|

|

|

|

|||||

|

|

|

C.H. Robinson Worldwide has been on fire lately. In the past six months alone, the company’s stock price has rocketed 53.4%, reaching $147.17 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy C.H. Robinson Worldwide, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free for active Edge members.

We’re happy investors have made money, but we're swiping left on C.H. Robinson Worldwide for now. Here are three reasons why CHRW doesn't excite us and a stock we'd rather own.

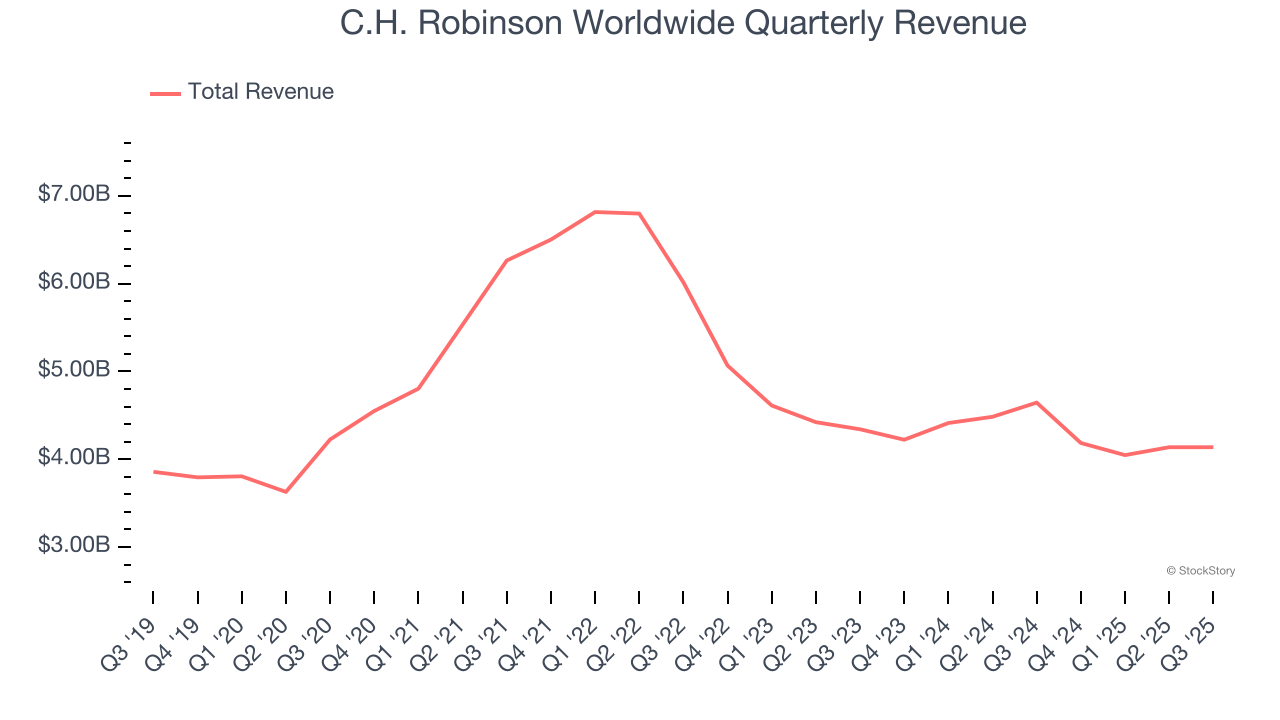

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, C.H. Robinson Worldwide’s sales grew at a weak 1.3% compounded annual growth rate over the last five years. This fell short of our benchmarks.

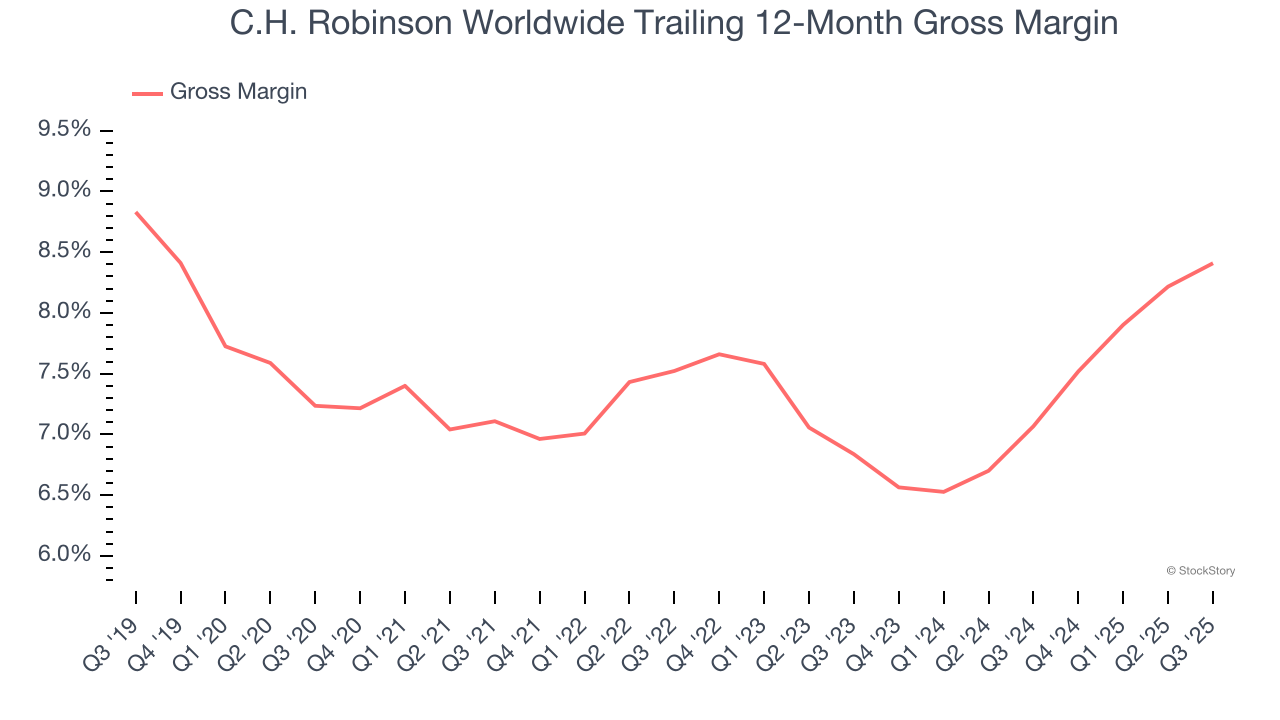

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

C.H. Robinson Worldwide has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 7.4% gross margin over the last five years. That means C.H. Robinson Worldwide paid its suppliers a lot of money ($92.63 for every $100 in revenue) to run its business.

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, C.H. Robinson Worldwide’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

C.H. Robinson Worldwide isn’t a terrible business, but it doesn’t pass our bar. Following the recent surge, the stock trades at 26.7× forward P/E (or $147.17 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Fresh US-China trade tensions just tanked stocks—but strong bank earnings are fueling a sharp rebound. Don’t miss the bounce.

Don’t let fear keep you from great opportunities and take a look at Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.

| Mar-11 | |

| Mar-08 | |

| Mar-08 | |

| Mar-06 | |

| Mar-04 | |

| Mar-04 | |

| Mar-02 | |

| Feb-27 | |

| Feb-26 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite