|

|

|

|

|||||

|

|

|

Form 13Fs provide investors with a way to track the quarterly buying and selling activity of Wall Street's savviest money managers.

Scion Asset Management's Michael Burry rose to fame with his wager against the U.S. housing market shortly before the financial crisis took shape in 2007.

Burry's option-based stakes against Nvidia and Palantir are supported by two historical headwinds.

For many investors, earnings season is the heartbeat of each quarter. This six-week period where a majority of S&P 500 companies report their operating results from the prior quarter provides clear evidence of the health of corporate America and the U.S. economy.

However, earnings season isn't the only quarterly event that offers invaluable data to investors. The filing of Form 13Fs with the Securities and Exchange Commission (SEC) can be of equal importance.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

A 13F is a required filing no later than 45 calendar days following the end to a quarter for institutional investors with at least $100 million in assets under management. This filing provides a concise snapshot for investors of which stocks, exchange-traded funds (ETFs), and select options Wall Street's savviest fund managers have been buying and selling.

Image source: Getty Images.

While Warren Buffett is the highest profile money manager that investors keep close tabs on, he's far from the only fund manager known to make waves on Wall Street. Scion Asset Management's Michael Burry, known affably as the "Big Short" investor (I'll touch on how he got this name in a moment), is one such asset manager that investors closely track.

Scion's latest 13F filing, covering trading activity for the September-ended quarter, shows Burry made sizable wagers against Wall Street's artificial intelligence (AI) darlings, Nvidia (NASDAQ: NVDA) and Palantir Technologies (NASDAQ: PLTR).

Based on years of Scion's 13Fs, it's apparent that Burry plays both sides of the investment aisle. This is to say that he uses his fund's capital to wager on securities increasing or decreasing in value.

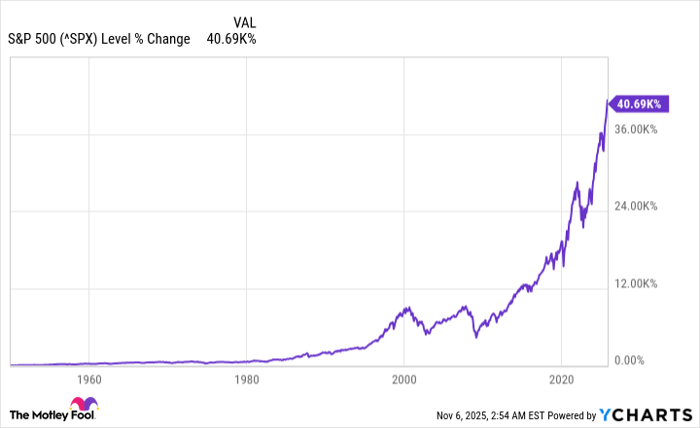

Statistically, it makes more sense to wager on the stock market to increase in value over the long run. A refreshed data set from the analysts at Crestmont Research shows that every rolling 20-year period for the S&P 500 since the start of the 20th century has resulted in a positive total return, including dividends.

The tide rises for Wall Street's benchmark index over long periods. ^SPX data by YCharts. Return data from Jan. 3, 1950 to Nov. 4, 2025.

But this doesn't mean all stocks are going to rise over time. Short-sellers are investors wagering on the share price of a public company to fall -- and Burry is no stranger to wagering against the share price or outlook of public companies.

Prior to the financial crisis taking shape from 2007 to 2009, Burry spotted trouble with the U.S. housing market. He specifically questioned the quality of the mortgage-backed securities (MBS) being held by major financial institutions. Burry ultimately purchased credit-default swaps on these MBSs that would pay out if the underlying financial instruments went into default (which they did). Despite having to pay financial institutions a premium to hold these credit-default swaps, Burry's fund cleared a profit of approximately $725 million.

Michael Burry's short of the U.S housing market is depicted in the 2015 film, The Big Short, along with the 2010 novel written by Michael Lewis, The Big Short: Inside the Doomsday Machine. This is how Burry came to be known as Wall Street's "Big Short" investor.

Image source: Getty Images.

Scion's newly filed 13F shows Michael Burry opened a $912.1 million notional value put option position in Palantir, as well as a roughly $186.6 million notional value put option stake in Nvidia.

You'll note I used the word "notional value" above to describe these positions because the exercise value of these options contracts (the notional value) can potentially differ, by a lot, from the nominal value Burry outlaid to make these wagers. Hypothetically, it doesn't take a lot of capital to wager on far out-of-the-money options contracts, but the notional value of exercising these options can be substantial.

With the above being said, these put options on Nvidia and Palantir appear substantial.

While both companies have enjoyed well-defined competitive advantages -- Nvidia is the undisputed leader in AI-graphics processing units (GPUs) and Palantir's Gotham software-as-a-service platform has no one-for-one replacement -- history would strongly suggest that Burry's wager will, eventually (keyword!), prove correct.

Arguably the leading factor working against Nvidia and Palantir is the early stage history of game-changing technologies and next-big-thing innovations. Though few investors will dispute that AI can be game-changer, the issue has to do with how quickly this technology will be adopted, utilized, and optimized on a broad scale.

Roughly 30 years ago, the advent and proliferation of the internet seemingly sent any public company with an online-based idea into the stratosphere. The dot-com bubble bursting was a function of these lofty investor expectations not being met. Since the internet arrived, other next-big-thing bubbles have followed, including genome decoding, nanotechnology, 3D printing, blockchain technology, and the metaverse. There's no indication that AI will be the exception, though there's no way to accurately forecast when bubbles will form and burst.

The respective valuations of Nvidia and Palantir act as another historical headwind that favors Burry's downside wager. In spite of their rapid growth rates, Nvidia's and Palantir's price-to-sales (P/S) ratios paint a worrisome picture.

Prior to the dot-com bubble bursting in 2000, some of the companies leading the charge peaked at P/S ratios in the neighborhood of 30 to 40. This arbitrary range has consistently served as a ceiling that megacap companies haven't been able to sustain over an extended period. Last week, Nvidia topped a P/S ratio of 30 (yet again!), and Palantir reached a P/S ratio of 152!

Once again, Burry's wager may not be timely. The Federal Reserve's rate-easing cycle, coupled with Nvidia's and Palantir's phenomenal growth rates, have the potential to support these high-flying stocks in the months or quarters to come. But based solely on what history has to tell us, there's a high probability the Big Short investor's bearish bet will be a moneymaker.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $595,194!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,153,334!*

Now, it’s worth noting Stock Advisor’s total average return is 1,036% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 3, 2025

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Palantir Technologies. The Motley Fool has a disclosure policy.

| 8 min | |

| 2 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 8 hours | |

| 8 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Nvidia Plans New Chip to Speed AI Processing, Shake Up Computing Market

NVDA

The Wall Street Journal

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite