|

|

|

|

|||||

|

|

|

ServiceNow NOW is scheduled to release its third-quarter 2025 results on Oct. 29.

The Zacks Consensus Estimate for third-quarter revenues is currently pegged at $3.35 billion, indicating 19.8% growth from the figure reported in the year-ago quarter.

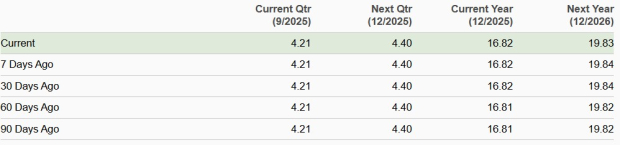

The consensus mark for earnings is pegged at $4.21 per share, unchanged over the past 30 days and indicates growth of 13.2% from the figure reported in the year-ago quarter.

ServiceNow’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 8.04%.

ServiceNow, Inc. price-eps-surprise | ServiceNow, Inc. Quote

Let’s see how things are shaping up prior to this announcement.

ServiceNow expects third-quarter 2025 subscription revenues between $3.26 billion and $3.265 billion, suggesting year-over-year growth in the range of 20%-20.5% on a GAAP basis on 19.5% on a constant currency basis. The Zacks Consensus Estimate for third-quarter 2025 subscription revenues is pegged at $3.03 billion, indicating 20.2% year-over-year growth.

NOW’s workflows are gaining traction. In the second quarter of 2025, technology workflows won 40 deals worth over $1 million, including four over $5 million. ITSM, ITOM, ITAM, security and risk were all in at least 15 of the top 20 deals. CRM and industry workflows were in 17 of NOW’s top 20 deals, with 17 of those deals over $1 million. Core business workflows were in 16 of the top 20 deals, with seven deals over $1 million. The trend is expected to have continued in the to-be-reported quarter.

NOW ended the reported quarter with 528 customers generating more than $5 million in ACV. The number of customers contributing $20 million or more increased by more than 30% year over year. ServiceNow closed 89 deals greater than $1 million in net new ACV in the reported quarter, including 11 deals over $5 million. NOW’s have been benefiting from strong platform adoption, a trend that is expected to have continued in the fiscal third quarter.

However, NOW shares have suffered from a worsening macroeconomic environment due to higher tariffs and trade uncertainty. Slowing growth prospects in the U.S. public domain have been a headwind for ServiceNow.

NOW shares have dropped 12.2% year to date (YTD), outperforming the Zacks Computer & Technology sector’s return of 25.9%. However, ServiceNow shares have outperformed the Zacks Computers – IT Services industry, which has declined 13% YTD.

ServiceNow’s Value Score of F suggests a stretched valuation at this moment.

In terms of the forward 12-month price/sales (P/S), NOW is trading at 12.79X, higher than the sector’s 7.05X.

ServiceNow is extensively leveraging AI and machine learning technologies to boost the potency of its solutions. The latest Zurich platform promises rapid AI adoption through the combination of multi-agentic AI development, enterprise-grade security and autonomous workflows. The launch of AI agents in ServiceNow’s Security and Risk solutions transforms enterprise security by enabling self-defending systems, improving response times and enhancing risk management in collaboration with Microsoft MSFT and Cisco.

A rich partner base that includes the likes of Alphabet, Amazon AMZN, Microsoft and NVIDIA NVDA is noteworthy. NOW has partnered with Amazon’s cloud computing arm, Amazon Web Services, to launch a bi-directional data integration solution, enabling enterprises to unify data and trigger AI-powered workflows by connecting ServiceNow with Amazon Redshift.

NVIDIA and NOW collaborated to launch AI agents for the telecom industry. The AI agents were built with NVIDIA AI Enterprise software and the AI platform NVIDIA DGX Cloud. ServiceNow has expanded its partnership with NVIDIA to enhance agentic AI by integrating NVIDIA Llama Nemotron reasoning models and AI agent evaluation tools into the ServiceNow Platform for optimized business transformation.

Acquisitions have also played an important role in expanding NOW’s portfolio. In April 2025, ServiceNow announced the acquisition of Logik.ai, a company specializing in AI-powered and Configure, Price, Quote solutions. This move is set to bolster ServiceNow’s CRM offerings, particularly in sales and order management, by integrating advanced AI capabilities. The Moveworks acquisition combines ServiceNow’s agentic AI and automation strengths with Moveworks’ front-end AI assistant and enterprise search technology.

ServiceNow’s strong portfolio and rich partner base are expected to drive its subscription revenues in the long term. However, macroeconomic headwind is a major concern along with a stretched valuation.

ServiceNow currently has a Zacks Rank #3 (Hold), which implies investors should wait for a favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 41 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 5 hours | |

| 5 hours | |

| 7 hours | |

| 7 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite