|

|

|

|

|||||

|

|

|

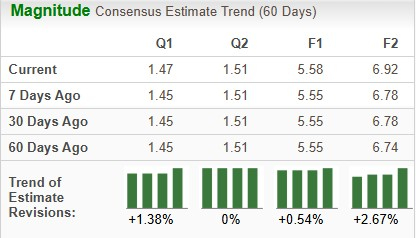

Celestica, Inc. CLS is scheduled to report third-quarter 2025 earnings on Oct. 27. The Zacks Consensus Estimate for sales and earnings is pegged at $3.02 billion and $1.47 per share, respectively. Earnings estimates for CLS have moved up 0.54% for 2025 and have increased 2.67% for 2026, over the past 60 days.

The leading electronics manufacturing services firm has had a solid earnings surprise history in the trailing four quarters, exceeding earnings expectations on most occasions. It delivered a four-quarter earnings surprise of 7.71%, on average.

Our proven model predicts a likely earnings beat for Celestica for the third quarter. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the chances of an earnings beat. That is exactly the case here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Celestica currently has an ESP of +2.49% with a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

During the quarter, Celestica introduced SC6110, a next-generation 2U dual-node, all-flash storage controller, engineered to support mission-critical enterprise applications like AI infrastructure, high-performance computing, core business applications, such as database, online transaction processing, and file sharing. Powered by EPYC Embedded 9004 Series from Advanced Micro Devices AMD, the solution delivers remarkable performance, efficiency, and optimizes energy usage while supporting highly demanding enterprise workloads. The company’s SC6100 storage controllers, powered by AMD processors, have also gained market traction.

As modern IT infrastructure becomes more complex with high-density IoT deployments, cloud application companies across industries are looking for ways to optimize their capital and operational expenditure. With high-speed, scalable ports and compact design, Celestica’s Enterprise access switches are benefiting from these market dynamics.

In the quarter under review, the company is expected to witness solid net sales growth from the Enterprise end market of the Connectivity & Cloud Solutions segment. One of its large hyperscaler customers is set to begin mass production. The company is also set to benefit from the growing demand for 400G and 800G switches.

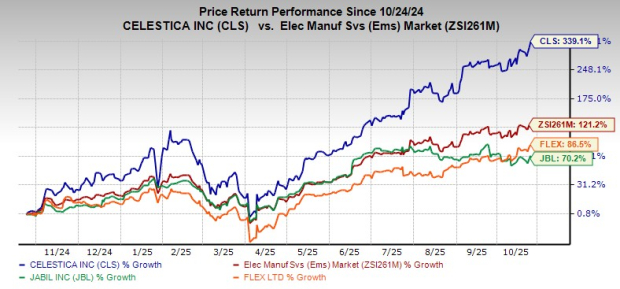

Over the past year, CLS has surged 339.1% compared with the industry’s growth of 121.2%. It has also outperformed its peers like Flex Ltd. FLEX and Jabil Inc. JBL over this period. Flex has gained 86.5% and Jabil is up 70.2% over this period.

From a valuation standpoint, Celestica appears to be trading at a premium relative to the industry and is trading above its mean. Going by the price/earnings ratio, the company’s shares currently trade at 43.18 forward earnings, higher than 25.87 for the industry and the stock’s mean of 24.93.

Several industries, such as healthcare, finance, retail, automotive and aerospace, are rapidly incorporating high data-intensive AI applications. Growing complexity in AI workloads is driving demand for power-efficient and highly scalable hardware solutions that can seamlessly support AI innovation and deployment. Celestica is steadily expanding its offering through innovation and strategic collaboration with industry leaders like AMD and Broadcom to gain from this emerging market trend. Demand in Enterprise, Communication and across its hyperscale portfolio remains strong.

Geopolitical volatility and tariff-related uncertainties have become a major obstacle for the supply chain worldwide. With a presence across 16 countries worldwide, Celestica’s diversified manufacturing network and resilient supply chain are paying off well to mitigate the effects of these factors. A robust inventory management is also a core component of CLS’ supply chain resilience. Efficiency in working management, flexibility and scalability in operations are major advantages. These factors have boosted its reliability among its customers.

Celestica’s strong revenue growth, combined with a stable cash cycle, indicates that cash is not held up unduly in excess inventory. Disciplined capital management, focus on margin expansion and healthy demand across segments are expected to drive free cash flow. These factors allows it to maintain its competitive edge in the electronics manufacturing services industry which consists of major players like Jabil and Flex.

With its comprehensive portfolio offerings, it is expected to gain from strong demand for networking products and growing AI-driven data center investments across industries. Robust supply chain network, efficient inventory management and strong cash flow growth are major tailwinds. Upward estimate revision underscores investors’ positive perception of the stock’s growth potential. With a Zacks Rank #2 and strong price performance, Celestica appears to be primed for further stock price appreciation.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite