|

|

|

|

|||||

|

|

|

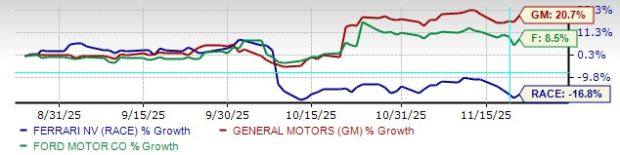

Ferrari N.V.’s (RACE) stock has hit a bumpy patch recently, falling about 17% over the last three months, even while major automakers like General Motors (GM) and Ford (F) saw their shares climb. The stock traded comfortably above $500 in early October before general investor anxiety pushed it down to its lowest price in a year.

However, the core story of the company hasn't actually changed. While the cooling stock price makes headlines, the fundamental drivers behind Ferrari’s long-term growth remain surprisingly solid — and, in many ways, truly exceptional. This recent drop draws attention back to what makes Ferrari unique: unmatched visibility into future demand, industry-leading profit margins, and a business model that is entirely different from companies that build cars for the mass market.

This analysis looks deeper into Ferrari’s recent slide and explains why the stock is still considered structurally strong despite this short-term uncertainty. Unlike mass-market brands, its strategy prioritizes scarcity over volume. This focus ensures high prices, multi-year backlogs, and consistent profits, insulating it from industry struggles and making its luxury business model nearly impossible to copy.

Ferrari’s third-quarter results once again highlighted the Purosangue’s growing dominance in the lineup. Demand remains red-hot, and production remains intentionally constrained to maintain rarity. The SUV’s contribution to the 3,401-unit quarterly delivery figure underscores Ferrari’s ability to expand its portfolio without diluting its identity — a balancing act that mainstream automakers like GM and Ford often struggle with as they chase scale over scarcity.

Alongside models like the 296 GTS and the 12Cilindri family, the Purosangue helped protect margins, improve product mix, and keep order books full well into 2027. Ferrari’s multi-year backlog remains one of its strongest competitive weapons. With more than 80% of annual sales coming from existing owners — and 40% of buyers under age 40 — demand is not only sticky but generational. This ensures that the long-term sales trajectory looks remarkably resilient, even as the stock cools in the short run.

Where mass-market peers depend on unit growth, Ferrari’s model thrives on pricing strength and customization. Every single car produced now includes personalization, and optional features already contribute around a fifth of total revenue. That mix helped Ferrari achieve an impressive EBITDA margin of 37.9% in Q3 — far beyond what GM or Ford typically reports.

The company’s strategic approach is deliberate: raise prices steadily, deepen the personalization ecosystem, and tightly manage production to maintain scarcity. Even the recent U.S. price increase of about 10% for some models landed without denting demand. Ferrari once again raised its full-year guidance, reinforcing the visibility of both revenue and cash flow. Because the company carries little debt or heavy manufacturing assets, it is free to keep increasing its high profit margins by offering more personalization and launching new models — even if it sells only slightly more cars.

Ferrari’s financial structure remains one of the cleanest in global luxury. With little debt and robust quarterly free cash flow, the company has ample flexibility to invest, innovate and reward shareholders. Since launching its multi-year €2 billion buyback program in July 2022, Ferrari has repurchased about 5.84 million shares for roughly €1.95 billion — a clear demonstration of its commitment to shareholder value. The continued pace of repurchases also reflects management’s confidence and helps lift per-share metrics at a time when the stock’s valuation multiple has eased into the mid-30s.

The company also maintains one of the industry’s deepest order books, extending into 2027 and supported by a rich pipeline of upcoming launches. Ferrari plans four new models per year between 2026 and 2030, ensuring product freshness while preserving exclusivity. This disciplined rollout strategy differentiates Ferrari from large-volume automakers like GM and Ford, whose model cycles are broader, faster, and more dependent on scale economics. Ferrari’s ability to balance innovation with controlled volumes is central to its long-run margin durability.

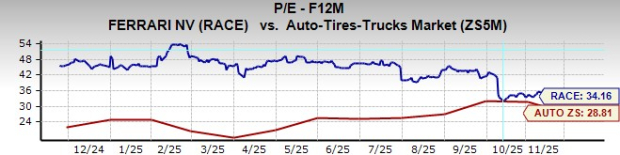

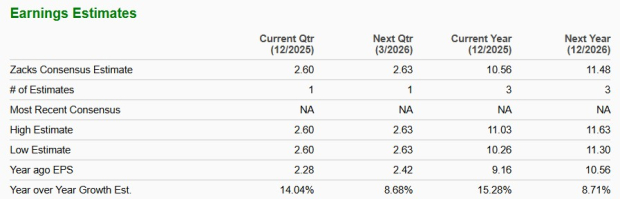

Agreed, Ferrari remains expensive compared with GM and Ford, but the premium is justified by its pricing power, deep order visibility, high margins and long-term growth runway. Earnings expectations for 2025 and 2026 call for 15.3% and 8.7% year-over-year growth — far stronger and more predictable than the consensus for GM or Ford, whose EPS trajectories remain more cyclical. Ferrari’s conservative long-term guidance has spooked some investors, but historically, the company has consistently exceeded its own targets well ahead of schedule.

Ferrari’s recent share-price slump may appear concerning, but the fundamentals tell a different story. The company continues to demonstrate pricing strength, margin leadership, a multi-year backlog, and a disciplined product and capital strategy. Despite near-term concerns around slower long-term guidance, RACE carries a Rank #1 (Strong Buy) due to its superior earnings trajectory, strong estimate revisions, and structural advantages in pricing and demand visibility. You can see the complete list of today’s Zacks #1 Rank stocks here.

For investors, the recent correction offers an appealing entry point into one of the most durable and premium franchises in global luxury. RACE remains a high-quality compounder positioned for steady long-term growth — and still one of the most compelling names in the automotive landscape.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 |

Ford, General Motors Upgraded On Profit, Cash Flow Outlooks. One Eyes A Buy Point.

GM +5.32%

Investor's Business Daily

|

| Jul-27 | |

| Jul-27 | |

| Jul-27 | |

| Jul-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite