|

|

|

|

|||||

|

|

|

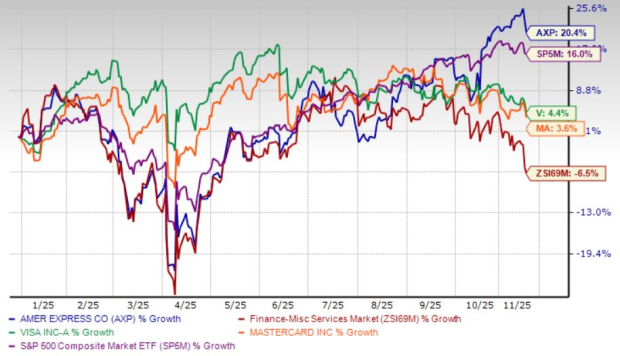

American Express Company AXP has been one of the year’s standout performers, rising 20.4% year to date and leaving both the broader market and key competitors behind. The S&P 500 has climbed 16% over the same period, while the broader industry has slipped 6.5%. Even Visa Inc. V (up 4.4%) and Mastercard Incorporated MA (up 3.6%), typically consistent outperformers, have trailed far behind.

This divergence speaks to the resilience of AmEx’s premium brand. Through a choppy macro backdrop, AmEx’s affluent, high-spending clientele and dependable earnings engine have helped it sidestep much of the volatility seen across consumer and financial stocks. As one of Berkshire Hathaway’s longest-held positions, the company continues to carry the reputation of a reliable, blue-chip compounder. Still, investors are asking the natural question: after such a strong run, is there meaningful upside left?

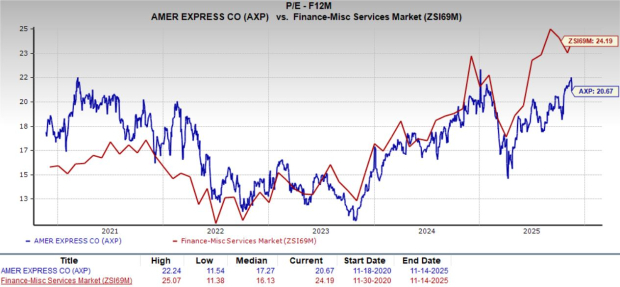

One of AmEx’s key strengths right now is its valuation setup. The stock trades at a forward P/E of 20.67X, comfortably below the industry average of 24.19X. Meanwhile, Visa and Mastercard command far richer premiums, with forward P/E ratios of 25.32X and 29.12X, respectively.

AmEx is often grouped with Visa and Mastercard, but its business model functions very differently. The company operates a closed-loop system, meaning it acts as both card issuer and bank. Unlike the pure-network models of Visa and Mastercard, AmEx earns revenues from transaction fees and interest on cardholder balances.

This dual-revenue structure gives AmEx more flexibility in shifting rate environments. It also strengthens customer relationships, since the company controls the entire payment chain end-to-end. That advantage showed up in recent results: third-quarter revenues, net of interest expense, reached $18.4 billion, up 11% year over year.

Its client base is also a stabilizing asset. While many households are pulling back due to inflation and tighter borrowing standards, AmEx’s affluent users continue spending on travel, dining, entertainment and lifestyle perks. That durability appeared in the numbers: network volumes rose 9% to $479.2 billion in the third quarter, fueled by steady U.S. consumer activity.

Management recently highlighted at the KBW Fintech Payments Conference that AmEx serves a demographic distinct from the typical Buy Now, Pay Later (BNPL) user. Rather than viewing BNPL services as direct rivals, the company sees them as complementary tools that cater to different spending tiers.

One metric that truly sets AmEx apart is its return on equity of 33.4%, more than double the industry average of 16.2%. This reflects the efficiency and pricing power embedded in its model.

Analysts have become increasingly optimistic. The Zacks Consensus Estimate now indicates 2025 earnings growth of 15.1%, followed by another 14.1% rise in 2026. Revenue estimates for those years point to expansions of 9.3% and 8.3%, respectively, signaling broad-based momentum.

Upward revisions have dominated recent analyst activity, with no downward estimate changes recorded in the past month. AmEx has also beaten earnings expectations for four consecutive quarters, generating an average surprise of 4%.

American Express Company price-consensus-eps-surprise-chart | American Express Company Quote

Because AmEx takes on lending and credit risk directly, its balance sheet is a central component of its strategy. The company ended the third quarter with $54.7 billion in cash and cash equivalents and only $1.4 billion in short-term debt. Total assets increased to $297.66 billion, up from $271.5 billion at the end of 2024.

Its net debt-to-capital ratio sits at just 4.9%, far below the industry average of 15.3%. This conservative structure enables AmEx to support cardholder loans, withstand credit cycles, meet regulatory needs and still return meaningful capital to shareholders.

In 2024, AmEx returned $7.9 billion through dividends and buybacks. In the third quarter of 2025 alone, the company distributed $2.9 billion.

Despite its many strengths, AmEx is not without vulnerabilities. The company’s heavy exposure to travel and entertainment spending can become a liability in economic downturns, as these categories weaken faster than essentials. Recent growth has also benefited from younger customers, Millennials and Gen Z, who tend to spend more selectively and may pull back if conditions worsen.

AmEx’s geographic base is another consideration. Visa and Mastercard have aggressively expanded global digital payment ecosystems, while AmEx remains comparatively domestically focused. Its dependence on lending and card volumes may also limit its ability to adapt to emerging non-card payment systems.

American Express has delivered an impressive year so far, driven by its premium customer base, strong financial discipline and differentiated closed-loop model. The company’s solid revenue momentum, consistent earnings beats and upward-trending estimates underscore the durability of its franchise, even as the broader payments landscape evolves. Its valuation remains appealing relative to major peers, and its strong balance sheet provides the flexibility to navigate credit cycles while rewarding shareholders.

That said, the stock is not without risks. AmEx’s heavier reliance on travel and discretionary spending, along with its more U.S.-centric footprint, introduces sensitivity to economic slowdowns and shifting consumer trends. These factors limit near-term visibility compared with the globally scaled, asset-light networks of Visa and Mastercard.

Balancing its strengths with its exposure to cyclical categories, AXP currently has a Zacks Rank #2 (Buy), supported by rising earnings estimates, robust profitability and sound capital management. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite