|

|

|

|

|||||

|

|

|

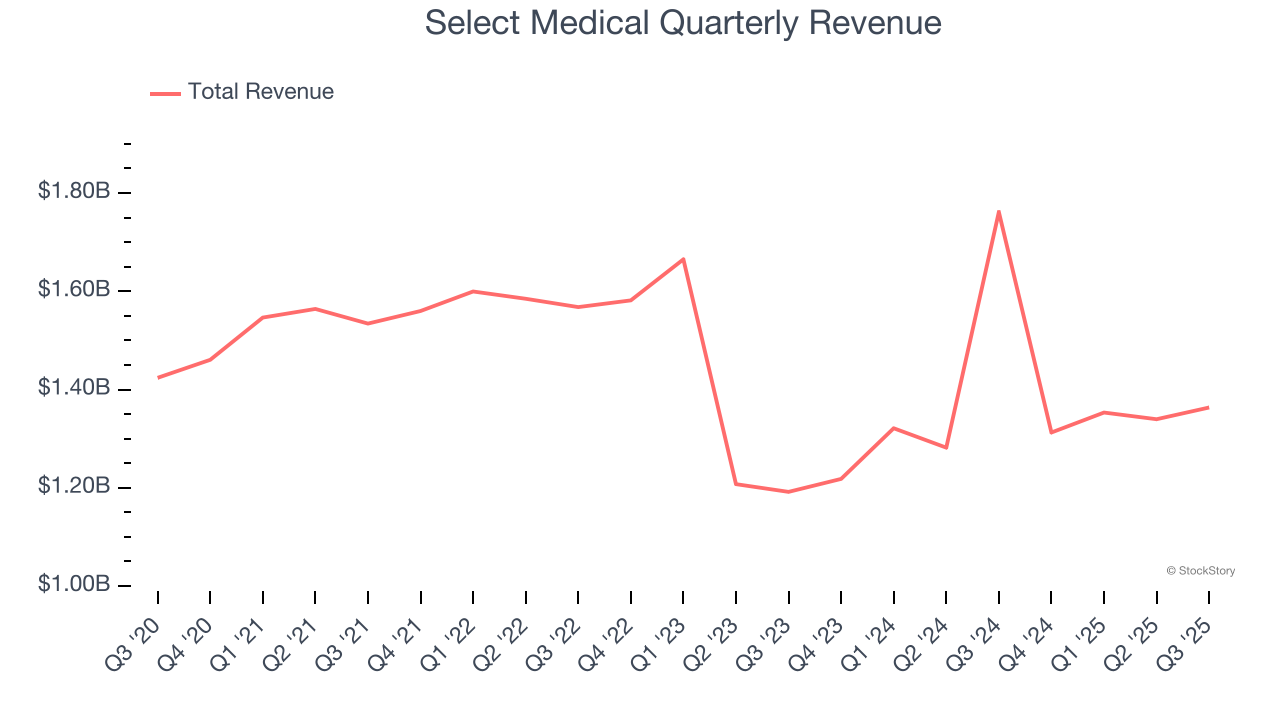

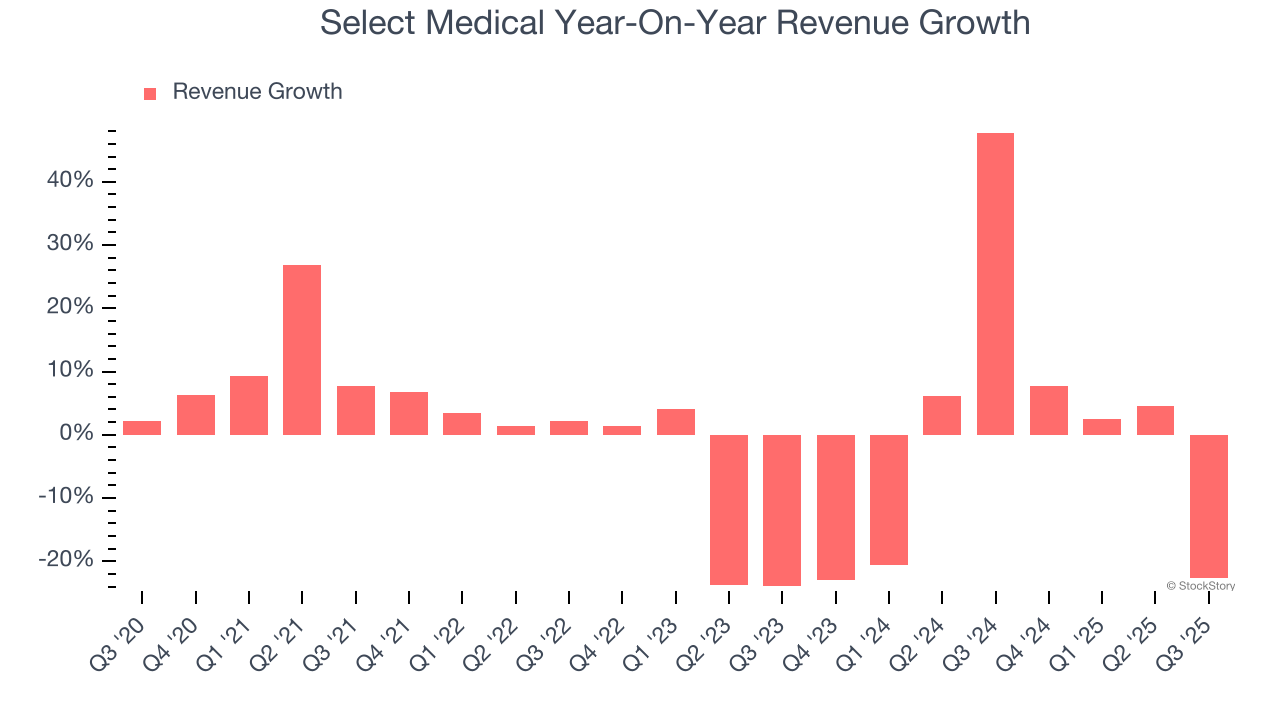

Healthcare services company Select Medical (NYSE:SEM) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales fell by 22.6% year on year to $1.36 billion. The company expects the full year’s revenue to be around $5.4 billion, close to analysts’ estimates. Its GAAP profit of $0.23 per share was 38% above analysts’ consensus estimates.

Is now the time to buy Select Medical? Find out by accessing our full research report, it’s free for active Edge members.

With a nationwide network spanning 46 states and over 2,700 healthcare facilities, Select Medical (NYSE:SEM) operates critical illness recovery hospitals, rehabilitation hospitals, outpatient rehabilitation clinics, and occupational health centers across the United States.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Select Medical struggled to consistently increase demand as its $5.37 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Select Medical’s recent performance shows its demand remained suppressed as its revenue has declined by 2.5% annually over the last two years.

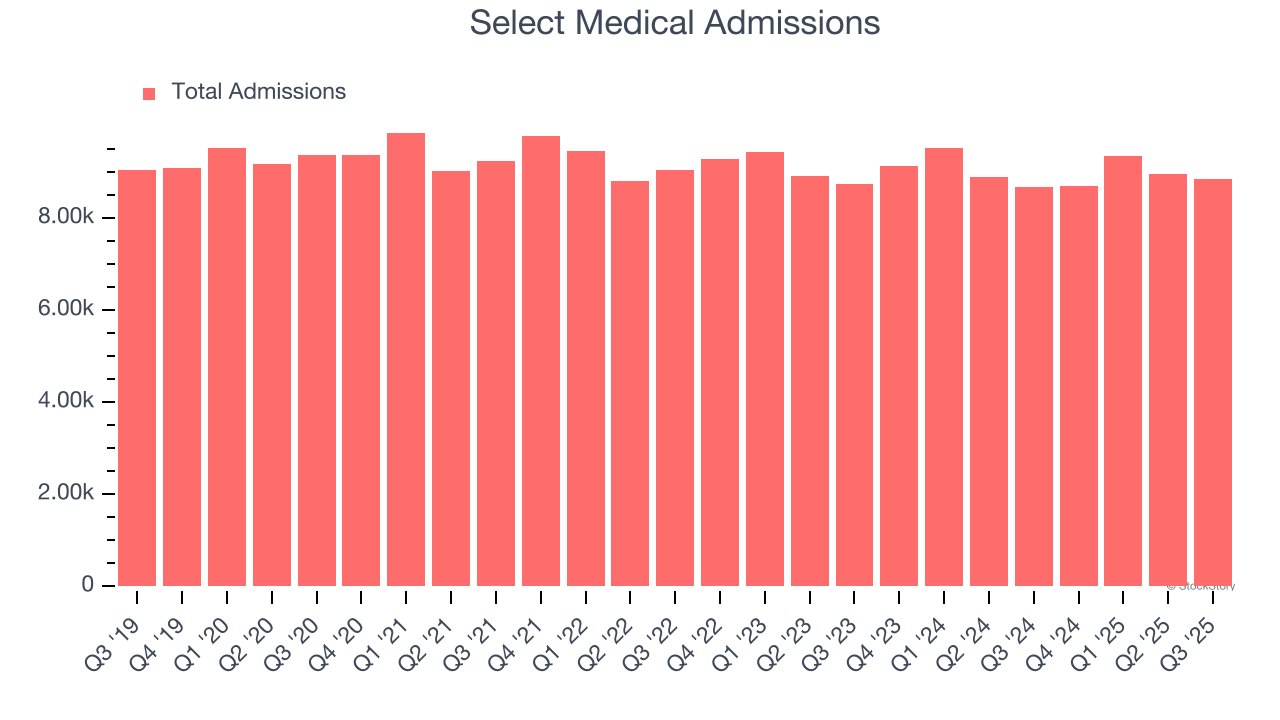

Select Medical also reports its number of admissions, which reached 8,859 in the latest quarter. Over the last two years, Select Medical’s admissions were flat. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, Select Medical’s revenue fell by 22.6% year on year to $1.36 billion but beat Wall Street’s estimates by 2.7%.

Looking ahead, sell-side analysts expect revenue to grow 4.1% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

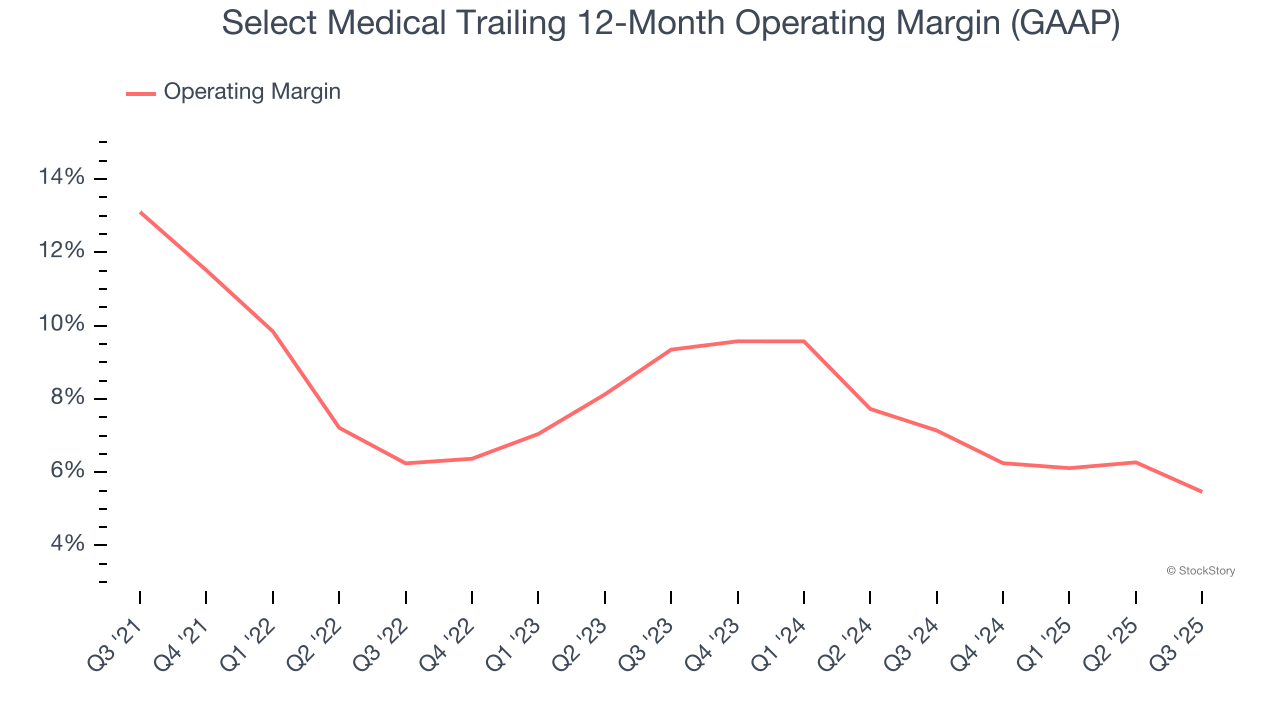

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Select Medical was profitable over the last five years but held back by its large cost base. Its average operating margin of 8.3% was weak for a healthcare business.

Looking at the trend in its profitability, Select Medical’s operating margin decreased by 7.6 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.9 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Select Medical generated an operating margin profit margin of 5.4%, down 2.7 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

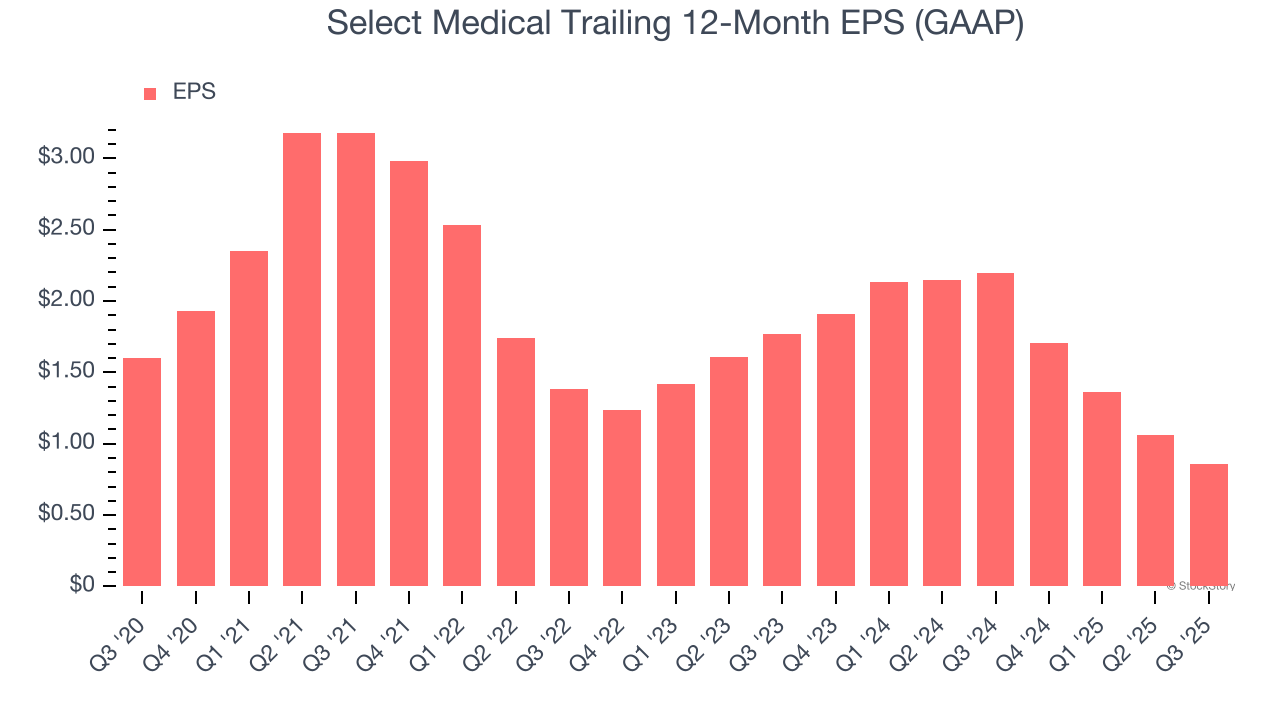

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Select Medical, its EPS declined by 11.7% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

We can take a deeper look into Select Medical’s earnings to better understand the drivers of its performance. As we mentioned earlier, Select Medical’s operating margin declined by 7.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Select Medical reported EPS of $0.23, down from $0.43 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Select Medical’s full-year EPS of $0.86 to grow 41.1%.

It was good to see Select Medical beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $14.20 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.

| Jun-26 | |

| Jun-26 | |

| Jun-12 | |

| May-27 | |

| May-25 | |

| May-21 | |

| May-19 | |

| May-08 | |

| May-04 | |

| May-02 | |

| May-01 | |

| Apr-30 | |

| Apr-30 | |

| Apr-28 | |

| Apr-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite