|

|

|

|

|||||

|

|

|

Western Digital Corporation WDC is delivering strong gross margin expansion, driven by a favorable product mix, healthy pricing dynamics, disciplined cost controls and improved operational efficiencies, which continued in its first-quarter fiscal 2026. In the first quarter, the company reported a non-GAAP gross margin of 43.9%, representing a sharp improvement of 660 basis points (bps) year over year and 260 bps sequentially.

A key driver of this margin strength is the accelerating transition toward higher-capacity nearline hard disk drives (HDDs), particularly advanced ePMR and UltraSMR products. The company shipped 204 exabytes of storage to customers, up 23% year over year, during the fiscal first quarter. The accelerating adoption of AI and data-intensive workloads among hyperscale customers is driving robust demand for its solutions. Customers continue to migrate toward higher-capacity drives, with shipments of the company’s latest ePMR products—offering capacities of up to 26TB CMR and 32TB UltraSMR— exceeding 2.2 million units in the September quarter. The reliability, scalability and TCO benefits of its ePMR and UltraSMR technologies remain key to its success in the data center market.

Western Digital plans to build on this momentum with its next-generation HAMR drives. All of its top seven customers have placed purchase orders extending through the first half of 2026, with five committing through year-end and one major hyperscale customer securing supply through 2027. Meanwhile, its next-gen ePMR drives are set to complete qualification by early 2026, ensuring a smooth and cost-effective transition to HAMR. For the second quarter of fiscal 2026, management expects continued revenue growth, supported by sustained data-center demand and improving profitability driven by increased adoption of high-capacity drives.

Apart from this, pricing conditions have been supportive. Western Digital noted modest low-single-digit increases in ASP per terabyte on both a sequential and year-over-year basis. Moreover, cost discipline and operational execution further underpin the margin expansion. In the last earnings call, management highlighted that the company continues to realize mid- to high-single-digit cost reductions per terabyte.

For second-quarter fiscal 2026, Western Digital expects non-GAAP gross margin in the range of 44-45%, implying further sequential improvement from the first-quarter level. Non-GAAP operating expenses are expected to decline sequentially between $365 million and $375 million. The company anticipates non-GAAP revenues of $2.9 billion (+/- $100 million) at the mid-point of its guidance, up 20% year over year. Management projects non-GAAP earnings of $1.88 (+/- 15 cents).

Seagate Technology Holdings plc STX is gaining from strong global cloud demand and rapid growth in high-capacity HAMR drive adoption, with cloud demand and improving enterprise OEM trends expected to continue. The data center generates a lion’s share of the company’s revenues, and we project it to reach $8.6B in fiscal 2026. High-capacity nearline production is largely booked through 2026, with long-term contracts providing strong demand visibility through 2027. In first-quarter fiscal 2026, non-GAAP gross margin reached a record 40.1%, rising about 220 basis points (bps) quarter over quarter and roughly 680 bps year over year, driven by stronger adoption of Seagate's high-capacity nearline products and continued pricing initiatives. Non-GAAP operating margin increased 860 bps year over year to 29%. For the fiscal second quarter, non-GAAP operating margin is projected to increase to approximately 30%, at the midpoint of revenue guidance.

Micron Technology MU is benefiting from the rapidly expanding AI-driven memory and storage markets. The positive impacts of inventory improvement across multiple end markets are driving top-line growth. The surging demand for HBM and robust DRAM pricing recovery will aid significant revenue and earnings growth in the coming quarters. In fourth-quarter fiscal 2025, the non-GAAP gross margin of 45.7% improved from the year-ago quarter’s 36.5%. The non-GAAP gross margin increased 670 basis points from the previous quarter’s 39%. For the first quarter of fiscal 2026, MU projects a non-GAAP gross margin of 51.5% (+/-100 basis points).

In the past six months, shares of WDC have surged 194.3% compared with the Zacks Computer-Storage Devices industry’s growth of 72.4%.

In terms of forward price/earnings, WDC shares are trading at 20.23X, higher than the industry’s 18.69X.

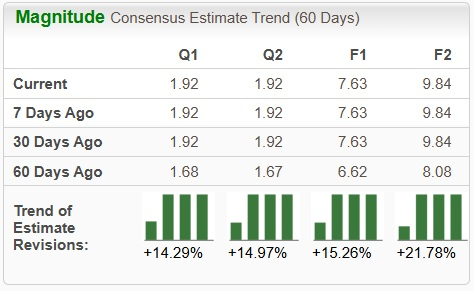

The Zacks Consensus Estimate for WDC’s earnings for fiscal 2026 has been revised upward by 15.3% to $7.63 over the past 60 days.

Currently, Western Digital sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 54 min |

Micron Stock Sell-Off Presents A Strategy That Could Return 32% In Weeks

MU

Investor's Business Daily

|

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 11 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 |

Micron giving thousands of young New Yorkers $250 for Trump accounts

MU +12.17%

Watertown Daily Times, N.Y.

|

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite