|

|

|

|

|||||

|

|

|

As Dollar General Corporation DG prepares to release its third-quarter fiscal 2025 earnings results on Dec. 4, before the opening bell, investors will be closely watching customer traffic, same-store sales trends, inventory levels and margins for signs of continued momentum.

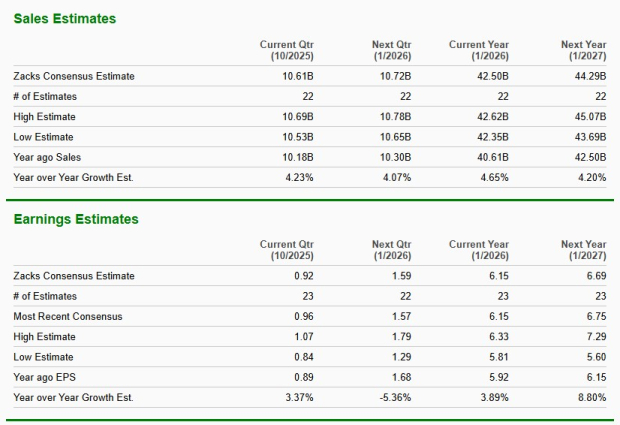

DG is expected to post growth in both revenues and earnings. The Zacks Consensus Estimate for revenues stands at $10.61 billion, calling for a 4.2% increase from the same quarter last year. While the consensus estimate for earnings has edged down by a penny over the past 30 days to 92 cents a share, it still indicates a 3.4% rise compared with the year-ago period.

Dollar General has a trailing four-quarter earnings surprise of 11.3%, on average. In the last reported quarter, the company’s bottom line beat the Zacks Consensus Estimate by a margin of 19.2%.

Dollar General Corporation price-consensus-eps-surprise-chart | Dollar General Corporation Quote

As investors prepare for Dollar General's third-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts that an earnings beat is likely for Dollar General this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Dollar General has an Earnings ESP of +3.35% and carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Dollar General’s third-quarter performance is likely to have benefited from continued strength across both consumables and key non-consumable categories. DG’s extensive footprint in rural and underserved markets, as well as its everyday low-price model, positions it to capture both a low-income customer base and higher-income consumers trading down from premium and mass-market retailers owing to underlying inflationary pressure. This shift in shopping behavior is likely to have driven same-store sales growth. We expect the metric to increase 2.3% in the third quarter.

Furthermore, operational improvements from the "Back to Basics" program, including better in-store execution and inventory management, should have contributed to top-line growth. Dollar General has been disciplined in its brick-and-mortar growth, focusing on new store openings and the high-return Project Renovate and Project Elevate remodels, which provide a same-store sales lift across its mature store base. Moreover, the acceleration of its digital and delivery initiatives, with platforms like DoorDash and Uber Eats, broadens the addressable market.

Supporting bottom-line growth is Dollar General’s margin-driving initiatives. Management has been focusing on lowering shrink, which was a substantial tailwind in the preceding quarter. Further shrink reduction would have boosted gross margin in the third quarter. Our model predicts gross margin expansion of 80 basis points in the quarter under review. Additionally, the scaling of the DG Media Network provides an attractive, high-margin revenue stream.

Despite the aforementioned favorable factors, the quarter's performance is likely to have faced headwinds from SG&A pressure and the ongoing mix shift toward low-margin consumables. Operating expenses may have seen deleverage due to planned elevated costs, including investments in retail labor to improve store execution and higher depreciation expenses stemming from the accelerated remodel and new store activity. We expect SG&A expenses as a percentage of net sales to deleverage 90 basis points.

Shares of Dollar General have rallied 38.3% in the past year against the industry’s decline of 0.1%. While DG has outpaced key competitors, including Target Corporation TGT and Costco Wholesale Corporation COST, it has underperformed Dollar Tree, Inc. DLTR. Shares of Dollar Tree have seen a gain of 46.9%, while Costco and Target have declined 7.1% and 30.5%, respectively, during the same period.

Dollar General is currently trading at a forward 12-month price-to-earnings (P/E) ratio of 16.57. This valuation reflects a discount compared to the industry’s average of 30.06 and the S&P 500's P/E of 23.41. However, the stock appears overvalued compared to its median P/E level of 15.91, observed over the past year.

Dollar General is trading at a premium to Target (with a forward 12-month P/E ratio of 11.90) but at a discount to Dollar Tree (17.46) and Costco (44.65).

As Dollar General approaches its third-quarter earnings announcement, it is supported by its value-seeking consumers and initiatives such as 'Back to Basics' operational improvements, remodel programs and digital expansion. These efforts, combined with expected margin gains from ongoing shrink reduction and the growing contribution of its high-margin media business, create a constructive backdrop that helps offset lingering cost pressures. Cumulatively, these raise DG’s probability of delivering an earnings beat.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 9 hours | |

| 12 hours | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite