|

|

|

|

|||||

|

|

|

Advanced Micro Devices AMD is set to release its third-quarter 2025 results on Nov. 4.

AMD expects third-quarter 2025 revenues of $8.7 billion (+/-$300 million). At the mid-point of the revenue range, this represents year-over-year growth of 28%, driven by strong double-digit growth in Client and Gaming, and Data Center segments. Sequentially, AMD expects revenues to grow approximately 13%, driven by strong double-digit growth in the Data Center segment with the ramp of AMD Instinct MI350 series GPU products.

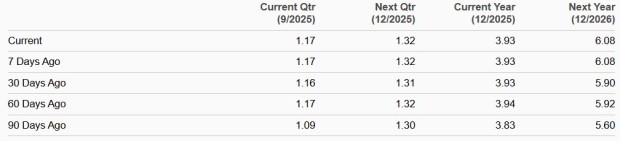

The Zacks Consensus Estimate for AMD’s third-quarter revenues is pegged at $8.72 billion, suggesting year-over-year growth of 27.9%. The consensus mark for third-quarter 2025 earnings is pegged at $1.17 per share, up by a penny over the past 30 days. The earnings estimate indicates growth of 27.2% on a year-over-year basis.

AMD beat the Zacks Consensus Estimate for earnings in all the trailing four quarters, the average surprise being 2.08%.

Advanced Micro Devices, Inc. price-eps-surprise | Advanced Micro Devices, Inc. Quote

Let’s see how things have shaped up for the upcoming earnings announcement.

AMD’s third-quarter 2025 performance is expected to have benefited from growth in both its data center and client segments, driven by continued demand for its EPYC processors and Instinct accelerators. AMD’s to-be-reported quarter results are expected to have benefited from a rich partner base that includes the likes of OpenAI, Cohere, IBM, Oracle ORCL, Google, HPE, Dell Technologies, Lenovo, Super Micro and others.

In enterprise, EPYC has been gaining traction with an expanding clientele in technology, automotive, manufacturing, financial services and public sector domains. The launch of the EPYC 4005 series is expected to boost AMD’s footprint among small and medium businesses as well as hosted IT service customers.

Adoption of EPYC by the largest cloud hyperscalers has been increasing significantly. In the second quarter of 2025, more than 100 new AMD-powered cloud instances were launched, including multiple Turin instances from Google and Oracle. At the end of the second quarter of 2025, roughly 1,200 EPYC cloud instances were available globally, a key driver behind the enterprise adoption of EPYC in the cloud. The trend is expected to have driven AMD’s top-line growth in the to-be-reported quarter.

Moreover, the Embedded segment is expected to have returned to growth in the third quarter of 2025, further driving consolidated top-line growth.

Advanced Micro Devices shares have surged 118.8% in the year-to-date period (YTD), outperforming the Zacks Computer and Technology sector’s return of 30.8% and the Zacks Computer–Integrated Systems industry’s growth of 90.5%.

The company’s shares have outperformed chip peers, including Intel INTC and NVIDIA NVDA, YTD. Shares of Intel and NVIDIA have appreciated 106.1% and 54.1%, respectively.

The AMD stock is not so cheap, as its Value Score of D suggests a stretched valuation at this moment.

In terms of the forward 12-month price/sales, Advanced Micro Devices is currently trading at 11.02X, higher than the industry’s 5.05X and Intel’s 3.38X.

Emerging AI use cases and rapid adoption of agentic AI are generating demand for general-purpose compute infrastructure, benefiting EPYC demand. AMD is benefiting from strong traction in the AI infrastructure market, driven by its advanced product portfolio and strategic investments in AI hardware and software.

In June 2025, AMD unveiled its new Instinct MI350 Series GPUs and open rack-scale AI infrastructure, showcasing significant advancements in AI performance and energy efficiency alongside major industry partners. AMD stated that its MI355 matches or exceeds NVIDIA’s B200 in critical training and inference workloads. MI355 delivers comparable performance to GB200 for key workloads at lower cost and complexity. AMD remains on track in the development of the next-generation MI400 series and is expected to launch in 2026.

However, AMD is facing stiff competition from NVIDIA and Broadcom. NVIDIA is benefiting from the strong growth of AI and high-performance, accelerated computing. The company’s newer Hopper 200 and Blackwell GPU platforms are being rapidly adopted as customers work to grow their AI infrastructure. Broadcom is benefiting from strong demand for its networking products and custom AI accelerators (XPUs). AVGO expects accelerated demand for XPUs in the back half of 2026 as hyperscalers focus more on inference, along with frontier model training.

AMD’s expanding portfolio and rich partner base are expected to have improved its top-line growth in the to-be-reported quarter. However, stiff competition and stretched valuation make the stock risky for investors.

AMD currently has a Zacks Rank #3 (Hold), suggesting that it may be wise to wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 min | |

| 11 min | |

| 16 min | |

| 23 min | |

| 24 min | |

| 25 min | |

| 28 min | |

| 35 min | |

| 37 min | |

| 41 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite