|

|

|

|

|||||

|

|

|

The ongoing wave of U.S. infrastructure, energy transition and mission-critical development has created a strong growth runway for companies positioned in engineering and construction services. Within this landscape, Sterling Infrastructure, Inc. STRL and Quanta Services, Inc. PWR are pursuing expansion in distinct ways. Sterling is sharpening its focus on large-scale site development tied to data centers, reshoring-driven manufacturing and major logistics facilities, while Quanta is scaling the broad utility, grid and renewable infrastructure platform through an integrated solutions model. Their strategies highlight two different approaches to capturing the same long-term opportunity, one more specialized and the other significantly diversified.

Both companies also operate in an environment shaped by similar pressures. Rising project complexity demands careful execution and affordability sensitivities influence spending patterns across utilities and residential markets. These shared considerations form the backdrop against which their expansion strategies are unfolding.

Let us dive deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

This Texas-based infrastructure services provider is benefiting from strong momentum in its E-Infrastructure business, which continues to be the company’s primary growth engine. The segment delivered another strong quarter, supported by accelerating demand for large-scale mission-critical projects across data centers, manufacturing facilities and e-commerce distribution.

Revenues from this segment, which represents roughly 60% of total revenues, reached $417.1 million and grew approximately 58% from the year-ago period. During the quarter, the data center market remained the key driver, with revenues rising more than 125% year over year. The company’s ability to execute complex site development projects efficiently, and often ahead of schedule, remains a key competitive advantage and a major factor in its rising activity levels.

Strength in this segment is further reflected in Sterling’s backlog. The company ended the quarter with a total backlog of $2.6 billion, an increase of 64% from the prior year. E-Infrastructure Solutions accounted for $1.8 billion of this, up 97% year over year, highlighting significant customer demand and growing visibility across multi-year project cycles. When combined with unsigned awards and future phase opportunities, total potential work exceeds $4 billion, reinforcing Sterling’s expanding presence in mission-critical infrastructure and the strong pipeline that supports continued scaling across core markets.

Despite the favorable trends, the company continues to manage a few challenges. Residential activity softened due to affordability pressures, and the wind-down of low-bid highway operations in Texas is still weighing on backlog growth.

Looking ahead, Sterling expects momentum in data centers, manufacturing and e-commerce projects to remain strong through 2026, supported by expanding customer pipelines and entry into new geographies. The company anticipates another record year in 2025 and has raised full-year guidance for both revenues and earnings. Continued growth in high-margin mission-critical work, combined with the integration of recent acquisitions and a disciplined approach to project selection, positions Sterling for sustained multi-year expansion.

PWR is benefiting from broad-based strength across its core end markets, supported by ongoing investment in electric power infrastructure, renewable energy and rising demand from large load customers. The company’s Electric segment remained the primary driver of results, accounting for 80.9% of total revenues in the third quarter of 2025. Revenues in this segment reached $6.17 billion, an increase of 17.9% year over year. Growth was supported by grid modernization needs, higher activity related to data centers and industrial customers, and steady momentum in renewable energy and battery storage work as early-stage programs advanced toward full construction.

Strong demand trends were also reflected in PWR’s record backlog. The company ended the third quarter with $39.2 billion in backlog, up from $33.96 billion in the prior year, underscoring consistent visibility across utility, renewable and technology-driven markets. Remaining performance obligations also increased, supported by expanding activity in the Electric segment and continued investment tied to manufacturing, electrification and high load requirements. This foundation allowed the company to raise expectations for full-year revenues and free cash flow while maintaining a healthy pipeline of multi-year programs.

Near-term challenges remain modest, with large generation and EPC-style projects carrying higher execution complexity and some pipeline-related work experiencing timing fluctuations. These factors introduce pockets of variability but are manageable within the broader demand environment.

Looking ahead, the company expects demand across its utility, renewable and technology customer base to remain strong as power requirements continue to rise. Growth in data centers, manufacturing, electrification and large load users is expected to support ongoing investment in transmission, substation, generation and supporting infrastructure. With an expanding total solutions platform, increasing multi-year visibility and a portfolio aligned with long-term energy and infrastructure needs, PWR is positioned for continued growth through 2026 and beyond.

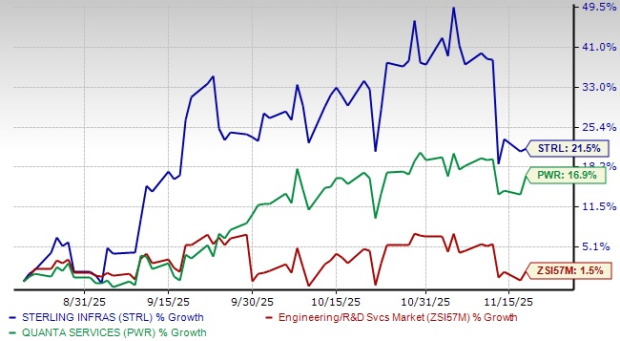

As witnessed from the chart below, in the past three months, Sterling’s share price performance stands above Quanta’s and the Zacks Engineering - R and D Services industry.

Considering valuation, Sterling is currently trading below Quanta on a forward 12-month price-to-earnings (P/E) ratio basis.

Overall, from these technical indicators, it can be deduced that STRL stock offers an incremental growth trend with a premium valuation, while PWR stock offers a slow growth trend with a discounted valuation.

The Zacks Consensus Estimate for STRL’s 2025 EPS indicates 56.9% year-over-year growth, with the 2026 estimate indicating an increase of 14.7%. The 2025 and 2026 EPS estimates have remained unchanged over the past 60 days.

The Zacks Consensus Estimate for PWR’s 2025 and 2026 earnings estimates implies year-over-year improvements of 17.8% and 16.7%, respectively. Its 2025 and 2026 EPS estimates have remained unchanged over the past 60 days.

Currently, both Sterling and Quanta hold a Zacks Rank #3 (Hold), yet their fundamentals point to different strengths. Sterling shows faster momentum with stronger stock performance, a sharper acceleration in earnings expectations, while also trading at a lower valuation compared with Quanta, which reflects its higher growth profile.

On the other hand, Quanta remains a stable long-term operator with broad exposure to utility and renewable infrastructure. Its valuation sits at a discount and the earnings outlook is steadier than rapid, supported by a record backlog but tempered by the complexity of large generation and EPC work.

Given current trends, Sterling offers slightly more near-term upside due to its stronger growth trajectory and improving mix of high-margin work, while Quanta appeals more to investors seeking steadier, long-cycle infrastructure exposure.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-31 |

Dow Jones Futures Rise, UAE Willing To Help Force Hormuz Open; Trump To Speak To Nation On Iran

PWR

Investor's Business Daily

|

| Mar-31 | |

| Mar-30 | |

| Mar-27 | |

| Mar-25 | |

| Mar-23 |

Wall Street Raises Outlook For Three AI Names And This Medical Stock

STRL +5.21%

Investor's Business Daily

|

| Mar-20 | |

| Mar-17 | |

| Mar-16 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite