|

|

|

|

|||||

|

|

|

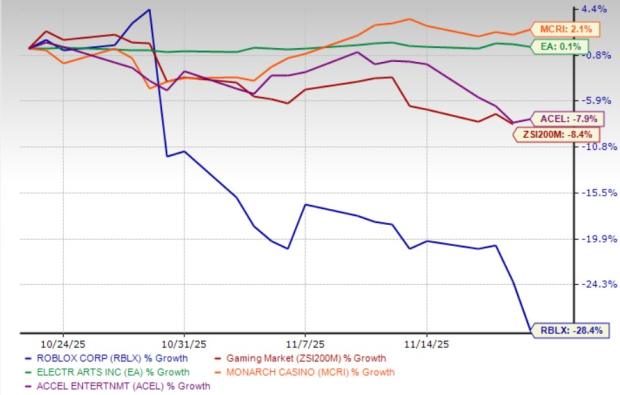

Roblox Corporation RBLX stock has lost 28.4% in the past month compared with the industry and the S&P 500’s decline of 8.4% and 0.9%, respectively. Investors reacted sharply to management commentary around slower profit expansion and uncertainty in bookings growth expectations for 2026.

In the past month, other industry players like Electronic Arts Inc. EA, Monarch Casino & Resort, Inc. MCRI and Accel Entertainment, Inc. ACEL have outperformed RBLX.

Despite posting stellar third-quarter 2025 user and bookings metrics, the market focused on signals that margin gains may remain elusive in the near term. The company expects margins to decline slightly in 2026, following a year of already limited improvements due to higher investments in safety, infrastructure and developer economics.

Investor anxiety has also been fueled by commentary suggesting tough growth comparisons in 2026, given the blockbuster performance of 2025 and the rollout of new safety policies that may temporarily weigh on engagement and bookings. Management clarified that no concrete 2026 growth guidance was being provided yet, but acknowledged market concerns around slower-than-expected momentum in the medium term.

Still, Roblox’s long-term trajectory remains compelling. With major structural investments underway and expanding global adoption, particularly among users aged 13 years and older, the recent selloff may be an overreaction. Let us break down the key drivers on both sides.

Roblox has grown faster than its cost structure could adapt. The company is increasing investment in DevEx (developer payouts), infrastructure across core and edge data centers, and trust & safety, which is expected to lead to margin compression in 2026. These expenses are not short-lived. Management has clearly indicated that margins will not improve year over year in fourth-quarter 2025 and even a modest decline heading into next year is expected.

Roblox continues to take a strict stance on platform safety, including AI-based facial age estimation and higher minimum age for restricted content, policies that may cause near-term drag on bookings. Management believes they build long-term trust and monetization, but investors remain wary of the short-term impact.

The company acknowledged that exceptionally strong 2025 performance means upcoming quarters could appear softer by comparison, one of the most direct catalysts for the recent selloff.

Rapid expansion in geographies like India and Southeast Asia, while beneficial for scale, puts pressure on bookings per user due to lower spending power. This mix shift contributed to the divergence between hours growth and monetization growth.

Roblox’s third-quarter 2025 DAUs hit 151.5 million, up 70% year over year, with hours engaged up 91%. Notably, engagement among the 13-year-olds and over audience now represents two-thirds of usage, signaling powerful demographic expansion beyond kids.

Third-quarter 2025 bookings surged 70% year over year to $1.92 billion, supported by rising payer penetration and viral hits across new and existing genres. DevEx payouts reached a new record, further strengthening creator loyalty.

Roblox is rolling out capabilities like server authority, custom matchmaking and richer avatars to break into higher-fidelity genres, including shooters, sports and racing, capturing more traditional gaming market share.

From real-time generative content to more than 400 AI systems supporting safety and discovery, Roblox is building foundational tech that rivals may struggle to replicate. The dataset advantage, 30,000 years' worth of daily 3D user interaction data, is enormous.

The Zacks Consensus Estimate for 2025 and 2026 sales is pegged at $6.64 billion and $8.09 billion, indicating 52% and 21.8% year-over-year growth, respectively.

Meanwhile, other industry players like Electronic Arts' sales in fiscal 2026 are likely to gain 9%, whereas Monarch Casino & Resort and Accel Entertainment's sales in 2025 are likely to witness a year-over-year rise of 4.2% and 7.8%, respectively.

The consensus estimate for RBLX’s 2025 loss estimates has narrowed in the past 30 days, as shown in the chart.

Roblox is currently valued at a premium compared with the industry on a forward 12-month P/S basis. RBLX’s forward 12-month price-to-sales ratio is 7.57, significantly higher than that of the industry. The company is trading at a premium compared with other industry players like Electronic Arts, Monarch Casino & Resort, and Accel Entertainment.

Roblox’s recent stock pullback reflects near-term profitability concerns and uncertainty tied to its heavy investments in safety upgrades, infrastructure and developer economics, all of which are pressuring margins even as user and booking trends remain exceptionally strong.

The long-term growth story is still intact, supported by robust engagement from older audiences, expanding global reach and technology capabilities that strengthen the platform’s competitive edge. However, with the stock still trading at a richer valuation than peers and management signaling limited margin improvement ahead, current shareholders may benefit from staying invested for future upside, while new investors should wait for better entry points as expectations reset and execution on monetization catches up to platform growth.

RBLX carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite