|

|

|

|

|||||

|

|

|

Both Skillsoft SKIL and Docusign DOCU are focusing on enterprise software and productivity. SKIL offers cloud-based learning to help organizations upskill/reskill their workforce, while DOCU provides an eSignature solution and contract lifecycle management.

We have analyzed both stocks to determine which one offers greater potential for investors.

SKIL’s top-line trajectory over the past few quarters has improved. After a 7.4% sequential dip during the first quarter of fiscal 2026, Skillsoft managed to elevate its revenues by 4%. The company’s Talent Development Solutions (TDS) remained flat at $101 million during the second quarter of fiscal 2026. It is the fourth consecutive quarter of revenue growth in its TDS Enterprise Solution, representing more than 90% of the TDS segment. The Global Knowledge segment registered $28 million in revenues, down 10% from the year-ago quarter due to lower discretionary spending in North America and geopolitical headwinds in the Middle East. However, it experienced a sequential growth of 12%.

Adjusted EBITDA margin expanded 70 basis points (bps) and 60 bps, respectively, banking on prudent expense management, operational enhancement, and efficient resource allocation. On the learning front, SKIL witnessed a 50% year-over-year rise in the number of technology learners on its platform. Furthermore, AI learners and AI learning hours surged 74% and 158% year over year, respectively.

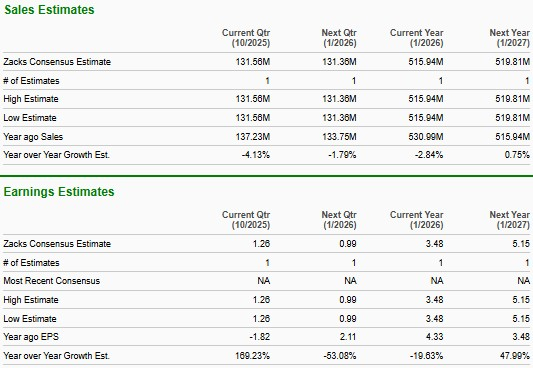

Amidst these positives, management announced a cut in the revenue outlook to $510-$530 million from the preceding fiscal quarter’s $530-$545 million, factoring in the macro and geopolitical instability. Furthermore, SKIL’s profitability position does not appear sound with a net loss of $23.8 million during the second quarter of fiscal 2026 compared with $39.6 million loss during the year-ago quarter. SKIL is operating in a domain that is already captured by well-established organizations such as Coursera and Udemy. It prompts the company to make rapid investments to gain an edge, which could potentially result in further losses, hampering its growth.

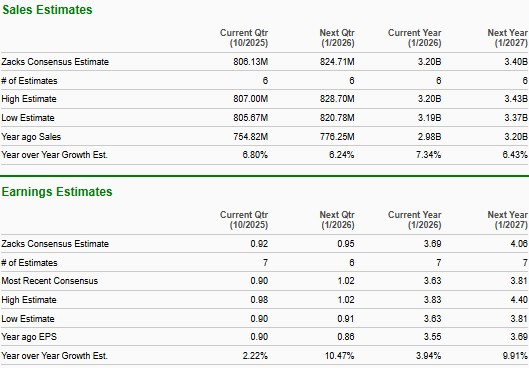

DOCU's growth trajectory is impressive in terms of its revenues increasing 9% year over year and 4.8% sequentially during the second quarter of fiscal 2026. This trend reflects a strong momentum in subscription revenues (98% of total revenues), rising 9% year over year and 5% sequentially, highlighting DOCU’s recurring revenues model’s strength and robust customer retention. It is impressive how billing climbed 13% year over year, outpacing the top line growth, reflecting strong demand, pricing power and rapid renewals. Furthermore, dollar net retention increased to 102%, solidifying the customer base retention. Banking on these optimistic performances, management hiked fiscal 2026 revenue guidance during the second quarter of fiscal 2026 to $3.189-$3.201 billion from the preceding quarter’s view of $3.151-$3.163 billion.

DOCU holds a solid balance sheet position with cash reserves of $844 million and no current debt. That being said, the company’s free cash flow generating prowess sustained across the past quarters, with $218 million secured during the second quarter of fiscal 2026. A substantial war chest, combined with a negligible short-term debt positions, enables the company to pivot to Intelligent Agreement Management (IAM) and build a future revenue pipeline from multi-year deals.

However, several challenges affect DOCU’s growth potential. Despite a robust top-line growth, the company struggled to attain margin efficiency during the second quarter of fiscal 2026. A 20-bps decline in adjusted gross margin and a 240-bps drop in adjusted operating margin raise questions on sustainable profitability. The company can experience further margin compression if it meets with execution hurdles while scaling IAM globally. This apparent risk is further magnified when competition from platform giants such as Adobe Acrobat Sign is an added variable.

The Zacks Consensus Estimate for SKIL’s fiscal 2026 sales and EPS shows a year-over-year decline of 2.8% and 19.6%, respectively. Two estimates for 2025 have increased over the past 60 days, with no downward revisions. There has been no change in analyst estimates or revisions lately.

The Zacks Consensus Estimate for DOCU’s fiscal 2026 sales and EPS indicates a year-over-year increase of 7.3% and 3.9%, respectively. Two estimates for 2025 have moved north in the past 60 days, with no southward revision. There has been no change in analyst estimates or revisions lately.

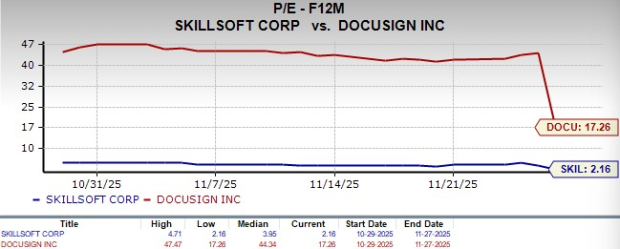

Skillsoft is trading at a 12-month forward price-to-earnings ratio of 2.16, which is lower than its 12-month median of 3.95. Docusign’s 12-month forward price-to-earnings ratio is 17.26, below its median of 44.34. SKIL appears undervalued compared to DOCU.

Both Skillsoft and Docusign paint compelling growth narratives. SKIL displays consistent growth in its business line, expanded margins, and robust momentum in AI learning. Similarly, DOCU’s heightened customer retention propels its top line, and a strong balance sheet position provides substantial leverage in its strategic pivot to IAM.

We anticipate SKIL to offer investors a better growth potential due to its undervaluation, which offers the potential for capital appreciation in the long run, offering a margin of safety that lowers downside risks.

DOCU and SKIL carry a Zacks Rank #3 (Hold) each, at present. You can see the complete list of today’s Zacks #1 Rank (STrong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-08 | |

| Jul-06 | |

| Jul-01 | |

| Jun-24 | |

| Jun-23 | |

| Jun-18 | |

| Jun-17 | |

| Jun-12 | |

| Jun-10 | |

| Jun-10 | |

| Jun-09 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 | |

| Jun-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite