|

|

|

|

|||||

|

|

|

Capital One COF and Synchrony Financial SYF are major consumer lenders, primarily focusing on credit card and related financing. Both generate a large part of their revenues from interest income, transaction fees and customer spending.

While both target consumers and small businesses, SYF leans on retail and affinity partnerships, whereas COF operates more like a traditional bank with a broader credit card and auto lending portfolio.

As the Federal Reserve has started lowering interest rates, the question arises: which credit card firm, Capital One or Synchrony, is a better choice for investors? Let’s find out.

In May 2025, Capital One acquired Discover Financial in a $35 billion all-stock deal, thus becoming the largest U.S. credit card issuer by balances. The deal expanded its payments network and gave it control of Discover’s network—one of only four in the United States—boosting interchange revenues and reducing reliance on Visa V and Mastercard MA. The merger is expected to deliver cost and revenue synergies while strengthening Capital One’s digital banking capabilities.

Over the years, the company has pursued a strategic acquisition strategy, with some of its notable acquisitions being ING Direct USA, HSBC's U.S. Credit Card Portfolio and TripleTree. These have been instrumental in transforming Capital One from a monoline credit card issuer into a diversified financial services firm with a significant presence in retail banking, commercial lending and digital banking platforms.

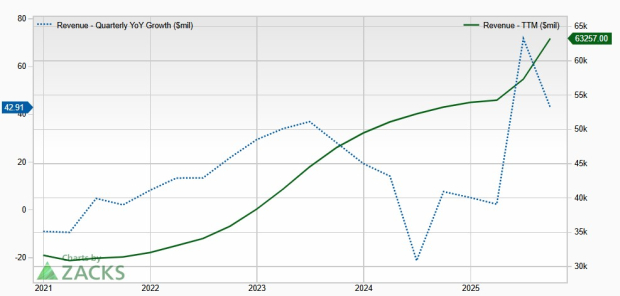

Though the company’s revenues declined marginally in 2020, the metric witnessed a five-year (2019-2024) CAGR of 6.5%. In the same time frame, net loans held for investment recorded a CAGR of 4.3%. The uptrend continued for both metrics during the first nine months of 2025. Revenue prospects look encouraging, given the company’s solid credit card and online banking businesses, Discover Financial's buyout and decent loan demand.

Capital One Revenue Trend

Capital One is likely to keep benefiting from relatively higher interest rates and a steady demand for credit card loans. As such, the company’s net interest income (NII) and net interest margin (NIM) have been rising. The company's NII witnessed a CAGR of 6% over the five years ended 2024. Also, NIM expanded to 6.88% in 2024 from 6.63% in 2023. The momentum continued for both NII & NIM in the first nine months of 2025.

Meanwhile, given the current tough operating backdrop and tariff-related ambiguity, Capital One faces headwinds in consumer spending and the auto lending business. As such, its asset quality will likely be under pressure. Also, the company spends heavily on marketing (almost 20% of the total operating expenses) and technology.

Synchrony Financial stands out by leveraging its strong distribution channel to offer a broad range of products, including private-label credit cards and dual Cards for use on MasterCard and Visa networks. It has the potential to issue dual cards for use on the American Express and Discover networks, contributing to a more profitable and resilient business model.

Further, the company has been driving growth through targeted acquisitions and strategic partnerships that enhance digital capabilities and diversify offerings. In 2024, it acquired Ally Financial’s point-of-sale financing business, Ally Lending.

Moreover, the Allegro Credit acquisition expanded its presence in audiology and dental financing, while partnerships with PayPal, Venmo, LG Electronics, Mastercard, and others modernized payment experiences. Recent expansions with Ashley, American Eagle Outfitters and an alliance with Adobe Commerce further strengthened its ecosystem and e-commerce reach. It partnered with OnePay to power a new credit card program at Walmart, offering a smarter, embedded credit experience for U.S. shoppers.

Further, Syncrony Financial has a solid balance sheet. As of Sept. 30, 2025, it had $16.2 billion in cash and cash equivalents, up 10.4% from the end of 2024. Total borrowings were $14.4 billion. Given its earnings strength and solid liquidity position, the company’s enhanced capital distribution plans look sustainable.

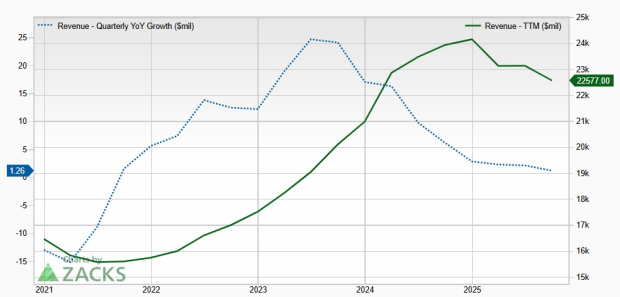

Driven by these partnerships and strategic organic and inorganic efforts, SYF’s revenues witnessed a five-year CAGR of 2.6% (ended 2024). The trend reversed in the first nine months of 2025 on a year-over-year basis due to the absence of a one-time gain recorded last year.

Synchrony Financial Revenue Trend

Management anticipates net revenues to be in the range of $15-$15.1 billion for 2025 compared with the earlier guidance of $15-$15.3 billion. This downward revision of the higher end of the guidance was on account of higher Retailer Share Arrangements (RSAs) and lower loan receivables.

Synchrony Financial’s business model exposes it to credit risk, impacting its credit quality, due to a higher allowance for loan loss, especially in an economy grappling with inflationary pressures and higher-than-normal interest rates. The lingering macroeconomic headwinds are expected to weigh on its financials to some extent.

The Zacks Consensus Estimate for COF’s 2025 and 2026 revenues implies year-over-year growth of 35.6% and 17.9%, respectively. Further, the consensus estimate for earnings indicates a 41% and 1.1% rise for 2025 and 2026, respectively. Earnings estimates for both years have been revised upward over the past week.

COF Estimate Revisions

On the contrary, analysts are slightly less bullish on Synchrony Financial’s revenue prospects. The consensus mark for the company’s 2025 and 2026 revenues indicates a year-over-year rise of 2.7% and 4.6%, respectively. The consensus estimate for earnings suggests a 37.5% and 1% surge for 2025 and 2026, respectively. Earnings estimates for 2025 were revised upward over the past week, while for 2026, the same have been revised downward.

SYF Estimate Revisions

Over the past three months, COF and SYF have risen 13.8% and 32%, respectively. Nonetheless, the weak job market and relatively higher interest rates have kept these firms under pressure, while improving clarity on tariffs and trade has offered some support.

Three-Month Price Performance

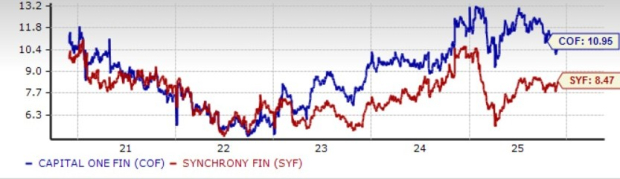

Valuation-wise, COF is currently trading at a 12-month forward price-to-earnings (P/E) of 10.95X, higher than its five-year median of 9.03X. SYF stock is currently trading at a 12-month forward P/E of 8.47X, which is also higher than its five-year median of 7.45X.

12-Month Forward P/E Ratio

While Capital One is trading at a premium to Synchrony Financial, its valuation seems justified, given its superior growth trajectory.

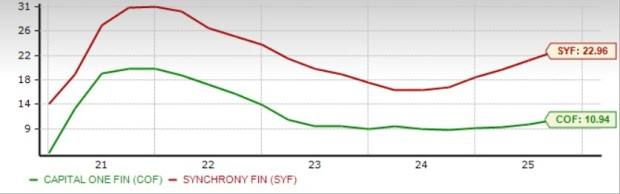

Synchrony Financial’s return on equity (ROE) of 22.96% is way above Capital One’s 10.94%. This reflects SYF’s efficient use of shareholder funds to generate profits.

Return on Equity

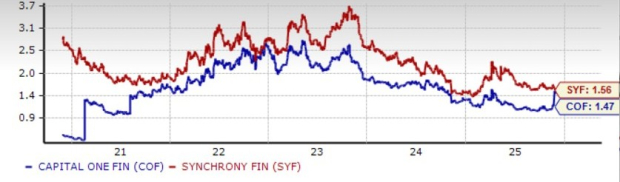

Capital One hiked its dividend by 33.3% to 80 cents per share in November 2025, while Synchrony Financial increased it in January 2025 by 20% to 30 cents per share. SYF’s dividend yield of 1.56% is slightly higher than Capital One’s 1.47%.

Dividend Yield

Capital One and Synchrony Financial are prominent U.S. credit card issuers and consumer lenders. Both are taking proactive steps to navigate the uncertain macroeconomic backdrop and relatively higher interest rates.

Synchrony Financial has a robust liquidity position and a strong distribution channel alongside diverse revenue streams. Nonetheless, higher RSAs and expenses and lower loans receivable are likely to hurt top-line growth, which is reflected in management guidance. Also, in this volatile environment, the allowance for loan losses is likely to remain elevated, impacting profitability in the near term.

On the other hand, Capital One has wrapped up one of its biggest deals this year. This, along with its strategic partnerships and higher credit card demands, is likely to support its growth. Additionally, relatively higher interest rates will continue to aid NII and NIM. Though it's trading at a premium compared with SYF, its valuation remains justified on the back of bullish analyst sentiments and growth trajectory. Thus, Capital One seems to be a better bet at the moment.

Currently, Capital One and Synchrony Financial carry a Zacks Rank #3 (Hold) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite