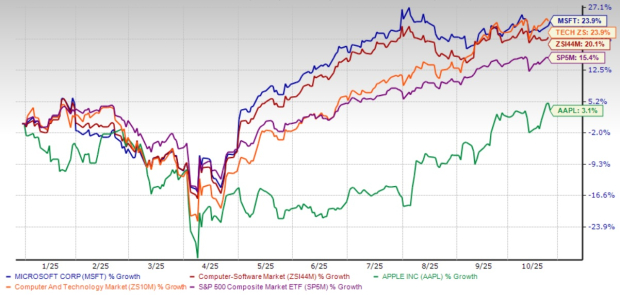

Year-to-date 2025 performance diverges sharply. Microsoft stock advanced 23.9%, reflecting investor recognition that AI infrastructure providers command premium valuations justified by accelerating growth. Conversely, Apple stock hit an all-time high on Monday at $260.2, driven by robust iPhone 17 sales in the United States and China. The tech giant’s market capitalization now stands at an impressive $3.85 trillion. Apple shares have returned 3.1% year to date.

Microsoft presents a more compelling investment opportunity than Apple for growth-oriented investors seeking exposure to artificial intelligence and cloud computing. Microsoft's 39% Azure growth, $368 billion contracted backlog, rapidly scaling $13 billion AI business, and clear enterprise adoption across Copilot products demonstrate superior execution in the AI era. The company's platform approach creates durable competitive advantages, while operating margin expansion proves that management can profitably scale investments. Apple, while demonstrating resilience through Services growth and loyal customers, faces decelerating growth, significant tariff headwinds, AI features still in beta, and limited visibility into AI revenue generation. Investors should buy Microsoft stock given its exceptional growth trajectory and AI leadership, while holding Apple stock or waiting for a better entry point as the company navigates its transition to an AI-driven future. Microsoft carries a Zacks Rank #2 (Buy), while Apple carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 | |

| Apr-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite