|

|

|

|

|||||

|

|

|

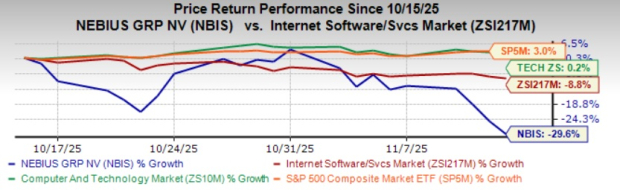

Nebius Group N.V. NBIS, a hypergrowth AI infrastructure-focused company, saw its shares slide following the third-quarter 2025 results, as widening losses and a tighter group revenue outlook weighed on investor sentiment. Notably, the company’s shares have declined 20.4% since third-quarter earnings on Nov. 7, 2025.

In the past month, shares of Nebius have plunged around 30%, underperforming the Zacks Internet Software Services industry’s decline of 8.8%. The Zacks Computer & Technology sector and the S&P 500 Composite are up 0.2% and 3%, respectively, over the same time frame.

The key question for investors: With NBIS stock down, is this dip a buying opportunity or a warning sign? Let’s take a deeper look at the recent numbers, management commentary and forward outlook points to ascertain the best course of action.

Nebius’ third-quarter 2025 adjusted net loss was $100.4 million, 153% wider than a loss of $39.7 million incurred a year ago.

The company’s revenues surged 355% year over year to $146.1 million, with the core infrastructure segment (making up 90% of total revenues) growing 400%. The increase in sales was primarily driven by strong performance in the company’s core business.

NBIS reported an adjusted EBITDA loss of $5.2 million for the third quarter, narrower than the $45.9 million loss in the prior-year quarter.

Total operating costs and expenses increased 145% to $276.3 million

As of Sept. 30, 2025, NBIS’ net loss from operations was $119.6 million compared with a loss of $43.6 million in the year-ago period.

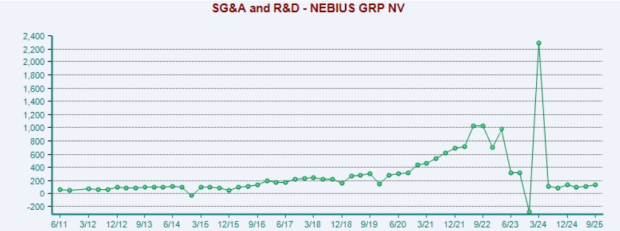

NBIS is grappling with macroeconomic uncertainties, rising expenses and heavy capital spending. In the third quarter of 2025, sales, general and administrative expenses increased 87% year over year. For 2025, Nebius has raised its capital expenditure guidance from approximately $2 billion to around $5 billion. Elevated capital expenditure levels pose a risk if revenue growth fails to keep pace with the company’s capital intensity, particularly in an environment where AI demand may fluctuate amid competitive pricing pressures and evolving regulatory frameworks.

Also, management highlighted structural operational challenges, including difficulties in securing sufficient power, ongoing supply-chain constraints and physical-world limitations that slow data-center buildouts. These issues, combined with being consistently “sold out” of capacity, limit Nebius’ ability to serve not only hyperscalers but also startups, software vendors and enterprise customers who require predictable, long-term capacity commitments. This persistent shortage risks lost business, delayed onboarding and reduced diversification of the customer base until significant new capacity, planned for late 2025 and 2026, comes online.

Nebius has tightened its full-year group revenue outlook to a range of $500 million to $550 million from the previous guidance of $450 million to $630 million. The company expects to land in the middle rather than the upper end, primarily relating to the timing of capacity coming online. Although the company continues to expect adjusted EBITDA to turn slightly positive at the group level by year-end 2025, it will remain negative for the full year.

Apart from this, scaling aggressively (multiple data centers in various regions) involves execution risk. Moreover, the company faces intense competition from other leading players, such as Microsoft Corporation MSFT, Amazon AMZN and CoreWeave, Inc. CRWV.

CRWV is rapidly scaling its purpose-built AI infrastructure, adding around 120 MW of active power to reach approximately 590 MW in total and expanding contracted power to 2.9 gigawatts in the third quarter. CoreWeave advanced large-scale GB200 deployments in the third quarter and became the first to bring the GB300 to market.

On the other hand, Amazon's AI initiatives gained significant momentum during the third quarter, representing a strategic priority across the company. AMZN launched Project Rainier, a massive AI compute cluster containing nearly 500,000 Trainium2 chips specifically designed to build and deploy Anthropic's Claude AI models. Trainium2, Amazon's custom AI chip, saw continued strong adoption and grew 150% quarter over quarter, becoming a multi-billion-dollar business that is now fully subscribed.

Valuation-wise, Nebius seems overvalued, as suggested by the Value Score of F.

In terms of Price/Book, NBIS shares are trading at 5.53X, higher than the Internet Software Services industry’s 4.26X.

Despite near-term headwinds, Nebius’ commitment to strengthening its core AI cloud business remains unwavering. The company continues to gain momentum with AI-native startups such as Cursor and Black Forest Labs, viewing these partnerships as essential to building its long-term growth engine. Its recent multi-billion-dollar agreements with Microsoft of contract value between $17.4 billion and $19.4 billion and Meta of up to $3 billion, further underscore the confidence major tech players are placing in Nebius. The company’s deals with Microsoft and Meta are expected to begin contributing late in the current quarter, with the bulk of revenue ramping through 2026.

Nebius plans to scale its existing data centers in the U.K., Israel and New Jersey in 2026 while bringing new facilities in the United States and Europe online in the first half of the year. The company is also securing several new large-scale sites, each capable of delivering hundreds of megawatts, with some expected to go live by year-end. The company now targets 2.5 GW of contracted power by 2026 and expects 800 MW to 1 GW of connected capacity by year-end, positioning itself for strong growth ahead.

Apart from these, Nebius is strengthening its enterprise portfolio with the rollout of its Aether 3.0 cloud platform and the Nebius Token Factory, a high-performance inference solution for running open-source models at scale. Nebius’ annual run-rate (ARR) revenue continues to expand, underscoring the resilience and scalability of its business model and providing a solid indicator of future growth potential. Nebius is on track to achieve its ARR guidance of $900 million to $1.1 billion by the end of 2025, setting the foundation for substantial growth in 2026 and beyond.

Although the company has strong long-term tailwinds, including multi-billion-dollar deals, accelerating data-center expansion and new enterprise offerings, the near-term risks remain significant, with high valuation, execution challenges, mounting costs and intense competition.

Given this risk-reward imbalance, existing investors may consider offloading the stock to avoid further downside, while new investors should stay on the sidelines.

At present, NBIS carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite