|

|

|

|

|||||

|

|

|

Johnson & Johnson’s JNJ stock has risen 16.7% in the past three months. A lot of this price increase is due to strong third-quarter 2025 results, where in both the top and bottom lines exceeded expectations. J&J also raised its sales guidance for the year to reflect a strong operational performance.

The drug and biotech sector has recovered lately, with large drugmakers like Pfizer PFE and AstraZeneca AZN signing drug pricing agreements with the Trump administration. PFE and AZN have offered to cut prescription drug prices and boost domestic investments in exchange for athree-year exemption from tariffs on pharmaceutical imports. Eli Lilly LLY and Novo Nordisk also signed similar deals with President Trump to cut prices of their respective GLP-1 therapies for obesity, Zepbound and Wegovy, in exchange for Medicare access for the drugs and athree-year exemption from tariffs on pharmaceutical imports.

The deals between PFE, AZN, LLY and NVO and the Trump administration have raised hopes of a sustainable sector recovery, with the President offering to hold off the tariffs on pharmaceutical imports to sign similar deals with other drugmakers. J&J could well be next in line to sign a similar deal, as it iscommitted to boosting manufacturing in the United States. J&J has already announced a plan to invest $55 billion over the next four years to ensure that all medicines consumed in the United States are manufactured domestically.

J&J has also rapidly advanced its pipeline this year, which will help drive growth through the back half of the decade

Let’s understand the company’s strengths and weaknesses to better analyze how to play J&J stock amid the recent price increase.

J&J’s Innovative Medicine unit is showing a growth trend. The segment’s sales rose 3.4% in the first nine months of 2025 on an organic basis despite the loss of exclusivity (LOE) of its multi-billion-dollar product, Stelara, and the negative impact of the Part D redesign. The third quarter was the segment’s second consecutive quarter of sales of more than $15 billion despite Stelara’s LOE. Growth is being driven by J&J’s key drugs like Darzalex, Erleada and Tremfya. New drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato also contributed significantly to growth.

In 2026, J&J expects accelerated growth in the Innovative Medicine segment to be driven by its key products as well as new drugs and recently launched products, including Tremfya in inflammatory bowel disease (IBD), Rybrevant plus Lazcluze in non-small cell lung cancer and the newly approved drug, Inlexzo in bladder cancer.

J&J has rapidly advanced its pipeline this year, attaining significant clinical and regulatory milestones that will help drive growth through the back half of the decade. This year, it gained approval for new products like Inlexzoh/TAR-200, a first-of-its-kind drug-releasing system, for treating high-risk non-muscle invasive bladder cancer and Imaavy (nipocalimab) for treating generalized myasthenia gravis. J&J believes that nipocalimab has a pipeline-in-a-product potential. Regulatory applications were recently filed for another key candidate, icotrokinra, for moderate-to-severe plaque psoriasis. J&J believes that icotrokinra has the potential to revolutionize the treatment of plaque psoriasis with a once-a-day pill.

Three of J&J’s new cancer drugs are Carvykti, a BCMA CAR-T therapy for relapsed or refractory multiple myeloma, Tecvayli, for relapsed or refractory multiple myeloma, and Talvey, a novel bispecific therapy for heavily pretreated multiple myeloma. These drugs have also begun to contribute to top-line growth. Combined, they generated $2.14 billion in sales in the first nine months of 2025.

J&J’s latest acquisition of Intra-Cellular Therapies added antidepressant drug, Caplyta, to its neuroscience portfolio. Caplyta is already approved for the treatment of schizophrenia and is the only medicine approved for the treatment of depression in both bipolar 1 and 2. With a regulatory application under review, Caplyta is expected to be approved as an adjunctive treatment for major depressive disorder later in 2025.

J&J believes 10 of its new products/pipeline candidates in the Innovative Medicine segment have the potential to deliver peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, newly acquired Caplyta, Inlexzo, Rybrevant, plus Lazcluze and icotrokinra.

J&J’s MedTech business has improved in the past two quarters, driven by the acquired cardiovascular businesses, Abiomed and Shockwave, as well as Surgical Vision and wound closure in Surgery. Improvements in J&J’s electrophysiology business also drove the growth.

Along with its third-quarter earnings release, J&J announced its intention to separate its Orthopaedics franchise in the MedTech segment into a standalone orthopedics-focused company, called DePuy Synthes.

The decision aligns with J&J’s efforts to shift its MedTech portfolio to high-innovation, high-growth markets like cardiovascular and robotic surgery. J&J expects that the separation will improve its MedTech unit’s growth and margins, as the Orthopaedics franchise has been a slow-growth business for J&J.

In 2026, J&J expects better growth in the MedTech business than 2025 levels, driven by increased adoption of newly launched products across all MedTech platforms and increased focus on higher-growth markets. J&J expects to launch new products like Shockwave C2 Aero catheter and Tecnis intraocular lens in the United States, as well as regulatory submission for the OTTAVA robotic surgical system in 2026. These new products may also contribute to growth in 2026.

However, the company continues to face headwinds in China. Sales in China are being hurt by the impact of the volume-based procurement (VBP) program, which is a government-driven cost containment effort in China. J&J expects continued impacts from VBP issues in China as the program continues to expand across provinces and products.

J&J lost U.S. patent exclusivity of Stelara in 2025. Stelara was a key top-line driver for J&J, accounting for around 18% of J&J’s Innovative Medicine unit’s sales in 2024, before it lost patent exclusivity in 2025.

Several biosimilar versions of Stelara have been launched in the United States in 2025. The launch of generics is significantly eroding Stelara’s sales and hurting J&J’s sales and profits in 2025. Stelara sales declined around 40% in the first nine months of 2025.

In addition, sales in 2025 are being hurt by the impact of the Medicare Part D redesign under the Inflation Reduction Act (IRA). The Part D redesign is mainly affecting sales of drugs like Stelara, Tremfya, Erleada and pulmonary hypertension drugs. J&J expects a negative impact of approximately $2 billion in sales due to the Medicare Part D redesign in 2025.

J&J faces more than 73,000 lawsuits for its talc-based products, primarily baby powders. The lawsuits allege that its talc products contain asbestos, which caused many women to develop ovarian cancer. J&J insists that its talc-based products are safe and do not cause cancer. The company permanently discontinued the sales of the talc-based Johnson’s Baby Powder.

In April, a bankruptcy court in Texas rejected J&J’s proposed bankruptcy plan to settle its talc lawsuits after a two-week trial in Houston. J&J has gone back to the traditional tort system to fight the lawsuits individually, with its bankruptcy strategy to settle the lawsuits failing for the third time.

J&J’s shares have outperformed the industry year to date. The stock has risen 42.5% in the year-to-date period compared witha 16.0% increase in the industry. The stock has also outperformed the sector and the S&P 500 Index, as seen in the chart below.

From a valuation standpoint, J&J is slightly expensive. Going by the price/earnings ratio, the company’s shares currently trade at 18.04 forward earnings, higher than 17.04 for the industry. The stock is also trading above its five-year mean of 15.65.

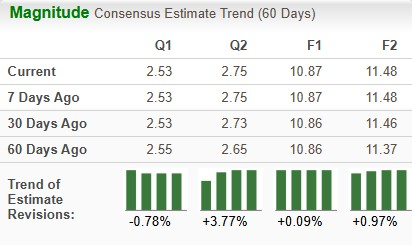

The Zacks Consensus Estimate for 2025 earnings has risen from $10.86 per share to $10.87, while that for 2026 has increased from $11.37 to $11.48 over the past 60 days.

J&J expects sales growth in both segments to be higher in 2026. It also boasts strong cash flows and has consistently increased its dividends for 63 consecutive years.

Despite headwinds like softness in the MedTech unit, the legal battle surrounding its talc lawsuits, the Stelara patent cliff and the impact of Part D redesign, J&J looks quite confident that it will be able to navigate these challenges.

J&J’s price appreciation this year, rising estimates and consistent earnings and sales growth suggest that one should hold onto this Zacks Rank #3 (Hold) stock for now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 17 min | |

| 33 min | |

| 47 min | |

| 57 min | |

| 59 min | |

| 1 hour | |

| 1 hour | |

| 1 hour |

Novo Nordisk Files Deceptive Advertising Lawsuit Against Rival Eli Lilly

LLY

The Wall Street Journal

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 9 hours | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite