|

|

|

|

|||||

|

|

|

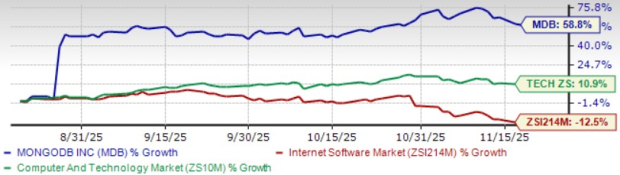

MongoDB MDB has experienced a remarkable 58.8% surge in the past three months, outperforming the Zacks Internet-Software industry’s decline of 12.5% and the Zacks Computer and Technology sector's return of 10.9%. The stock’s surge reflects stronger Atlas adoption and rising demand for MongoDB’s platform as more customers build AI-driven applications.

MongoDB trades at a forward 12-month P/S of 10.3X, well above the sub-industry average of 4.64X. The premium mirrors expectations that MDB will continue expanding its role in AI-ready data infrastructure. With Atlas scaling faster than peers and the platform broadening into higher-value enterprise workloads, its premium valuation is justifiable.

Considering MDB’s robust share price appreciation and premium valuation, investors must be wondering how to approach the stock at this stage. Let's take a closer look.

MongoDB’s Atlas platform has become a unified operational data layer that handles transactional workloads, full-text search, vector search and stream processing without the patchwork of services typically required across Snowflake SNOW, Databricks and Amazon’s AMZN Amazon Web Services (AWS).

Its document architecture supports structured, semi-structured and unstructured data in one model, enabling enterprises to replace rigid relational systems. The flexibility has driven high-profile migrations. Deutsche Telekom runs 90 Atlas clusters managing over 60 million customer records, while Agibank saw nearly five times better performance and 90% lower costs after transitioning to Atlas.

This platform's strength translates directly into measurable momentum. Atlas revenues grew 29% year over year to $438.97 million in the second quarter of fiscal 2026, representing 74% of total revenues. The Zacks Consensus Estimate for fiscal third-quarter Atlas revenues stands at $455.82 million, up 25.7% year over year. The consensus mark for Atlas customers is pegged at 59,906, up 17.2% year over year. The steady mix shift toward Atlas shows enterprises are scaling workloads on the platform, reinforcing Atlas as MongoDB’s core growth driver.

MongoDB is strengthening its role in the AI infrastructure stack as enterprises move from experimental pilots to full-scale AI applications that require flexible schemas, fast retrieval and continuous context updates. Its JSON-native design provides a structural edge over systems like PostgreSQL, which depend on add-ons such as pgvector to support vector workloads.

The acquisition of Voyage AI in February 2025 has added advanced embedding models directly into MongoDB’s environment, tightening control over the critical layer that connects enterprise data to large language models. This has attracted high-scale AI deployments, including an electric vehicle company that chose MongoDB over PostgreSQL pgvector for its autonomous driving platform managing more than a billion vectors and DevRev, which built its AgentOS platform on MongoDB to handle billions of monthly semantic requests.

The Zacks Consensus Estimate for third-quarter fiscal 2026 earnings is pegged at 79 cents per share. Although it signals a year-over-year decline of 32.76%, the upward revision of a penny over the past 30 days indicates growing confidence in MongoDB’s strategic positioning in long-term AI infrastructure.

MongoDB, Inc. price-consensus-chart | MongoDB, Inc. Quote

MongoDB’s partner and customer ecosystem continues to scale, driven by a balanced go-to-market model that pairs enterprise sales with a strong self-serve engine and deep cloud partnerships. The listing of MongoDB Enterprise Advanced on Amazon’s AWS Marketplace for the U.S. Intelligence Community streamlines procurement for federal agencies operating sensitive workloads, broadening the company’s public-sector reach.

Integrations across Amazon’s AWS, Microsoft’s MSFT Azure and Google Cloud place MongoDB directly inside cloud service catalogs, reducing deployment friction and enabling seamless adoption as enterprises modernise their data stacks. MongoDB added over 5,000 customers in the first half of fiscal 2026, with strength in both large enterprise accounts, expanding workloads and self-serve customers building new applications.

The Zacks Consensus Estimate for the fiscal third quarter pegs total customers at 62,000, up 17.9% year over year, while the consensus mark for customers over $100K is pegged at 2,699, up 16.3% year over year, reflecting continued expansion in high-value accounts. This diversified customer base across finance, healthcare, manufacturing, telecom and technology supports resilience and positions MongoDB for durable multi-sector demand.

As cloud strategies mature, many enterprises are building environments that rely on a combination of Snowflake for analytics, Microsoft for application services and Amazon for infrastructure, creating more multi-platform deployments where MongoDB becomes the operational database that ties these stacks together. This growing presence across Snowflake, Microsoft and Amazon–driven architectures is making MongoDB a consistent part of long-term modernisation roadmaps rather than a single-workload choice.

MongoDB’s momentum is being driven by real structural tailwinds, which include accelerating Atlas adoption, deeper penetration into AI infrastructure and a partner ecosystem that now extends across major cloud and data players like Amazon, Microsoft and Snowflake. Steadily expanding customer base and upward earnings estimate revisions make the company a compelling investment option.

While the stock commands a premium valuation, the underlying growth drivers remain firmly intact, positioning MongoDB to benefit from ongoing cloud modernisation and the next wave of AI-powered applications.

MongoDB currently carries a Zacks Rank #2 (Buy), and investors may consider accumulating the stock at current levels. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 35 min | |

| 56 min | |

| 3 hours | |

| 4 hours | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite