|

|

|

|

|||||

|

|

|

After reporting another quarter of profit growth, Sprouts Farmers Market, Inc. SFM now faces an uncertain stretch ahead. The company’s latest quarterly results, while reflecting strong operational execution and margin improvement, also showed early signs of a slowdown in its growth trajectory. Management’s cautious tone and softer near-term outlook emphasize increasing consumer pressures and tougher year-over-year comparisons. With comparable-store sales showing signs of fatigue and guidance indicating a slower finish to the year, investors are wondering whether the best of Sprouts Farmers’ growth phase is already behind.

Shares of Sprouts Farmers have fallen roughly 20% since the release of its third-quarter 2025 earnings results, wherein the top line fell short of the Zacks Consensus Estimate, while the bottom line beat the same. (Read: Sprouts Farmers Q3 Earnings Beat, Comparable Store Sales Moderate)

Decent comparable sales, positive traffic trends, accelerating unit growth and strong e-commerce performance positively impacted the quarterly results. However, management acknowledged that the trends in comparable store sales moderated, reflecting challenging year-over-year comparisons and signs of consumer softness.

Comparable store sales rose 5.9% during the quarter under review, coming in below our projected 7.6% increase. We note that e-commerce sales grew 21% and represented 15.5% of total sales in the quarter.

The company’s near-term outlook also reflects weaker confidence. Management guided for fourth-quarter comparable stores sales between 0% and 2% and earnings in the band of 86-90 cents a share, both pointing to a meaningful sequential slowdown. Management also admitted that SFM would face tough laps well into early 2026, which could limit top-line progress.

Wall Street analysts have turned cautious on Sprouts Farmers, trimming their earnings estimates. Over the past 30 days, the Zacks Consensus Estimate for the current fiscal year has slipped by 5 cents to $5.27, while the estimate for the next fiscal year has declined by 29 cents to $5.63. Despite these downward revisions, the estimates still imply year-over-year earnings growth of 40.5% and 6.8%, respectively.

Sprouts Farmers’ latest quarter results may have shown resilient profitability, but several factors indicate why investors may want to avoid the stock for now. Despite solid earnings growth, the results masked an underlying softness in comparable sales and a loss of top-line momentum. Management acknowledged that comparable-store sales decelerated faster than expected through the quarter, reflecting both tough year-over-year comparisons and a softening consumer backdrop.

The company’s core health-conscious shoppers appear to be moderating spending, particularly in middle-income and younger trade areas. This shift, coupled with lower basket sizes, signals that Sprouts Farmers’ differentiation in the natural and organic segment is losing some traction at a time when consumer budgets remain under pressure.

Comparable-store sales rose 5.9% in the third quarter, coming in below management’s expectations. Moreover, the growth rate decelerated from 10.2% and 11.7% increases registered in the second and first quarters, respectively. This slowdown carries important implications for the early part of 2026. Sprouts Farmers will lap double-digit comparable-store sales from the prior year through the first half of 2026. The company’s fourth-quarter guidance of flat to 2% comparable store sales growth already signals this normalization.

Management acknowledged that margin performance will soften in the near term as strong prior-year comparisons and moderating comps weigh on profitability. For the fourth quarter, SFM cautioned that both gross margin and SG&A rates are “normalizing,” implying a step down from the recent margin expansion achieved earlier in the year. Management pointed out that EBIT margins will be flat year over year in the fourth quarter.

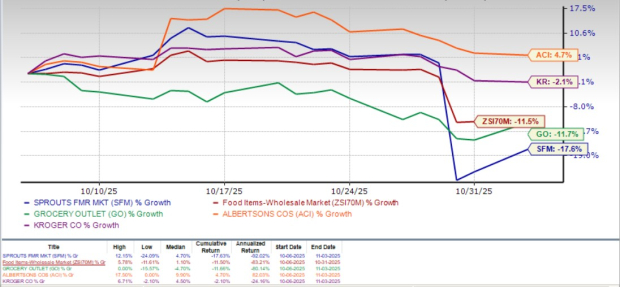

Shares of SFM closed at $83.82 yesterday, reflecting a 17.6% decline over the past month and underperforming the industry’s 11.5% drop. Sprouts Farmers has also lagged behind competitors such as Grocery Outlet Holding Corp. GO, Albertsons Companies, Inc. ACI and The Kroger Co. KR. While shares of Grocery Outlet and Kroger have fallen 11.7% and 2.1%, respectively, Albertsons Companies has risen 4.7%.

Despite the recent drop, SFM’s valuation remains elevated relative to the broader industry, reflecting expectations for sustained growth that may now be difficult to justify amid slowing comparable-store sales and cautious guidance. The premium multiple appears increasingly disconnected from near-term fundamentals, particularly as the company faces soft consumer trends and normalization in margins.

Sprouts Farmers currently trades at a forward 12-month price-to-sales (P/S) multiple of 0.85, which positions it at a premium compared to the industry’s average of 0.24. At the same time, SFM is trading below its 12-month median P/S of 1.69.

This premium positioning is especially notable when compared to peers like Grocery Outlet (with a forward 12-month P/S ratio of 0.28), Albertsons Companies (0.12) and Kroger (0.28).

Sprouts Farmers’ latest quarterly results signal a moderating sales trend and a cautious outlook clouding its near-term prospects. While the company remains profitable and operationally sound, the slowdown in comparable-store sales performance and management’s tempered guidance point to challenges. Given the soft consumer backdrop and normalization in margins, the stock’s current valuation appears stretched. At this stage, investors may be better off avoiding new positions in Sprouts Farmers, while existing shareholders could consider trimming exposure until clearer signs of renewed momentum emerge.

SFM currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-17 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-10 | |

| Jul-10 | |

| Jul-08 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite