|

|

|

|

|||||

|

|

|

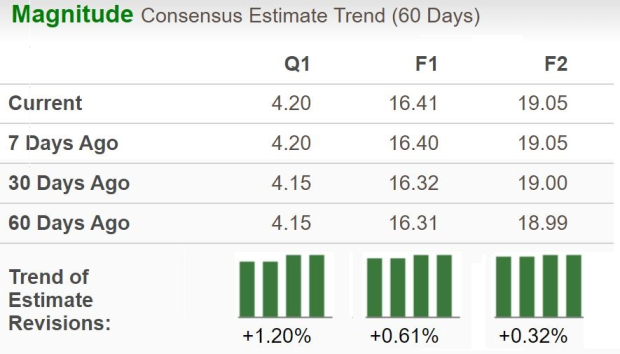

Wall Street sentiment toward Mastercard Incorporated MA is heating up, reflected in the latest upward estimate revisions. Over the past week, the Zacks Consensus Estimate for 2025 and 2026 earnings per share (EPS) has seen two and one positive adjustments, respectively — signaling renewed optimism. For 2025, Mastercard’s EPS is projected at $16.41, implying 12.4% year-over-year growth, while the 2026 estimate of $19.05 points to a 16.1% rise.

The company’s track record of consistent outperformance adds confidence; it has topped EPS estimates in each of the past four quarters, with an average surprise of 3.1%. Meanwhile, revenue forecasts of $32.6 billion for 2025 and $36.7 billion for 2026 translate to robust growth of 15.7% and 12.7%, respectively.

Despite upbeat estimates, Mastercard shares dipped 1.3% in the past month, narrower than the 4.3% decline for the broader industry. Peer performance varied: Visa Inc. V slipped 2.1%, while American Express Company AXP rallied 14.1%. In comparison, the S&P 500 Index advanced 1.6% during the same period.

This short-term pullback raises an interesting question: Should investors seize this dip as a buying opportunity? Let’s assess Mastercard’s operations, valuation and potential risks before drawing conclusions.

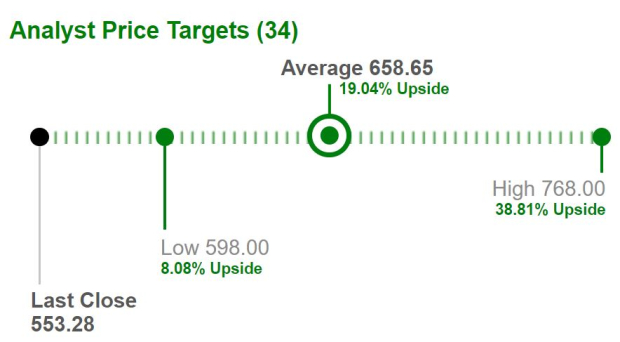

Mastercard currently trades below its average analyst price target of $658.65, implying an attractive 19% potential upside from current levels. The most bullish target stands at $768, while the lowest sits at $598, indicating a range of views but an overall upward sentiment.

The company’s gross dollar volume continues to scale higher, rising 8.2% in 2024 after 10.2% growth in 2023. During the first nine months of 2025, GDV increased by another 8.3%. Switched transactions followed a similar trajectory, up 13.9% in 2023, 11.3% in 2024, and 10.1% through the first three quarters of 2025. Cross-border assessments surged 27.5%, 21.1% and 17.1%, respectively, over those same periods, underscoring strong global momentum.

The shift toward digital and cashless payments remains Mastercard’s primary growth engine. As consumers and merchants migrate from cash to digital solutions, Mastercard is capitalizing through its global network, product innovation and technology-driven expansion. Its robust cash reserves fund both organic initiatives and selective acquisitions, ensuring continued growth.

In parallel, Mastercard is investing heavily in AI, cybersecurity and fraud prevention, areas that strengthen its value proposition and deepen client loyalty.

A major contributor to Mastercard’s growth story is its value-added services portfolio, which includes data analytics, cybersecurity and consulting solutions. Revenue from these offerings rose 16.8% year over year to $10.8 billion in 2024, fueled by increasing demand for consumer insights, digital engagement and business intelligence.

Momentum accelerated further in 2025, with value-added services generating $9.4 billion in the first three quarters alone, up 21.4% year over year. This diversification not only strengthens revenue quality but also buffers Mastercard against cyclical swings in transaction volumes.

Mastercard’s expansion across emerging markets, particularly in Southeast Asia and Latin America, aligns with its long-term growth vision. These regions house vast unbanked populations, offering significant opportunities for financial inclusion and digital adoption. However, extensive global exposure also introduces geopolitical and regulatory risks, which require active management.

While stablecoins offer faster, lower-cost transactions, they lag in areas where companies like Mastercard and Visa excel, such as superior fraud protection, credit access and rewards programs. Instead of viewing digital currencies as threats, Mastercard is integrating them into its network through partnerships with Circle, Paxos, Binance, MetaMask and OKX.

These alliances reflect Mastercard’s strategy to position itself as the bridge between traditional finance and the digital asset economy. As stablecoin regulation advances, particularly under the GENIUS Act, Mastercard’s established infrastructure could give it a major advantage in facilitating compliant real-world applications.

From a valuation perspective, Mastercard is trading at a forward P/E ratio of 29.55X, well above the industry average of 20.64X. In comparison, Visa trades at 25.84X and American Express at 21.42X. This premium reflects Mastercard’s superior growth, innovation edge and resilience, but it also limits near-term upside potential.

Mastercard’s strong operational momentum has come with higher costs. Adjusted operating expenses have climbed steadily, up 10.5% in 2023, 11% in 2024 and 14.4% through the first nine months of 2025. Rebates and incentives, which offset revenues, also increased 16.1% in 2024 and 14.9% year over year so far in 2025.

Regulatory challenges remain a persistent overhang. In June 2025, the London Competition Appeal Tribunal ruled that Mastercard and Visa’s multilateral interchange fees violated European competition law. The U.K. Payment Systems Regulator is now imposing two-stage fee caps, potentially constraining revenue growth in the region.

In the United States, the Department of Justice has accused Mastercard and Visa of using their dominance to overcharge merchants, while the proposed Credit Card Competition Act could introduce new routing mandates, pressuring margins. Despite lobbying by banks, regulatory pressure for greater payment competition is expected to remain elevated.

Adding to compliance concerns, Mastercard settled a workplace pay bias case earlier in 2025, agreeing to conduct internal pay audits, another sign of rising scrutiny over corporate governance.

Mastercard’s strong fundamentals, expanding digital ecosystem and steady earnings growth reinforce its position as a global payments leader. Continued strength in cross-border volumes and value-added services supports a solid long-term outlook. However, persistent regulatory scrutiny, rising costs and a premium valuation could temper near-term gains.

Hence, investors may prefer to wait for a better entry point. Considering the balance of strengths and risks, Mastercard currently carries a Zacks Rank #3 (Hold), indicating a neutral stance in the near term. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite