|

|

|

|

|||||

|

|

|

Nebius Group N.V. (NBIS) is aggressively prioritizing an accelerated capacity expansion strategy to fuel explosive revenue growth. With strong third-quarter demand, Nebius sold out all available capacity. This trend continues with every new round of capacity being fully absorbed as soon as it becomes available. With NVIDIA’s Blackwell generation ramping, more customers are locking in capacity earlier and for longer terms.

However, on its latest earnings call, management highlighted that capacity constraints are limiting revenue generation. To address the bottleneck, NBIS has laid out an aggressive buildout plan. By 2026, it expects contracted power to reach 2.5 GW, up from the 1 GW outlined on its August earnings call. It also plans to have 800 MW to 1 GW of power fully connected to its data centers by year-end 2026. These structural expansions are likely to dramatically increase NBIS’s capacity to serve large-scale AI workloads.

Scaling to this level requires substantial capital investments and strategic execution. Nebius has raised its 2025 CapEx guidance from approximately $2 billion to around $5 billion, reflecting strong demand and its effort to secure critical infrastructure, hardware, power, land and key sites. These strategic investments enhance its growth prospects and position the company to seize emerging opportunities. Additionally, to fund this expansion, NBIS is utilizing multiple sources such as corporate debt, asset-backed financing and equity.

All of this capacity expansion directly fuels NBIS’ revenue engine. For 2025, NBIS has revised its full-year group revenue guidance to $500–$550 million from the previous $450-$630 million. NBIS is positioned in the middle of this range mainly due to the timing of capacity coming online, while its underlying momentum and long-term growth remain very strong. It is on track to achieve its $900 million to $1.1 billion ARR target by the end of 2025 and $7–$9 billion ARR by the end of 2026.

However, in the near term, the main hurdles to expanding capacity are obtaining sufficient power and stabilizing the supply chain. Also, the AI infrastructure market is getting more competitive, with many players scaling up, leading to broader capacity shortages. Cut-throat rivalry in this space, especially from tech giants like Microsoft (MSFT) and strong contenders like CoreWeave, Inc. (CRWV), continues to challenge its potential.

Microsoft is capitalizing on the momentum of the AI business, fueled by strong Copilot adoption and the rapid expansion of its Azure cloud infrastructure. Recently, it announced plans to increase total AI capacity by more than 80% in 2025 and roughly double the total data center footprint over the next two years. For the fiscal second quarter, MSFT expects Azure revenue to grow about 37% in constant currency, as demand continues to exceed available capacity far. Even with accelerated buildouts, Microsoft now anticipates being capacity-constrained through the end of its fiscal year. Growth may also show quarterly volatility due to the timing of capacity additions and contract mix, adding further uncertainty to near-term results. However, revenues are anticipated in the $79.5-$80.6 billion band, implying growth of 14% to 16%, driven by solid AI platform adoption and record cloud bookings.

CoreWeave has rapidly expanded its footprint, benefiting from product innovations, deep customer engagements, strategic hyperscaler ties and federal-sector opportunities roll out. It is poised to capitalize on surging enterprise adoption, fueled by heightened demand across cloud, AI and data-centric workloads. However, the company remains supply-constrained, with demand for its AI cloud platform far outpacing available capacity. Delays in powered-shell delivery from a data center partner are expected to weigh on its fourth-quarter results, prompting a reduction in its 2025 outlook. Revenue is now projected at $5.05–$5.15 billion (down from $5.15–$5.35 billion), and adjusted operating income at $690–$720 million (previously $800–$830 million).

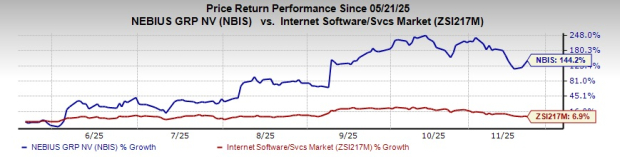

Shares of Nebius have surged 144.2% in the past six months compared with the Internet – Software and Services industry’s growth of 6.9%.

In terms of price/book, NBIS’ shares are trading at 4.66X, lower than the Internet Software Services industry’s 39.95X.

The Zacks Consensus Estimate for NBIS’ 2025 earnings has seen a downward revision over the past 60 days.

NBIS currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Jul-29 | |

| Jul-29 |

Even $64 Billion in Quarterly Profit Is a Disappointment for Chip Investors

MSFT MSFT +7.12%

The Wall Street Journal

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Dow Jones Futures Rise; Microsoft, Meta Lead Big Earnings After Market Tumbles, Oil Prices Soar

MSFT MSFT +7.12%

Investor's Business Daily

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite