|

|

|

|

|||||

|

|

|

Dutch Bros Inc. BROS has built a reputation as one of the fastest-growing beverage concepts in the United States, but the key question for investors is whether that momentum can hold as store openings ramp up. Insights from the company’s third-quarter 2025 earnings call suggest the growth engine remains intact, even as scale increases.

The foundation of Dutch Bros’ growth is strong transaction momentum. In third-quarter 2025, the company delivered its fifth straight quarter of transaction growth, supported by mid-single-digit same-shop sales gains. Management emphasized that growth was not driven by pricing alone, but by higher customer traffic across dayparts, indicating genuine demand rather than inflation-driven sales.

Store expansion is accelerating, with plans to open roughly 175 new system shops in 2026 and a long-term target of more than 2,000 locations by 2029. Importantly, new shops are producing record average unit volumes, suggesting that newer markets in the Midwest and Southeast are responding just as positively as legacy regions. This consistency reduces the risk that growth slows simply due to geographic expansion.

Digital and loyalty initiatives further strengthen scalability. Order Ahead now accounts for a growing share of transactions, while the Dutch Rewards program drives more than 70% of system transactions. These tools help manage throughput, personalize marketing, and maintain engagement even as the footprint widens.

There are challenges ahead, including higher coffee costs and incremental labor investments tied to growth. However, management believes disciplined execution, strong four-wall economics and a deep development pipeline position Dutch Bros to sustain its growth edge, even as expansion accelerates.

Shares of Dutch Bros have lost 7.3% in the past six months compared with the 3.8% decline in the industry. In the same time frame, shares of other industry players like Starbucks Corporation SBUX, Sweetgreen, Inc. SG and Chipotle Mexican Grill, Inc. CMG have plunged 7.7%, 47.4% and 31.6%, respectively.

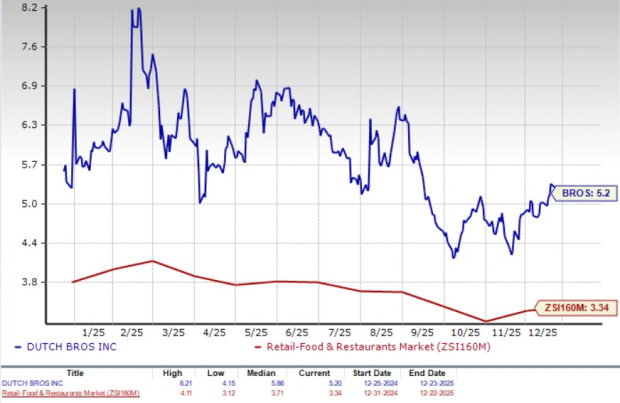

From a valuation standpoint, BROS trades at a forward price-to-sales (P/S) multiple of 5.2, above the industry’s average of 3.34. Conversely, industry players, such as Starbucks, Sweetgreen and Chipotle, have P/S multiples of 2.44, 1.02 and 3.82, respectively.

The Zacks Consensus Estimate for BROS’ 2026 earnings per share has increased to 88 cents in the past 30 days.

The company is likely to report strong earnings, with projections indicating a 29.8% rise in 2026. Conversely, industry players like Sweetgreen and Chipotle expect 2026 earnings to increase 15.5% and 4.5%, respectively, year over year. Meanwhile, Starbucks' fiscal 2026 earnings are likely to witness a rise of 10.3% year over year.

BROS stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite