|

|

|

|

|||||

|

|

|

U.S. legacy automaker Ford F is hovering around its 52-week high. It closed the last trading session at $13.21, just around 5% off its one-year peak. Year to date, the stock has gained more than 33%, outperforming both the industry and its closest peer, General Motors GM. Ford shares also outperformed the most valuable automaker, Tesla TSLA, whose shares rose over 6% during the same timeframe.

Ford’s third-quarter results came in better than expected, with both EPS and revenues topping estimates. With that, the company surpassed earnings in each of the trailing four quarters. Nonetheless, Ford has issued a subdued outlook for the fourth quarter amid fire at Novelis’ aluminum plant, a key supplier. In fact, per a recent Wall Street Journal article, the company is considering pulling the plug on F-150 Lightning, the best-selling e-pickup in the United States, though Ford is yet to confirm the rumor.

Against this backdrop, should investors sell F shares now that the stock is trading close to its 52-week high? Or are there enough reasons to keep holding on? Let’s assess the key drivers and challenges to find out.

Ford’s EV sales dropped nearly 25% year over year to 4,709 units in October following the expiration of the $7,500 federal EV tax credit at the end of September. Mustang Mach-E fell 12.3% in October to 2,906 units, though it rose 15% year to date. F-150 Lightning, whose production is currently paused due to the fire at the Novelis plant, slid 17.2% to 1,543 units. The E-Transit cargo van plunged 76% to only 260 units.

Just to put things in perspective, Ford reported record EV deliveries in the third quarter of 2025 as buyers rushed to take advantage of incentives. General Motors and Tesla also posted record sales during the quarter. However, this surge largely reflects a “pull-forward” effect seen across the industry, as October sales numbers already point to a broader slowdown in the EV market.

Ford’s Model e unit has been a spoilsport in the company’s overall performance. The segment continues to run at a loss amid significant costs tied to next-generation EV development. The company is expected to incur substantial losses in its EV business again this year, after posting a $5.07 billion loss in 2024.

Ford is grappling with supply disruptions following the fire at Novelis’ aluminum plant. The incident is expected to result in a fourth-quarter EBIT headwind of $1.5-$2 billion and a free cash flow hit of $2-$3 billion. Consequently, Ford lowered its 2025 adjusted EBIT guidance to $6–$6.5 billion, down from $10.2 billion in 2024 and below its earlier forecast of $6.5–$7.5 billion.

While Model e remains a drag, Ford Pro unit remains a key growth engine, supported by strong order books, rising demand for Super Duty trucks, and expanding software and service offerings. The combination of vehicles, digital solutions, and physical services continues to drive momentum in this high-margin segment.

Also, while Ford’s EV business is facing near-term headwinds, the company is positioning itself for long-term success with its Universal EV Platform, designed for affordable, digitally advanced vehicles starting around $30,000. The company plans to begin equipment installation for UEV production in Louisville and start LFP battery cell production in Michigan later this year, reinforcing its long-term electrification strategy.

Financially, Ford’s position remains solid. It ended the third quarter of 2025 with $54 billion in liquidity, including $33 billion in cash. Its dividend yield above 4% offers strong income potential, and management aims to return 40–50% of free cash flow to shareholders.

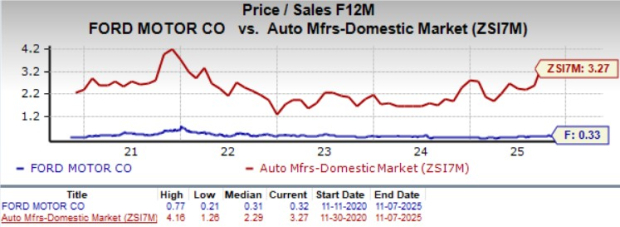

From a valuation standpoint, F trades at a forward price-to-sales ratio of 0.33, way below the industry average. It carries a Value Score of A. In comparison to this, General Motors and Tesla trade at 0.36 and 13.46, respectively.

While the Zacks Consensus Estimate for Ford’s 2025 EPS implies a 40.7% decline year over year, 2026 marks a 27% improvement from 2025 projected levels. The consensus mark for 2025 EPS has moved south over the past 60 days, but the estimates for 2026 have moved up over the same period.

Ford’s story now is about short-term bumps versus long-term potential. Yes, the EV business is still losing money, and the Novelis fire hasn’t helped. But Ford’s strong showing in its Pro division, solid cash position and reliable dividend haven’t dented investors’ confidence. And that’s reflecting in the stock’s performance.

After more than a century in business, Ford has shown time and again that it can adapt to changing industry cycles. Its strong-vehicle lineup and focus on hybrids give it breathing room as the EV market stabilizes.

So, while it may not be the best time to buy more after the rally, it’s also not a reason to jump ship. Ford stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Drivers in Dire Crashes Relied Too Much on Ford's Hands-Free Technology, NTSB Says

F

The Wall Street Journal

|

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite