|

|

|

|

|||||

|

|

|

PepsiCo Inc.’s PEP flagship U.S.-Canada beverage arm — PepsiCo Beverages North America (“PBNA”) — spans carbonated soft drinks, functional hydration, sports nutrition, modern soda, coffee, tea and away-from-home channels. As one of PepsiCo’s most strategically important businesses, PBNA plays a pivotal role in driving brand equity and profitability. Its scale, innovation pipeline and distribution muscle make it central to PepsiCo’s long-term margin expansion goals.

In third-quarter 2025, PBNA delivered 2% year-over-year organic revenue growth despite a three-point volume drag from the transition of its case-pack water business to a third party. The segment’s third-quarter performance showed renewed momentum in core brands, with Trademark Pepsi posting volume and net revenue gains, fueled by Pepsi Zero Sugar and successful marketing campaigns.

Mountain Dew flavor extensions revived engagement, while poppi delivered more than 50% retail sales growth year to date. Propel continued to scale, on track to exceed $1 billion in annual retail sales, and PBNA also gained share in enhanced water and energy through expanded partnerships, including its new distribution role for Celsius-owned brands.

PepsiCo outlined a robust plan to accelerate PBNA’s growth, expanding zero-sugar offerings, scaling functional innovations like protein-infused beverages and pushing further into away-from-home channels. On the cost side, PBNA is mitigating higher supply-chain expenses through productivity initiatives, improved logistics and SKU reductions. Since 2022, the company has cut more than 35% of SKUs, reducing complexity and sharpening in-market execution.

Given these actions, PBNA appears to be on a credible path toward its mid-teens operating margin ambition. Execution risks remain, particularly inflation in global inputs and consumer price sensitivity, but third-quarter trends and structural initiatives indicate meaningful progress. If innovation traction continues and cost efficiencies scale as planned, PepsiCo has a viable line of sight to achieving its PBNA margin target by 2026.

PepsiCo’s beverage rivals, The Coca-Cola Company KO and Monster Beverage Corporation MNST, each entered 2025 with bold performance goals, but are they executing well enough to stay on track with their targets?

Coca-Cola’s beverage business appears on track with its global growth goals, supported by high-end organic revenue growth, consistent value-share gains and improving execution across markets. Management highlighted resilient demand, strong innovation contributions and expanded operating margins despite currency headwinds. With continued investment in marketing, affordability, premiumization and system capabilities, KO expects to deliver its 2025 guidance and remains confident in achieving long-term commitments.

MNST’s beverage business remains firmly on track with its global growth targets, delivering 16.8% net sales growth and record profits, while international markets climbed to 43% of the total sales, the highest ever for the company. Strong momentum across EMEA, APAC and LatAm, combined with robust innovation, rising household penetration and successful zero-sugar extensions, continues to fuel share gains. Management remains optimistic about sustained category expansion and Monster Beverage’s ability to outperform globally.

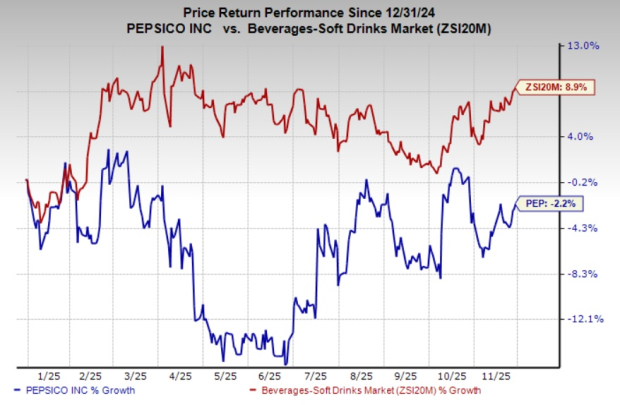

Shares of PepsiCo have lost 2.2% in the year-to-date period against the industry’s growth of 8.9%.

From a valuation standpoint, PEP trades at a forward price-to-earnings ratio of 17.42X, below the industry’s average of 18.2X.

The Zacks Consensus Estimate for PEP’s 2025 earnings implies a year-over-year decline of 0.7%, whereas its 2026 earnings estimates indicate growth of 5.9%. The company’s EPS estimates for 2025 have risen by a penny, whereas 2026 estimates have increased 0.2% in the past 30 days.

PEP currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite