|

|

|

|

|||||

|

|

|

Eli Lilly and Company’s LLY stock has risen 18% in a month, driven mainly by a stellar third-quarter performance. Also, earlier this month, President Trump announced deals with Lilly and rival Novo Nordisk NVO to cut prices of their respective GLP-1 therapies for obesity, Zepbound and Wegovy, in exchange for Medicare access for the drugs and a three-year exemption from tariffs on pharmaceutical imports. This also contributed to the price rise.

On Oct. 30, Lilly reported solid third-quarter results, beating estimates for both earnings and sales.

Sales of Lilly’s key drugs, Mounjaro, Zepbound and Jardiance beat estimates while Verzenio and Taltz missed expectations. Lilly’s new products also contributed to sales growth.

The company raised its sales as well as earnings expectations for 2025, for the second time this year, backed by a strong performance year to date, mainly driven by the robust growth of Mounjaro and Zepbound and currency tailwinds.

Lilly raised its revenue expectations for 2025 from $60.0 billion to $62.0 billion to $63.0 billion to $63.5 billion and EPS range from $21.75 to $23.00 to $23.00 to $23.70.

However, an investment decision cannot be based on a single quarter’s good or bad performance. Let’s understand the company’s strengths and weaknesses to analyze better how to play the stock amid the recent price increase.

Lilly boasts a robust portfolio of treatments for diabetes and other cardiometabolic conditions, with its cardiometabolic division emerging as the company’s strongest segment. This success is largely attributed to its widely used GLP-1 therapies — Mounjaro for diabetes and Zepbound for weight loss. In the United States. Mounjaro is the most widely prescribed incretin for type II diabetes in the United States, while Zepbound also holds a leading market share in the anti-obesity market.

Despite being on the market for only around three years, Mounjaro and Zepbound have become key top-line drivers for Lilly, with demand rising rapidly. Mounjaro and Zepbound account for more than 50% of the company’s total revenues.

Mounjaro recorded sales of $6.52 billion in the third quarter, rising 109% year over year. While sales continue to remain strong in the United States, the growth was mainly driven by robust outperformance in ex-U.S. markets, benefiting from launches in new markets. Zepbound recorded sales of $3.59 billion in the quarter, up 185% year over year.

Launches of Mounjaro and Zepbound in new international markets and improved supply from ramped-up production in the United States have led to strong sales growth in 2025. Mounjaro and Zepbound are expected to continue to see strong demand in 2026.

Regulatory approvals for new indications and improved production capacity are expected to boost sales further.

Lilly is investing broadly in obesity and has several new molecules currently in clinical development with a range of oral and injectable medications with different mechanisms of action. This includes two late-stage candidates, orforglipron, a once-daily oral GLP-1 small molecule, and retatrutide, a GGG tri-agonist and some mid-stage candidates, bimagrumab, eloralintide and mazdutide.

Lilly has announced positive data across six studies on orforglipron in obesity and type II diabetes. An oral pill like orforglipron has the potential to be a more convenient alternative to injectable treatments like Zepbound and NVO’s Wegovy. Lilly plans to file regulatory applications for orforglipron in obesity later this year, setting up the timeline for a potential launch next year. For the type II diabetes indication, Lilly plans to file regulatory applications in the first half of 2026.

It is also evaluating orforglipron in late-stage studies in other disease areas like obstructive sleep apnea, osteoarthritis pain of the knee, stress urinary incontinence and hypertension. It also expects the first data readout from a phase III study on its triple-acting incretin, retatrutide, in osteoarthritis of the knees later in 2025.

LLY is also working to diversify beyond GLP-1 drugs by expanding into cardiovascular, oncology, and neuroscience areas. In 2025, it announced several M&A deals. It acquired Verve Therapeutics to add gene therapies for heart disease to its pipeline. Lilly has also entered into agreements to acquire Scorpion Therapeutics’ oncology drug and SiteOne Therapeutics’ non-opioid pain candidate.

Last week, Lilly announced a definitive agreement to acquire Adverum Biotechnologies ADVM, which will add the latter’s lead candidate, Ixo-vec, an intravitreal single-administration gene therapy being developed in phase III to treat vision loss associated with wet age-related macular degeneration. Ixo-vec has the potential to transform chronic eye care into a one-time treatment.

In addition to Mounjaro and Zepbound, Lilly has secured approvals for several other new therapies over the past few years. These include Omvoh for treating ulcerative colitis and Crohn’s disease, BTK inhibitor Jaypirca for mantle cell lymphoma and chronic lymphocytic leukemia, Ebglyss for moderate-to-severe atopic dermatitis, and Kisunla (donanemab) for early symptomatic Alzheimer’s disease. These newly approved drugs are also contributing to Lilly’s revenue growth. Inluriyo (imlunestrant) was approved in the United States for treating ER+, HER2-, ESR1-mutated advanced or metastatic breast cancer in September.

Lilly expects its new drugs, Mounjaro, Zepbound, Omvoh, Jaypirca, Ebglyss and Kisunla, along with the expanded use of existing drugs, to drive sales growth in 2026.

The obesity market is expected to expand to $100 billion by 2030, according to data from Goldman Sachs, which means fierce competition is inevitable. Lilly and Novo Nordisk presently dominate the market.

Mounjaro and Zepbound face strong competition from Novo Nordisk’s semaglutide medicines, Ozempic for diabetes and Wegovy for obesity.

Several other companies, like Amgen and Viking Therapeutics VKTX, are also making rapid progress in the development of more potent and convenient GLP-1-based candidates in their clinical pipeline.

Viking Therapeutics’ dual GIPR/GLP-1 receptor agonist, VK2735, is being developed both as oral and subcutaneous formulations for the treatment of obesity.

NVO, LLY and VKTX are racing to introduce oral weight-loss pills, as Wegovy and Zepbound are both injectable drugs. Novo Nordisk has already filed regulatory applications for an oral version of Wegovy in the United States and the EU and also has several next-generation candidates in its obesity pipeline, like CagriSema (a combination of semaglutide and cagrilintide) and an oral pill, amycretin (a dual GLP-1 and amylin receptor agonist). The FDA is expected to decide on the Wegovy oral formulation NDA later this year.

Others like Roche, Merck and AbbVie are also looking to enter the obesity space by in-licensing obesity candidates from smaller biotechs, which could threaten Novo Nordisk and Eli Lilly’s dominance in the market. Pfizer has offered to buy obesity drugmaker Metsera to gain a foothold in the obesity space.

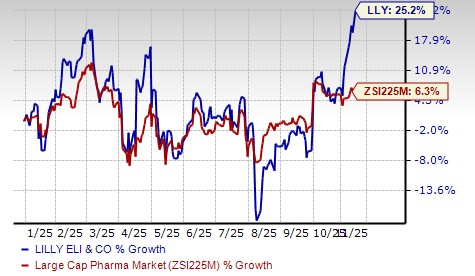

Lilly’s stock has risen 25.2% so far this year compared with the industry’s increase of 6.3%.

From a valuation standpoint, Lilly’s stock is expensive. Going by the price/earnings ratio, LLY’s shares currently trade at 31.62 forward earnings, much higher than 15.57 for the industry. However, LLY’s stock is trading below its 5-year mean of 34.54.

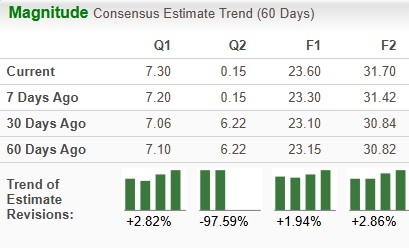

The Zacks Consensus Estimate for 2025 has risen from $23.10 per share to $23.60 per share over the past 30 days, while that for 2026 has risen from $30.84 to $31.70 per share over the same timeframe.

Lilly has its share of problems. Prices of most of Lilly’s products are declining in the United States. Potential competition in the GLP-1 diabetes/obesity market is a key headwind.

However, exceptional growth from Mounjaro and Zepbound has made it the largest drugmaker with a market cap of more than $850 billion, and its stock price fast nearing $1000 per share.

Despite its expensive valuation, Lilly is a great stock to have in one’s portfolio, considering its product and pipeline portfolio in high-growth therapeutic areas like obesity, robust growth prospects and bullish analyst sentiment. Consistently rising estimates also reflect analysts’ optimistic outlook for the stock.

The drug sector has also recovered, with large drugmakers like Pfizer and AstraZeneca signing drug pricing agreements with the Trump administration. Both companies have offered to cut prescription drug prices and boost domestic investments in exchange for a three-year exemption from tariffs on pharmaceutical imports. The deals between Pfizer and AstraZeneca and the Trump administration have raised hopes of a sustainable sector recovery, with the President offering to hold off the tariffs on pharmaceutical imports to sign similar deals with other drugmakers.

Investors who own this Zacks Rank #3 (Hold) stock should retain it. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 4 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite