|

|

|

|

|||||

|

|

|

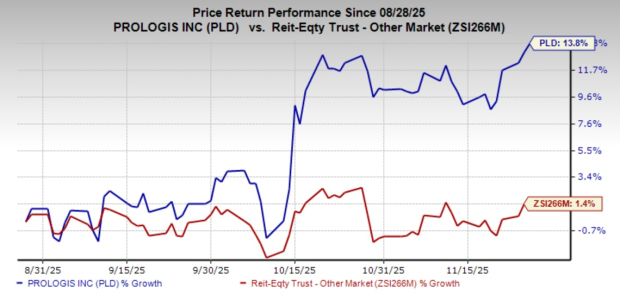

Shares of Prologis PLD have rallied 13.8% in the past three months, outperforming the industry’s growth of 1.4%. Analysts seem bullish on this Zacks Rank #3 (Hold) company. The Zacks Consensus Estimate for its 2025 and 2026 FFO per share has moved marginally northward over the past months to $5.80 and $6.08, respectively.

This industrial REIT is poised to gain from its scale and strategically located modern distribution facilities in key markets globally. Prudent buyouts, development and a healthy balance sheet will drive growth. The company is also converting some of its warehouses into data centers to capitalize on the growing opportunity in this asset category.

However, amid macroeconomic uncertainty, customers remain focused on cost controls and delay their decision-making with respect to leasing. Elevated interest expenses add to PLD’s concerns.

Let’s delve deeper and find out what’s in favor of this stock and what’s not.

Prologis operates one of the world’s largest portfolios of industrial distribution facilities, concentrating its assets in dense, supply-limited markets where proximity to major transportation hubs supports fast, efficient logistics. These well-located properties continue to draw solid demand, sustaining strong operational results across recent quarters. For 2025, we estimate occupancy to be 95.2%, reflecting the resilience of its tenant base and market positioning. The company’s new and renewal leases are expected to translate into considerable rises in future rental income. Our estimate points to a year-over-year increase of 9.1% in rental revenues in 2025, followed by growth of 6.8% in 2026 and 9.9% in 2027.

The company remains active on the expansion front, making strategic acquisitions and pursuing large development pipelines in high-barrier markets. From the beginning of the year through Sept. 30, 2025, Prologis’ share of acquisitions reached $1.19 billion, while consolidated development starts totaled $1.94 billion, most of which were build-to-suit. For 2025, management expects $1.25-$1.50 billion in acquisitions and $2.75-$3.25 billion in development starts, underscoring its discipline and scale across various deal structures.

Prologis is also leaning into the rapid growth of the data-center sector, driven by rising demand for cloud computing, AI workloads, IoT and big-data infrastructure. The company is pursuing both warehouse conversions and ground-up developments. As per the company’s September 2025 Investor Presentation, it has deployed a capital investment of $0.9 billion for data centers under development with 300 MW capacity.

Financial strength remains a defining feature for Prologis. At the end of the third quarter of 2025, liquidity stood at $7.5 billion, and the company maintained a favorable weighted average interest rate of 3.2% on debt with an average maturity of 8.3 years. Leverage remained manageable at 5.0X debt to adjusted EBITDA, and strong credit ratings, A2 from Moody’s and A from S&P, help support low borrowing costs. Coupled with consistent dividend growth of more than 12% annually over the past five years, Prologis appears well-positioned to sustain its shareholder returns in the near term. Check Prologis’ dividend history here.

Amid macroeconomic uncertainty, customers currently remain focused on cost controls and are delaying their decisions with respect to decision-making for leasing. As such, demand remains subdued, and this trend is expected to continue in the near term. Furthermore, recovery in the industrial market has continued for a long time, and the growth of e-commerce sales is likely to stabilize to some extent in the upcoming quarters. Any robust performance is unlikely in the near term.

The company’s consolidated debt as of Sept. 30, 2025 was $35.30 billion. With a high level of debt, interest expenses are likely to remain elevated. In the third quarter of 2025, interest expenses jumped 12.2% on a year-over-year basis to $258.3 million. For 2025, our estimate indicates a 14.6% year-over-year increase in the company’s interest expenses.

Some better-ranked stocks from the REIT sector are VICI Properties VICI and W.P. Carey WPC. Both VICI Properties and W.P. Carey carry a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for VICI Properties’ 2025 FFO per share is pegged at $2.37, suggesting a 4.10% increase year over year.

The Zacks Consensus Estimate for W.P. Carey’s 2025 FFO per share is pegged at $4.92, calling for a rise of 4.7% year over year.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO), a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 8 hours | |

| 8 hours | |

| Aug-01 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 |

Segro Shares Rise After Board Yields to Prologis's Final $18.7 Billion Takeover Bid

PLD

The Wall Street Journal

|

| Jul-23 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite