|

|

|

|

|||||

|

|

|

Archer Daniels Midland Company ADM posted third-quarter 2025 results, wherein the top line fell short of the Zacks Consensus Estimate but increased year over year. Meanwhile, earnings surpassed the Zacks Consensus Estimate but declined from the same period last year.

Archer Daniels Midland Company price-consensus-eps-surprise-chart | Archer Daniels Midland Company Quote

Adjusted earnings of 92 cents per share surpassed the Zacks Consensus Estimate of 89 cents. However, the figure decreased from adjusted earnings of $1.09 per share in the year-ago quarter. On a reported basis, Archer Daniels’ third-quarter earnings were 22 cents per share, up from 4 cents in the year-ago quarter.

Revenues gained 2.2% year over year to $20.4 billion, but missed the consensus estimate of $20.7 billion.

Segment-wise, revenues for Ag Services & Oilseeds increased 3.5% year over year to $15.6 billion, while Carbohydrate Solutions’ revenues decreased 5.9% year over year to $2.7 billion. Nutrition’s revenues rose 4.6% year over year to $1.92 billion. The Zacks Consensus Estimate for the segments’ revenues was pegged at $15.7 billion, $2.9 billion and $1.9 billion, respectively. Revenues from Other Business are flat at $109 million compared with the figure in the prior-year period.

The gross profit decreased 7% year over year to $1.3 billion, while the gross margin stood at 6.2%. Selling, general and administrative expenses declined to $873 million from $905 million in the year-ago quarter.

Archer Daniels reported adjusted segmental operating profit of $845 million, down 19% from the year-ago quarter.

The company has a trailing four-quarter return on invested capital of 6.7% on an adjusted basis.

Adjusted operating profit for Ag Services & Oilseeds dropped 21% year over year to $379 million. The Ag Services subsegment’s operating profit rose 78%, driven by higher export activity in North America and improved results in South America. This quarter included $4 million in net positive mark-to-market (MTM) impacts, versus $50 million in net negative impacts a year earlier.

The Crushing subsegment’s operating profit plunged 93% year over year on lower margins resulting from muted demand tied to the deferral of U.S. biofuel policy and international trade challenges. There were about $41 million of net positive mark-to-market timing impacts in the quarter against zero of net negative impacts in the year-ago quarter.

Refined Products and Other operating profit was down 3% from the prior year, as biodiesel and refining margins were affected by the delayed biofuel policy, weighing on North American demand. The quarter included $8 million in net negative MTM impacts, versus $20 million in the prior-year period. Equity earnings from the company’s investment in Wilmar decreased by approximately 10% from the prior-year quarter.

The Carbohydrate Solutions segment posted an operating profit of $336 million in the third quarter of 2025, reflecting a 26% decline from the year-ago period. Operating profit in the Starches & Sweeteners subsegment also fell 36% due to lower global S&S demand, which pressured both volumes and margins. The subsegment also continued to face higher corn costs in EMEA stemming from corn quality issues, further weighing on profitability.

Global wheat milling performance remained relatively stable versus the prior-year quarter, though last year’s results had benefited from $47 million in insurance proceeds, amplifying the year-over-year comparison. Vantage Corn Processors posted a $46 million increase in operating profit, supported by strong export flows and elevated pricing amid lower industry inventory levels caused by plant downtime from maintenance programs.

The Nutrition segment reported an operating profit of $130 million in the third quarter of 2025, marking a 24% increase from the same period last year. Operating profit in the Human Nutrition subsegment gained 12% year over year. Within this segment, Flavors saw profit growth, driven by higher margins, particularly in North America. The Health & Wellness category also contributed to the increase, benefiting from stronger biotics demand.

Meanwhile, the Animal Nutrition subsegment posted an operating profit of $34 million, marking a 79% year-over-year upsurge, fueled by margin expansion from a strategic focus on higher-value product lines and continued portfolio streamlining and cost optimization initiatives.

The company ended the quarter with cash and cash equivalents of $1.24 billion, long-term debt, including current maturities, of $7.6 billion, and shareholders’ equity of $22.5 billion. As of Sept. 30, 2025, ADM generated $5.77 billion in cash from operating activities. It paid out dividends of $743 million during the nine months of 2025.

For 2025, based on performance over the first nine months of the year and current expectations regarding the timing of anticipated benefits from favorable biofuel policy developments and the evolution of global trade dynamics, the company has revised its full-year adjusted EPS guidance. Adjusted earnings are now expected to be in the range of $3.25 to $3.50 per share, compared to the previous guidance of approximately $4.00.

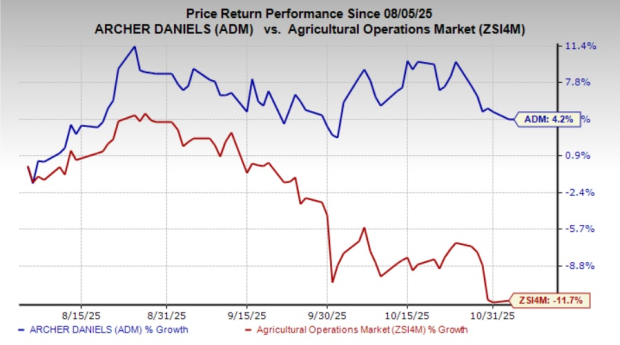

We note that shares of this Zacks Rank #3 (Hold) company have gained 4.2% in the past three months against the industry’s 11.7% decline.

We have highlighted three better-ranked stocks from the Consumer Staples sector, namely United Natural Foods, Inc. UNFI, PepsiCo, Inc. PEP and Ollie's Bargain Outlet Holdings OLLI.

United Natural is the leading distributor of natural, organic and specialty food and non-food products. It currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

UNFI delivered an earnings surprise of 416.2% in the trailing four quarters, on average. The Zacks Consensus Estimate for United Natural’s current fiscal-year sales and earnings indicates growth of 2.5% and 167.6%, respectively, from the year-ago reported figures.

PepsiCo is one of the leading global food and beverage companies. It presently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for PepsiCo’s current financial-year sales indicates year-over-year growth of 1.8%, whereas that for EPS suggests a decline of 0.6%. PEP has a trailing four-quarter negative earnings surprise of 1.1%, on average.

Ollie's Bargain is a value retailer of brand-name merchandise at drastically reduced prices and currently carries a Zacks Rank #2. OLLI delivered a trailing four-quarter earnings surprise of 4.2%, on average.

The Zacks Consensus Estimate for Ollie's Bargain’s current fiscal-year sales and earnings indicates 16.4% and 16.5% rallies, respectively, from the year-earlier reported levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 12 hours | |

| 18 hours | |

| Mar-31 | |

| Mar-29 |

Food Mega-Mergers Hardly Ever Work. Could McCormick-Unilever Be Different?

PEP

The Wall Street Journal

|

| Mar-28 | |

| Mar-26 | |

| Mar-25 | |

| Mar-25 | |

| Mar-24 | |

| Mar-23 | |

| Mar-23 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 | |

| Mar-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite