|

|

|

|

|||||

|

|

|

What a fantastic six months it’s been for IonQ. Shares of the company have skyrocketed 123%, hitting $63.95. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy IONQ? Find out in our full research report, it’s free for active Edge members.

Founded by quantum physics pioneers from the University of Maryland and Duke University in 2015, IonQ (NYSE:IONQ) develops quantum computers that process information using trapped ions to solve complex computational problems beyond the capabilities of traditional computers.

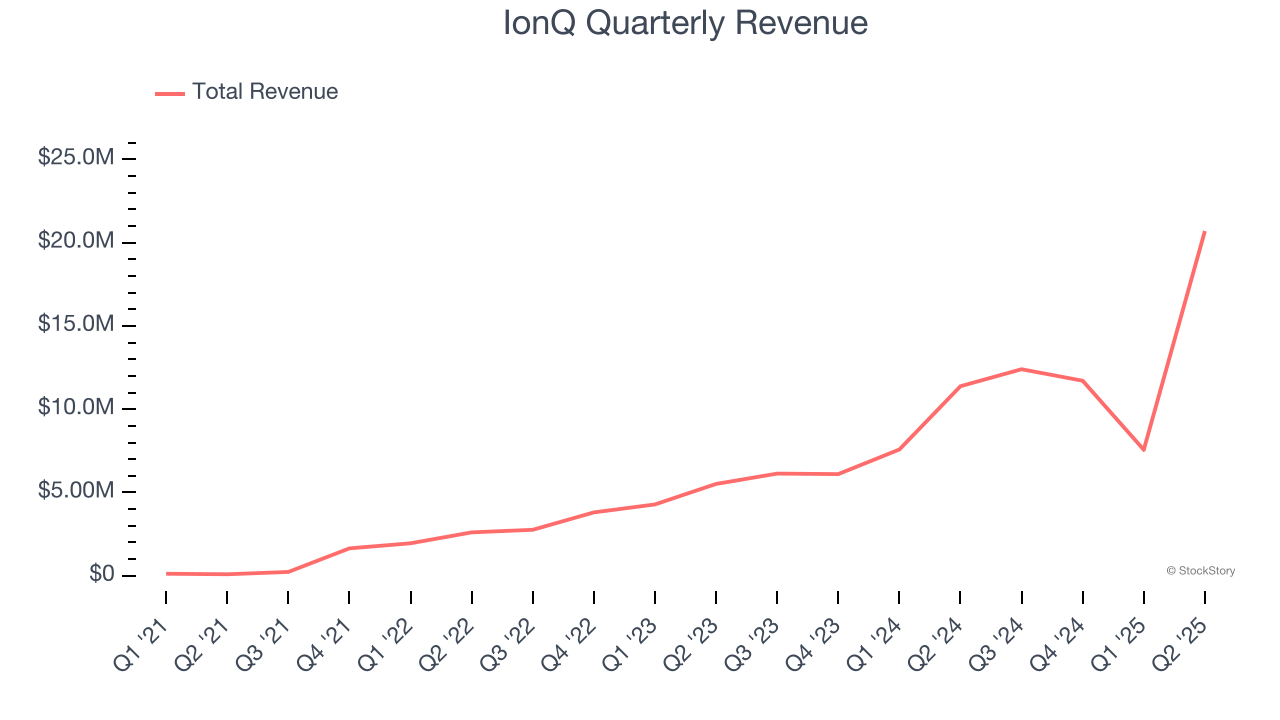

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, IonQ’s sales grew at an incredible 237% compounded annual growth rate over the last four years. Its growth beat the average business services company and shows its offerings resonate with customers.

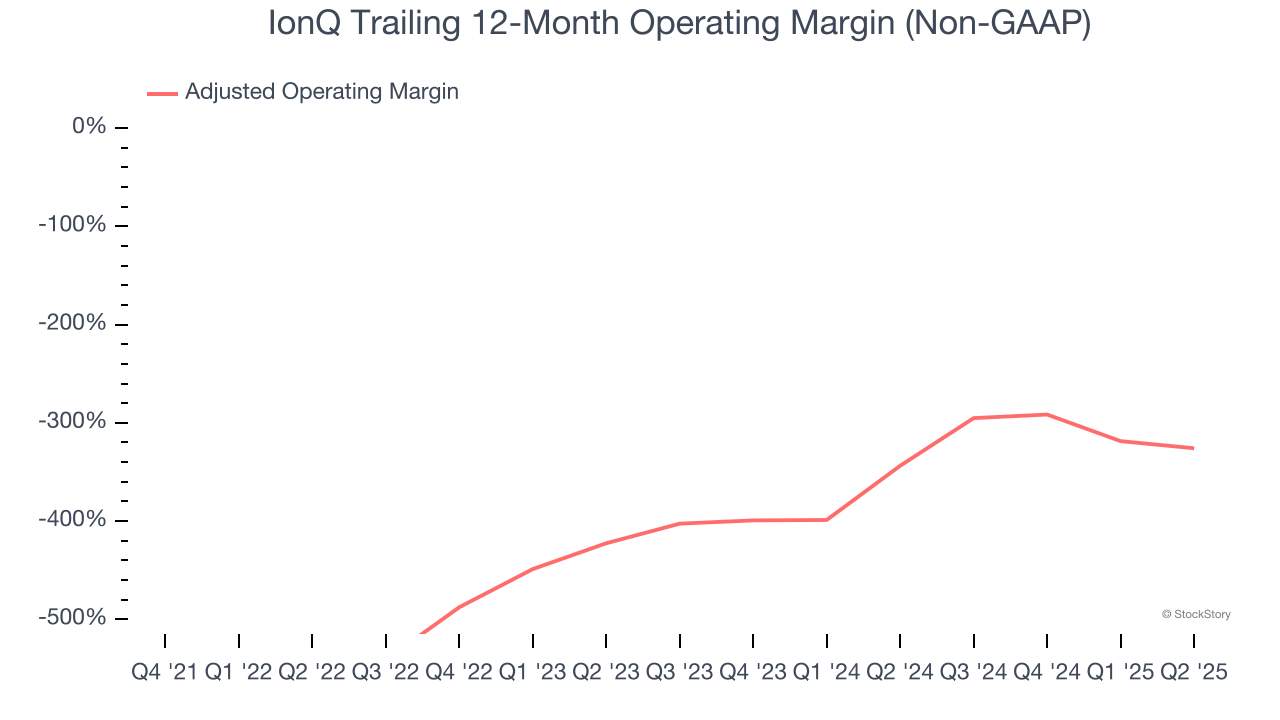

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

IonQ’s adjusted operating margin rose over the last five years, as its sales growth gave it operating leverage. Although its adjusted operating margin for the trailing 12 months was negative 326%, we’re confident it can one day reach sustainable profitability.

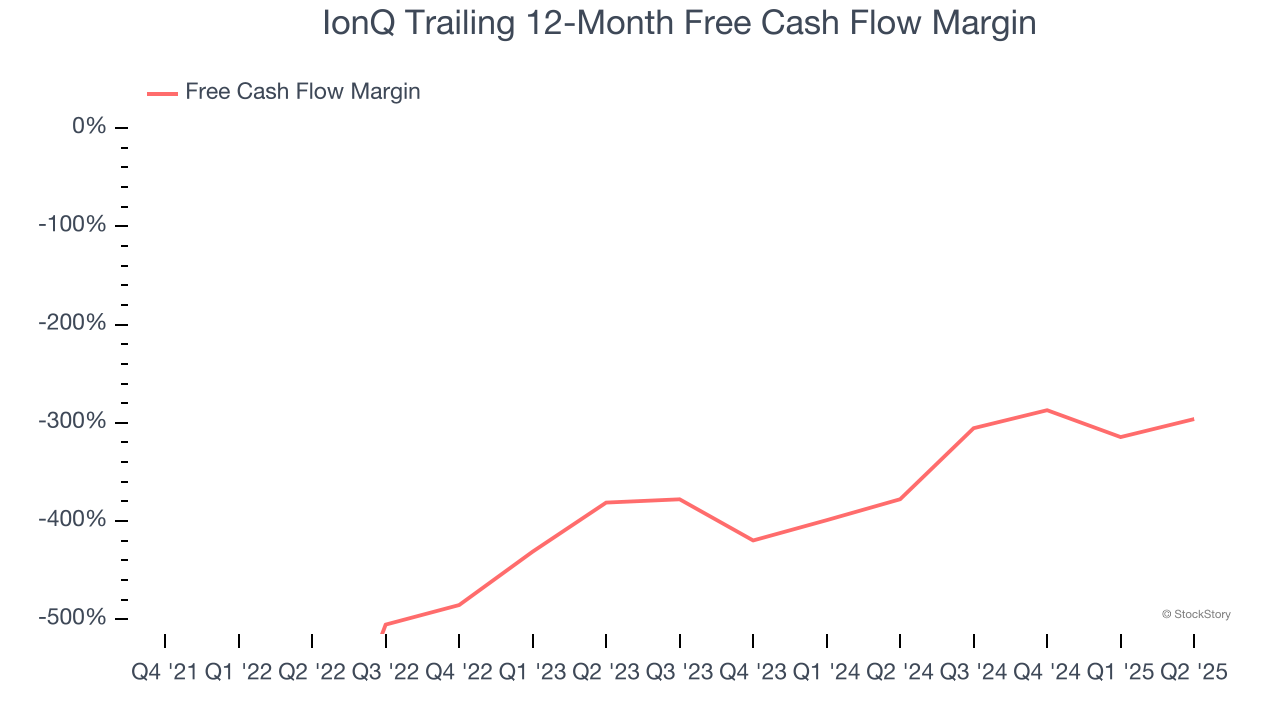

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

IonQ’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 369%, meaning it lit $369.25 of cash on fire for every $100 in revenue.

IonQ has huge potential even though it has some open questions, and after the recent surge, the stock trades at $63.95 per share (or a forward price-to-sales ratio of 117.4×). Is now the time to buy despite the apparent froth? See for yourself in our full research report, it’s free for active Edge members.

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 9 hours | |

| 11 hours | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 | |

| Feb-26 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite