|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

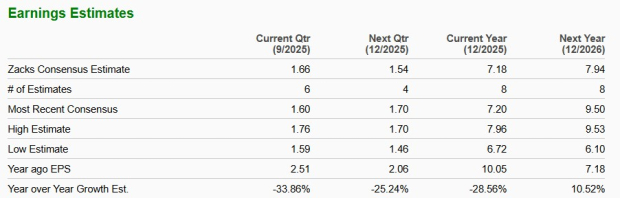

Chevron Corporation (CVX) is slated to release third-quarter 2025 results on Oct. 31, before market open. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings per share (EPS) and revenues is pegged at $1.66 and $53.6 billion, respectively.

The earnings estimates for the to-be-reported quarter have been revised downward by 6.2% over the past seven days. The bottom-line projection indicates a decline of 33.9% from the year-ago reported number. The Zacks Consensus Estimate for quarterly revenues, however, suggests a year-over-year increase of 5.7%.

For full-year 2025, the Zacks Consensus Estimate for CVX’s revenues is pegged at $194.3 billion, implying a decline of 4.2% year over year. The consensus mark for 2025 EPS stands at $7.18, indicating a contraction of around 28.6%.

In the trailing four quarters, the San Ramon, CA-based oil and gas company surpassed EPS estimates thrice and missed in the other, as reflected in the chart below.

Chevron Corporation price-eps-surprise | Chevron Corporation Quote

Our proven Zacks model does not conclusively show that Chevron is likely to beat estimates this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of beating estimates. But that’s not the case here.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Earnings ESP: Chevron has an Earnings ESP of 0.00%. This is because the Most Accurate Estimate and the Zacks Consensus Estimate are pegged at $1.66 per share each.

Zacks Rank: CVX currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Let’s start by exploring how Chevron’s third-quarter results may have been shaped by fluctuations in oil and natural gas prices.

According to the U.S. Energy Information Administration, average monthly WTI crude prices for July, August and September 2024 were $81.80, $76.68 and $70.24 per barrel, respectively. By comparison, prices declined to $68.39, $64.86 and $63.96 per barrel in the same order during the comparable months of 2025. This year-over-year drop highlights the weaker oil price environment in third-quarter 2025.

However, natural gas prices presented positive signals. In third-quarter 2025, U.S. Henry Hub average prices were $3.20 in July, $2.91 in August and $2.97 in September. These prices were significantly higher than the same months in 2024 — $2.07, $1.99 and $2.28, respectively.

With more than 60% of Chevron’s output weighted toward liquids, weaker crude prices are expected to have outweighed gains in natural gas realizations. Consequently, the Zacks Consensus Estimate for third-quarter upstream earnings is pegged at $2.7 billion — a decline of more than 41% year over year.

On the production front, however, Chevron continues to perform well. Output rose 3.2% last quarter, supported by higher volumes from the Permian Basin, Gulf of Mexico and Kazakhstan. For the third quarter, the consensus mark for total production is pegged at 3,928 thousand barrels of oil-equivalent per day (MBOE/d) versus 3,364 MBOE/d a year earlier, likely aided by the Hess acquisition.

Chevron is also expected to have experienced a boost from its downstream/refining business, with margins going up. Consequently, the Zacks Consensus Estimate for CVX’s third-quarter downstream income is pegged at $863 million, implying an improvement from $595 million earned in the year-ago period.

Rival ExxonMobil (XOM) also highlighted a similar trend, noting that refining margins rebounded in the third quarter, adding roughly $500 million to earnings versus the prior quarter. According to ExxonMobil, its fuel-making business — the largest among major oil peers — is expected to contribute an additional $300 million to $700 million, while its chemicals division may add around $200 million. ExxonMobil also indicated that changes in oil and gas realizations are expected to have minimal impact on overall earnings.

Another of Chevron’s ‘Big Oil’ peers Shell’s (SHEL) upcoming third-quarter results are expected to be mixed. Shell forecasts higher LNG liquefaction volumes and stronger Trading & Optimization performance, which should support overall profitability. Upstream production is set to rise, though earnings may take a hit of up to $400 million due to adjustments at Brazil’s Tupi field. Meanwhile, Shell’s refining margins have improved to around $11.6 per barrel, offsetting continued weakness in its chemicals segment, where losses are projected to persist.

So far this year, shares of Chevron have gained more than 7%, outperforming the Oil/Energy sector but below the S&P 500.

From a valuation perspective — in terms of forward price-to-earnings ratio — Chevron is trading at a premium compared to the industry average. The stock is also trading above its five-year mean of 11.86.

Chevron’s strong operations and production growth highlight its execution strength, but softer oil realizations and declining upstream earnings point to near-term pressure. Despite solid cash generation and disciplined capital returns — including a 4.4% dividend yield and aggressive buybacks — much of the company’s resilience appears priced in. The Hess integration expands its portfolio but adds complexity, while OPEC’s output hike clouds the demand outlook. With a premium valuation and limited catalysts for earnings growth, Chevron’s risk-reward balance now skews negative. Overall, the stock looks better suited for profit-taking than fresh buying.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 44 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 4 hours |

Saudi Aramco begins Jafurah condensate exports with sales to US and India

XOM CVX

Offshore Technology

|

| 4 hours | |

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| Feb-22 | |

| Feb-22 | |

| Feb-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite