|

|

|

|

|||||

|

|

|

The buildout of artificial intelligence (AI) infrastructure could be a $7 trillion opportunity.

GPU designers are the most obvious beneficiaries of rising data center infrastructure spending.

Memory specialist Micron is positioned to grow alongside GPU stocks as hyperscalers continue to pour vast sums into constructing AI data centers.

When it comes to artificial intelligence (AI) stocks, the semiconductor industry is one of the most closely followed.

Parallel processors from chip designers like Nvidia, Advanced Micro Devices, and Broadcom have become the hardware backbone of generative AI. Meanwhile, Taiwan Semiconductor Manufacturing remains perhaps the most lucrative pick-and-shovel AI trade in the market given its leading position in the chip fabrication space.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Another chip stock that has put on an impressive show throughout 2025 is Micron Technology (NASDAQ: MU) -- its shares have soared 188% this year alone. After this type of rally, investors might fear they've missed their chance to get into the stock, but I'd encourage taking a longer-term perspective.

Because Micron is such a critical piece of the overall chip landscape, there's a case to be made that even now, it remains an underrated AI stock.

Much of the chatter surrounding the semiconductor industry relates to how graphics processing units (GPUs) and custom application-specific integrated circuits (ASICs) are being deployed to provide processing power in data centers. For this reason, specialty players like Micron have largely been overshadowed by the likes of Nvidia, AMD, and Broadcom.

The interesting nuance to understand here, however, is that Micron doesn't even compete with these companies. Rather, it's positioned to grow alongside its larger semiconductor cohorts.

At its core, Micron builds memory and storage chips for electronic devices and data centers. The company's DRAM (short-term memory), NAND (long-term storage), and high-bandwidth memory (HBM) solutions are necessary to allow the processors handling AI workloads to communicate with each other and process information efficiently across GPU clusters.

Image source: Micron Technology.

A recent report published by management consulting firm McKinsey & Company suggests that investment in AI infrastructure could reach nearly $7 trillion over the next five years. In addition, Goldman Sachs is forecasting that the major hyperscalers -- Microsoft, Alphabet, Amazon, and Meta Platforms -- could spend nearly $500 billion on AI capital expenditures (capex) over the next year.

Smart investors are beginning to understand that the infrastructure era is set to be a prolonged, multiyear catalyst as AI buildouts accelerate. Another way of looking at this dynamic is that the semiconductor space is swiftly transitioning from a cyclical, boom-and-bust industry to one that features more predictable, recurring demand thanks to evolving AI applications.

As big tech continues to spend hundreds of billions of dollars procuring GPUs, Micron is quietly positioned to scale up, too. In turn, AI infrastructure should ignite a sustained hardware upgrade cycle as next-generation chip architectures continue to flood the market.

Against this backdrop, AI data center owners will increasingly need to complement their GPU clusters with the best available memory and storage solutions. For Micron, that secular tailwind should translate into notable revenue acceleration and profit margin expansion -- ultimately earning it a higher valuation in the long run.

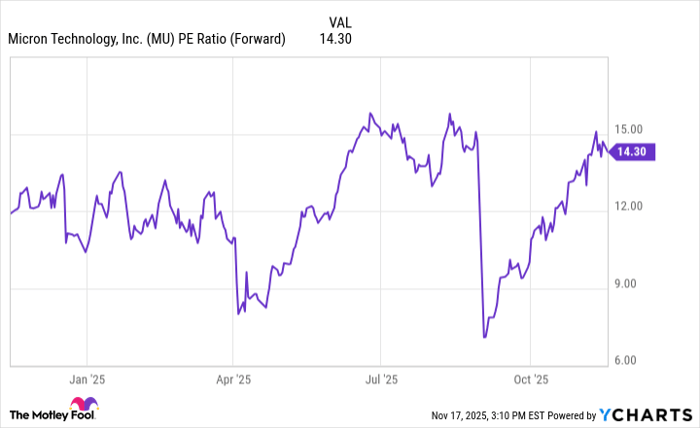

Micron currently trades at a forward price-to-earnings (P/E) multiple of 14. On the surface, it may appear that the stock is beginning to get pricey given its notable valuation expansion as of late.

MU PE Ratio (Forward) data by YCharts.

In my view, shares of Micron -- and the company's underlying valuation ratios -- have gotten frothy simply due to bullish sentiment around the idea of AI infrastructure and its benefits for chip stocks. Said differently, Micron appears to be experiencing an upswing due to macro factors rather than company-specific progress.

However, given that the market for high-bandwidth memory and storage is somewhat fragmented -- SK Hynix and Samsung are Micron's main competition -- and that the multitrillion-dollar AI infrastructure buildout still is unfolding, I think Micron appears reasonably valued.

For these reasons, I think Micron still remains a rather underrated long-term growth opportunity in the broader chip space -- making it a compelling stock to buy and hold right now.

Before you buy stock in Micron Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Micron Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $562,536!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,096,510!*

Now, it’s worth noting Stock Advisor’s total average return is 981% — a market-crushing outperformance compared to 187% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of November 17, 2025

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Goldman Sachs Group, Meta Platforms, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-02 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite