|

|

|

|

|||||

|

|

|

President Trump’s sweeping global tariffs have somewhat rattled investor confidence, contributing to one of the most volatile quarters for U.S. stocks in recent years. As fears of economic fallout grow, investors may want to focus on companies less vulnerable to trade tensions. Visa Inc. V, with its low-risk, transaction-based model, stands out as a potential safe harbor.

Visa, with a market cap of $619.4 billion, is a dominant force in global digital payments. Unlike banks, Visa doesn’t issue credit cards or lend money. It simply runs the payment network and earns a fee on each transaction. This asset-light model shields it from credit risk, making it more resilient during economic downturns.

Its peer, Mastercard Incorporated MA, valued at $464.7 billion, operates a similar model. American Express Company AXP (market cap of $176.4 billion), however, takes on more risk by issuing its own cards and extending credit. While this allows AmEx to earn both interest income and processing fees, it also exposes the company to potential losses in a high-rate, inflationary environment.

Interestingly, Visa may benefit from inflation, often a consequence of tariffs. Since it charges a percentage of each transaction, rising prices can boost its revenues. With millions of transactions processed daily, even slight increases in consumer spending add up. That said, if inflation starts to dent consumer demand, Visa’s volume growth could slow, partially offsetting this benefit.

Visa is well-positioned for long-term growth, supported by the global shift away from cash toward digital payments. Its powerful network effect — where more users attract more merchants, and vice versa — further strengthens its competitive moat.

Despite ongoing macroeconomic uncertainty, Visa has continued to deliver steady earnings and revenue growth. It’s also investing heavily in innovation, with strategic expansions into real-time payments, B2B solutions, crypto, and blockchain technology, all aimed at staying ahead of the curve.

Visa is also attractive to income investors. The company maintains a solid balance sheet, with total debt making up just 35% of its capital, well below the industry average of 42.8%. In fiscal 2024, it repurchased shares worth $16.7 billion. Further, it rewarded $5.1 billion to shareholders via share buybacks ($3.9 billion) and dividends ($1.2 billion) in the first quarter of fiscal 2025. It had $9.1 billion remaining under its share repurchase authorization as of Dec. 31, 2024.

The Zacks Consensus Estimate for Visa’s fiscal 2025 and fiscal 2026 EPS implies a 12.5% and 12.6% uptick, respectively, on a year-over-year basis. The earnings estimates remained stable over the past week. Also, the consensus mark for fiscal 2025 and fiscal 2026 revenues suggests a 10.2% and 10.3% increase, respectively. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

The payments giant beat earnings estimates in each of the past four quarters with an average surprise of more than 3%.

Visa Inc. price-eps-surprise | Visa Inc. Quote

Over the past month, Visa shares only increased 0.2% but outperformed both the broader industry and the S&P 500 Index. During this time, shares of Mastercard and American Express declined 3.7% and 3.4%, respectively.

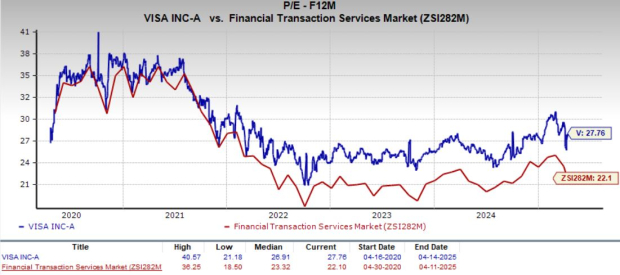

From a valuation perspective, Visa is trading at a premium. Going by its price/earnings (P/E) ratio, the company is trading at a forward earnings multiple of 27.76X, higher than its five-year median of 26.91X and the industry average of 22.10X.Meanwhile, Mastercard and American Express are currently trading at 30.75X and 16.08X, respectively.

Visa is grappling with rising costs and regulatory hurdles that could weigh on near-term performance. Adjusted operating expenses rose 10.8% in fiscal 2024 and 11.4% in first quarter of fiscal 2025. Meanwhile, client incentives — which reduce net revenues — jumped 11.9% and 13.4% over the same periods.

Regulatory headwinds are mounting. In the U.S., Visa faces a lawsuit from the Department of Justice filed last September. In the U.K., the company is dealing with scrutiny over interchange fees. The U.K.’s Payment Systems Regulator is also proposing a cap on cross-border fees, a move Visa is challenging.

In addition, the Credit Card Competition Act of 2023 could introduce more players into the U.S. payments market, pressuring both Visa and Mastercard by reducing their pricing power with merchants. The impact of these legal and regulatory challenges — combined with broader geopolitical uncertainty — is likely to shape Visa’s competitive landscape in the months ahead.

Visa’s dominant global networkand operational resilience, even amid tariff tensions and growth potential, make it a strong long-term play. The continued shift toward digital payments and Visa’s investments in real-time payments and blockchain tech only add to its growth runway.

That said, with shares trading near their 52-week high of $366.54, short-term upside appears limited. For current shareholders, holding the stock still makes sense. But for new investors, waiting for a more attractive entry point may be wise at this point.

Visa currently carries a Zacks Rank #3 (Hold), indicating a neutral stance. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour |

Digital payments sovereignty: Industry responds to UK domestic card payments alternative

MA V

Retail Banker International

|

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 7 hours | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite