|

|

|

|

|||||

|

|

|

Advanced Micro Devices AMD envisions the data center total addressable market (TAM) to hit $1 trillion by 2030, suggesting a CAGR of more than 40% from roughly $200 billion estimated in 2025. AMD expects its data center AI revenues to see a CAGR of more than 80% over the next 3-5 years, driven by strong demand for instinct GPUs (MI450 Series and Helios rack-scale solutions) and expanding clientele that includes multiple hyperscalers as well as sovereign opportunities. Overall data center business revenues and total revenues are expected to see a CAGR of more than 60% and greater than 35%, respectively, over the same time frame.

Although the projections are attractive for investors, are they compelling enough to buy the stock? Let’s dig deep to find out.

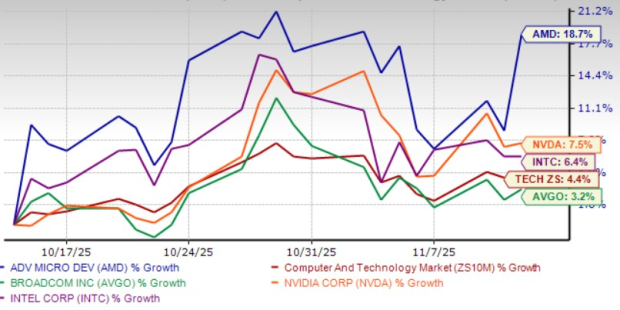

AMD shares have jumped 18.7% in the past month, outperforming the Zacks Computer and Technology sector and its closest peers, NVIDIA NVDA, Broadcom AVGO and Intel INTC. Shares of NVIDIA, Broadcom and Intel climbed 7.5%, 3.2%, and 6.4%, respectively. The broader sector has climbed up 4.4%. However, over the trailing 12-month period, Broadcom shares have outperformed AMD. While AVGO shares have returned 108.5%, AMD has appreciated 86.4%. Intel and NVIDIA shares have returned 51.3% and 31.8%, respectively, over the same time frame.

AMD’s outperformance can be attributed to strong demand for EPYC processors that power cloud and enterprise workloads. Emerging AI use cases and rapid adoption of agentic AI are generating demand for general-purpose compute infrastructure, benefiting EPYC demand. AMD is benefiting from strong traction in the AI infrastructure market, driven by its advanced product portfolio and strategic investments in AI hardware and software.

However, NVIDIA is benefiting from the strong growth of AI and high-performance, accelerated computing. The company’s newer Hopper 200 and Blackwell GPU platforms are being rapidly adopted as customers work to grow their AI infrastructure. Broadcom is benefiting from strong demand for its networking products and custom AI accelerators (XPUs). AVGO expects accelerated demand for XPUs in the back half of 2026 as hyperscalers focus more on inference, along with frontier model training. Intel is undertaking various strategic decisions to gain a firmer footing in the expansive AI sector. Capital infusion by Softbank, NVIDIA and direct funding from the U.S. Department of Commerce are likely to pave the way for innovation and growth.

Strong demand for fifth-gen EPYC processors and Instinct MI350 series GPUs is driving AMD’s top-line growth. In the third quarter of 2025, hyperscalers launched more than 160 EPYC-powered instances, including new Turin offerings from Google, Microsoft Azure, Alibaba and others. More than 1,350 public EPYC cloud instances are now available globally, up roughly 50% year over year.

A strong portfolio is driving AMD’s prospects. The company recently introduced its Helios design supporting Meta Platforms’ new Open Rack Wide specification. AMD launched ROCm 7 software, which delivers an improved AI training and inference performance with richer enterprise deployment tools. ROCm 7 delivers up to 4.6 times higher inference and 3 times higher training performance compared to ROCm 6.

An expanding partner base that includes the likes of OpenAI, HPE, Dell Technologies, Lenovo, Super Micro, Amazon Web Services, Oracle, Cisco, IBM, Cohere, Vultr, DigitalOcean and others is driving AMD’s prospects.

AMD expects fourth-quarter 2025 revenues of $9.6 billion (+/-$300 million). At the mid-point of the revenue range, this represents year-over-year growth of approximately 25% and sequential growth of approximately 4%.

The Zacks Consensus Estimate for fourth-quarter 2025 revenues is pegged at $9.65 billion, indicating 25.97% from the figure reported in the year-ago quarter. The consensus mark for fourth-quarter 2025 earnings is pegged $1.31 per share, unchanged over the past 30 days, suggesting 20.18% from the figure reported in the year-ago quarter.

Advanced Micro Devices, Inc. price-consensus-eps-surprise-chart | Advanced Micro Devices, Inc. Quote

AMD stock is currently overvalued, as the Value Score of D suggests a stretched valuation at this moment.

The stock is trading at a premium, with a forward 12-month price/sales of 10.22X compared with the sector’s 6.88X.

AMD’s expanding portfolio, growing data center AI footprint and rich partner base are expected to improve its top-line growth. However, its near-term prospects are dull due to macroeconomic uncertainties and stiff competition, particularly from NVIDIA in the cloud data center and AI chip markets. Stretched valuation is a concern.

AMD currently has a Zacks Rank #3 (Hold), suggesting that it may be wise for investors to wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 19 min | |

| 26 min | |

| 29 min | |

| 36 min | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite