|

|

|

|

|||||

|

|

|

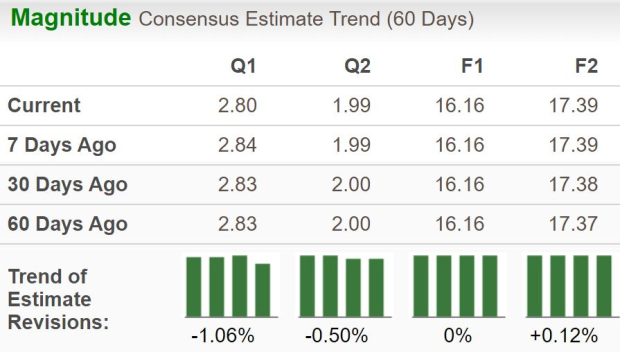

UnitedHealth Group Incorporated UNH is set to report third-quarter 2025 results on Oct. 28, 2025, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $2.80 per shareon revenues of $113.38 billion.

Third-quarter earnings estimates have declined by 4 cents over the past week. The bottom-line projection indicates a decrease of 60.8% from the year-ago reported number. However, the Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 12.5%.

For the current year, the Zacks Consensus Estimate for UnitedHealth’s revenues is pegged at $448.46 billion, implying a rise of 12% year over year. However, the consensus mark for current-year earnings per share is pegged at $16.16, implying a plunge of 41.6% on a year-over-year basis.

UnitedHealthbeat the consensus estimate for earnings in two of the last four quarters and missed twice, with the average surprise being negative 3.3%. This is depicted in the figure below.

UnitedHealth Group Incorporated price-eps-surprise | UnitedHealth Group Incorporated Quote

Our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat, but that’s not the case here.

UNH has an Earnings ESP of -0.81% and a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for premium revenues for the third quarter indicates 15.1% year-over-year growth, whereas our model estimate suggests a 14.1% increase. Higher contributions from the UnitedHealthcare division are expected to have supported premium growth.

The Zacks Consensus Estimate for UnitedHealthcare’s total domestic commercial customers suggests 0.9% year-over-year growth, whereas our estimate implies a 0.5% gain. The consensus mark for Medicare Advantage members indicates an 8% year-over-year rise. The consensus estimate for Medicaid memberships implies a 1.9% increase from the year-ago level. These are likely to have pushed total memberships up from the year-ago period. The consensus estimate implies 1.2% growth year over year.

UNH's third-quarter top-line performance is expected to have been enhanced by a rise in service revenues from the Optum brand. The consensus estimate implies a 3.1% jump in total service revenues. Similarly, the Zacks Consensus Estimate for product revenues indicates a 9.4% increase.

However, rising medical costs, as utilization continues to grow,are expected to have elevated UnitedHealth’s overall expenses in the quarter. This is expected to have affected margins, making an earnings beat uncertain this time around. Our model estimate for total operating costs indicates an 18% increase from the prior-year period.

The Zacks Consensus Estimate for UNH’s medical care ratio is pegged at 90.82%, up from 85.2% in the year-ago quarter. Our estimates for medical costs and costs of products soldindicate 22% and 9.6% year-over-year increases, respectively.

The Zacks Consensus Estimate for operating income from the Optum business segment suggests a 35.6% year-over-year decrease. Meanwhile, the Zacks Consensus Estimate for operating income from UnitedHealthcare indicates a 65.8% year-over-year decline.

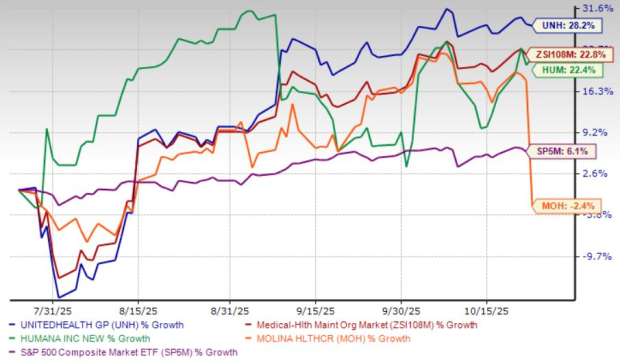

UnitedHealth's stock has gained 28.2% in the past three months compared with the industry’s growth of 22.8%. Its peers, such as Humana Inc. HUM and Molina Healthcare, Inc. MOH, have increased 22.4% and decreased 2.4%, respectively, during this time. UNH has outperformed the S&P 500 significantly, which has grown only 6.1% during the same period.

Now, let’s look at the value UnitedHealth offers investors at current levels.

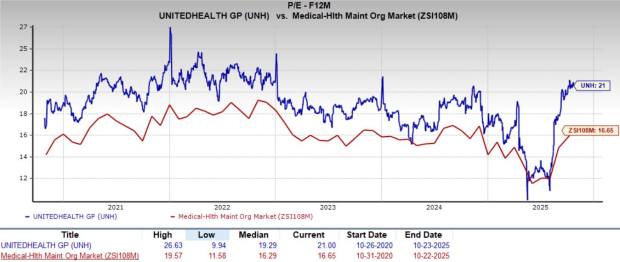

UNH is trading at 21X forward 12-month earnings, above the industry’s average of 16.65X. In comparison, Humana and Molina Healthcare are currently trading at 20.56X and 8.26X, respectively. The premium reflects investor confidence in UnitedHealth’s long-term stability.

Although UnitedHealth is facing margin pressure and higher utilization trends, its long-term fundamentals remain firmly intact. The company’s scale, diversified portfolio across insurance and healthcare services, and strategic positioning within the managed care industry continue to provide a strong competitive moat. Recent volatility appears driven more by near-term cost headwinds and regulatory scrutiny than by any deterioration in its core business strength.

Management’s proactive approach, including selective plan exits, disciplined cost control and operational optimization within Optum, reflects an intent to protect profitability and maintain financial flexibility. Its continued commitment to shareholder returns and long-term earnings growth underscores confidence in the company’s trajectory. Moreover, improving sentiment following renewed institutional interest and strategic acquisitions suggests a gradual recovery in investor confidence.

While short-term challenges could limit earnings momentum, UnitedHealth’s resilience, balance sheet strength and diversified business make it well positioned to navigate the current environment. With strong execution, pricing discipline and expanding memberships, the stock offers a compelling opportunity for investors seeking steady growth and stability. Therefore, adding UnitedHealth to your portfolio at this stage appears to be a prudent move.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite