|

|

|

|

|||||

|

|

|

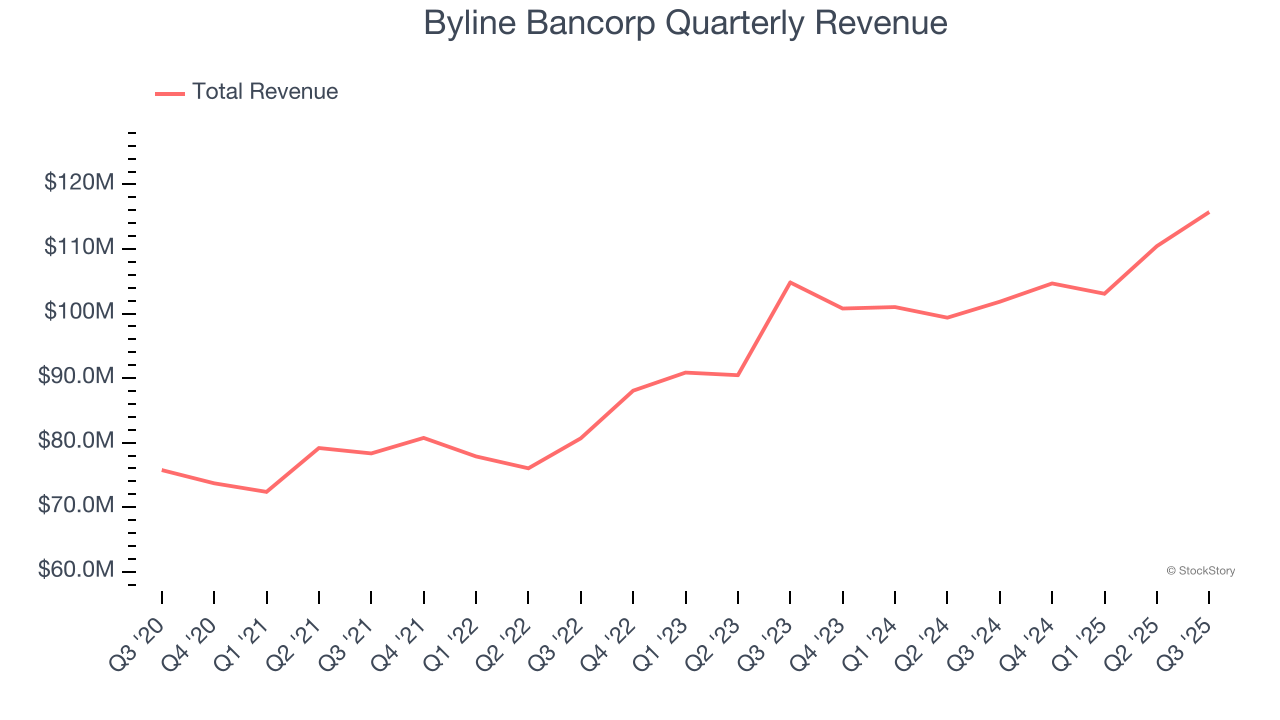

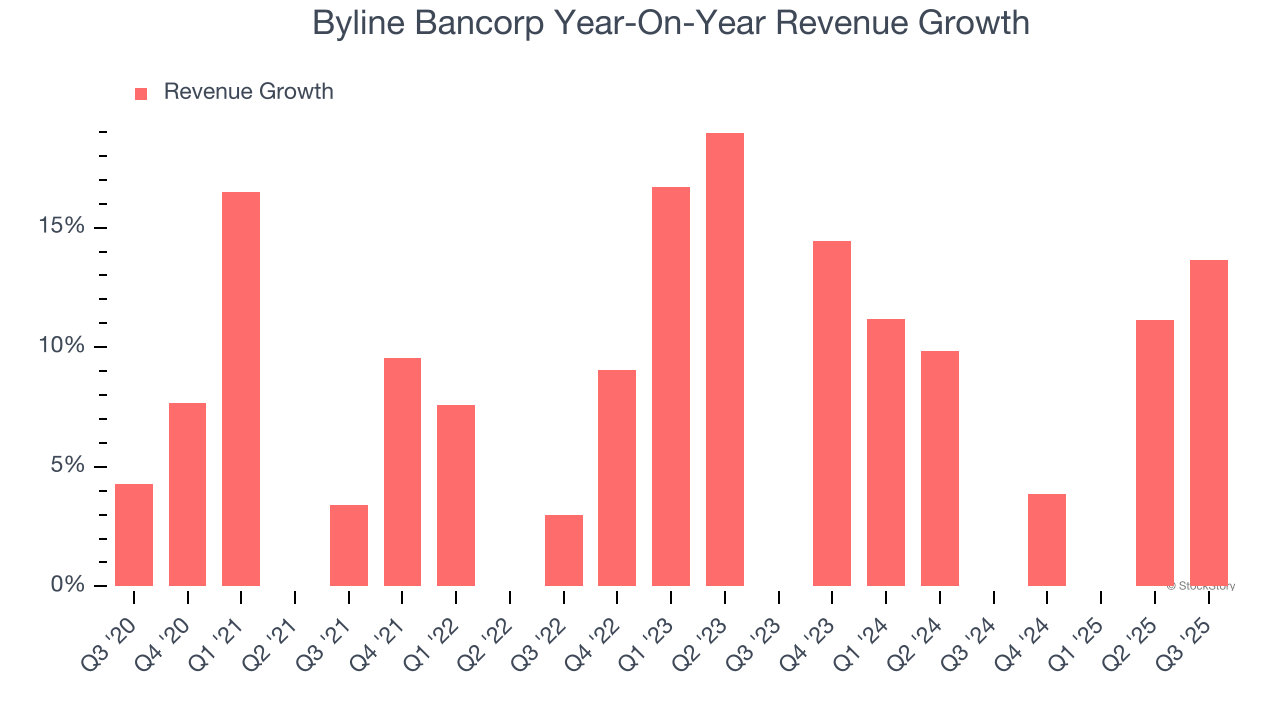

Regional banking company Byline Bancorp (NYSE:BY) announced better-than-expected revenue in Q3 CY2025, with sales up 13.6% year on year to $115.7 million. Its non-GAAP profit of $0.83 per share was 15.3% above analysts’ consensus estimates.

Is now the time to buy Byline Bancorp? Find out by accessing our full research report, it’s free for active Edge members.

Roberto R. Herencia, Executive Chairman and CEO of Byline Bancorp, commented, "Building on the momentum of a strong second quarter, we are pleased to deliver record financial results this quarter as a public company, reflecting the underlying strength of our business. We continue to execute well on our strategic plans and remain focused on becoming the preeminent commercial bank in Chicago. "

Ranking as the fifth most active Small Business Administration lender in the country, Byline Bancorp (NYSE:BY) is a Chicago-based bank that provides banking services to small and medium-sized businesses, commercial real estate developers, and consumers.

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Luckily, Byline Bancorp’s revenue grew at an impressive 9.8% compounded annual growth rate over the last five years. Its growth beat the average banking company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Byline Bancorp’s annualized revenue growth of 7.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Byline Bancorp reported year-on-year revenue growth of 13.6%, and its $115.7 million of revenue exceeded Wall Street’s estimates by 4.5%.

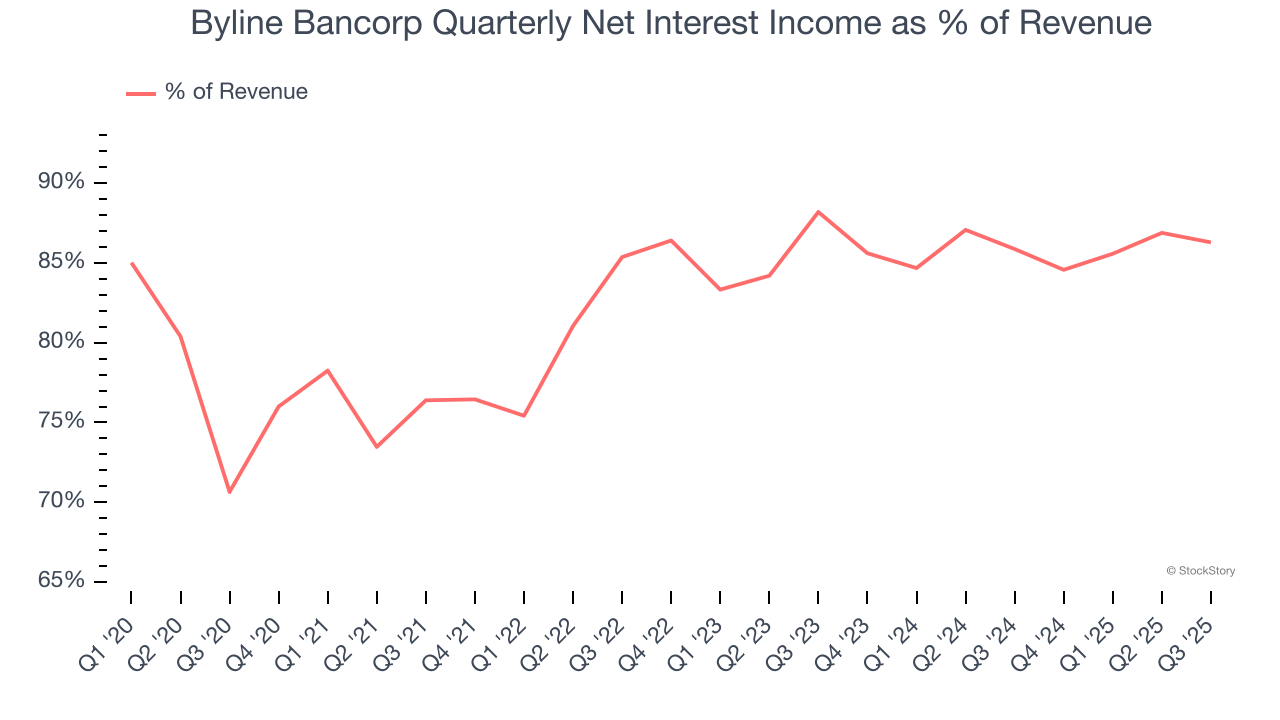

Net interest income made up 82.6% of the company’s total revenue during the last five years, meaning Byline Bancorp barely relies on non-interest income to drive its overall growth.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

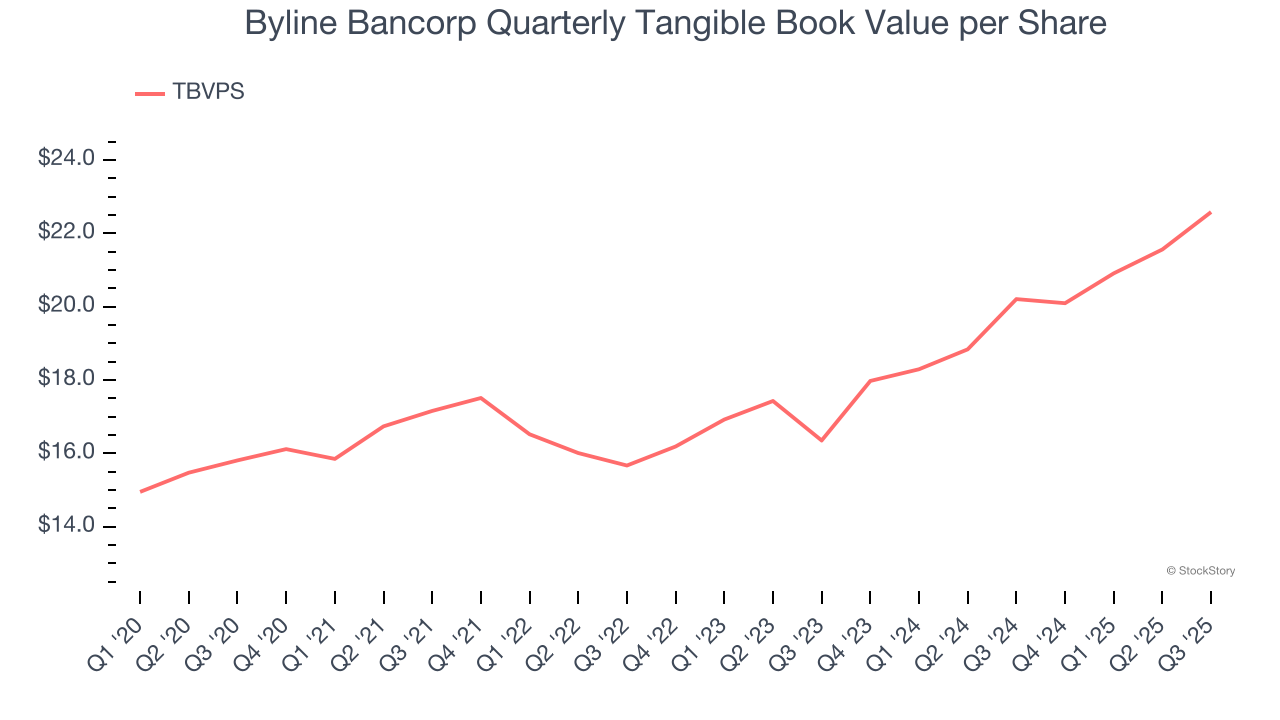

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

Byline Bancorp’s TBVPS grew at an impressive 7.4% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 17.5% annually over the last two years from $16.35 to $22.58 per share.

Over the next 12 months, Consensus estimates call for Byline Bancorp’s TBVPS to grow by 10.2% to $24.88, solid growth rate.

We enjoyed seeing Byline Bancorp beat analysts’ revenue expectations this quarter. We were also glad its net interest income outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $26.65 immediately following the results.

So should you invest in Byline Bancorp right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jul-09 | |

| Apr-25 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-07 | |

| Apr-03 | |

| Feb-25 | |

| Feb-11 | |

| Feb-09 | |

| Feb-03 | |

| Jan-29 | |

| Jan-28 | |

| Jan-26 | |

| Jan-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite