|

|

|

|

|||||

|

|

|

IonQ has incorporated several quantum computer capabilities into its operations through acquisitions.

The company's sales are going strong, rising 222% year over year in the third quarter to $39.9 million.

IonQ's many acquisitions contributed to a Q3 operating loss of $168.8 million.

Quantum computing stocks have been popular over the past year, but among the pure-play quantum companies, one of the most compelling to invest in is IonQ (NYSE: IONQ). It has made tremendous strides in its quest to become the Nvidia of quantum computing. IonQ seeks to produce quantum processors that are as indispensable as Nvidia's artificial intelligence (AI) semiconductor chips.

If IonQ's technological success can match its lofty ambitions, it could be a good long-term investment. Here's a deeper dive into the company to evaluate whether now is the time to invest in IonQ.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

In order to become a leader in the nascent field of quantum computing, IonQ pursued several acquisitions, which helped to quickly expand its offerings. As a result, the company claims to be "the world's most complete quantum platform."

One of its most recent acquisitions is Oxford Ionics, which holds the world record for fidelity (a measure of accuracy of quantum operations). A big challenge to the progress of quantum devices is reducing currently high error rates. Purchasing Oxford Ionics is intended to help IonQ improve its error rates.

The company also acquired businesses to build a quantum computing network and to develop quantum capabilities to deploy in outer space. The latter may seem a bit extreme, considering IonQ's fidelity problems, but its space features helped it win a contract with the U.S. Department of Energy to demonstrate quantum-based secure satellite communications.

These kinds of customer wins allowed IonQ to grow revenue in the third quarter by 222% year over year to $39.9 million. The strong sales growth prompted the company to raise its 2025 full-year revenue forecast to a range of $106 million to $110 million.

Even the low end of that range represents a massive increase over 2024's $43.1 million and made the company the first public pure-play quantum business to project triple-digit sales, according to IonQ.

While its acquisitions helped IonQ quickly build up its quantum capabilities, this progress came at a cost. The company exited the third quarter with an operating loss of $168.8 million, a substantial increase from the prior year's loss of $53.1 million.

IonQ's revenue growth isn't keeping pace with its large and growing operating losses. So to help fund its acquisition appetite, the company executed a $1 billion equity offering in July, then another for $2 billion in October.

These actions brought IonQ's cash hoard to a robust $3.5 billion on a pro forma basis as of Sept. 30. While the funds from the equity offerings will sustain IonQ's operations for a time, they cause share dilution.

Moreover, the company's downsides contributed to shares dropping from the 52-week high of $84.64 reached on Oct. 13, despite strong Q3 sales growth and a rise in the full-year outlook.

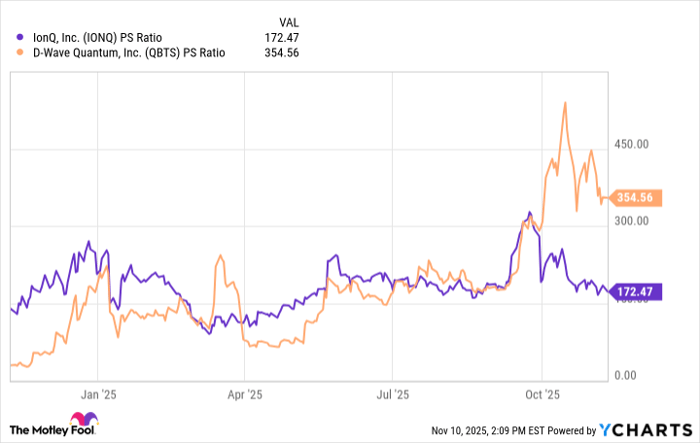

With the stock price drop, perhaps now is a good time to pick up IonQ shares. Consider the stock's price-to-sales (P/S) ratio, which measures how much investors pay for every dollar of revenue generated over the trailing 12 months, and compare it to that of fellow pure-play quantum computing company D-Wave Quantum.

Data by YCharts.

The chart reveals IonQ's P/S ratio is far lower than D-Wave's, which indicates it is a better value than its rival. Still, at a sales multiple over 100, IonQ stock is not cheap. For example, Nvidia is a leader in the hot artificial intelligence sector, yet its P/S ratio is about 30.

That said, given the technological platform IonQ is rapidly building, the promise of potent computational power through its ion-based quantum computers, and the sales growth validating customer interest in its solutions, IonQ may well be worth an elevated share price.

At this point, a good strategy is to wait for the stock price to drop further before deciding to buy. Even then, because IonQ's operating loss is high and rising, and many competitors are vying for quantum computing supremacy, only investors with a high risk tolerance should consider investing.

Before you buy stock in IonQ, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and IonQ wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $624,230!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,187,967!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 195% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 10, 2025

Robert Izquierdo has positions in IonQ and Nvidia. The Motley Fool has positions in and recommends IonQ and Nvidia. The Motley Fool has a disclosure policy.

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-14 | |

| Jul-13 | |

| Jul-07 | |

| Jul-06 | |

| Jun-30 | |

| Jun-29 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-23 | |

| Jun-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite