|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

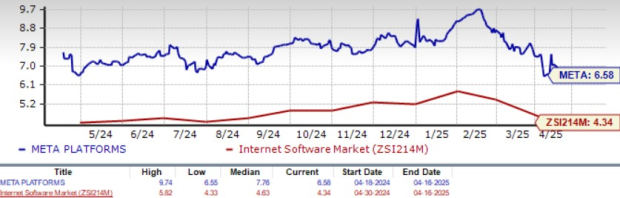

Meta Platforms META shares have dropped 13.7% in the past month, underperforming the Zacks Internet Software industry’s fall of 10.5% and the Zacks Computer & Technology sector’s decline of 7.9% over the same time frame.

The dip can be attributed to challenging macroeconomic conditions. U.S. President Donald Trump’s decision to levy tariffs on trade partners, including China, Mexico and Canada, has negatively impacted technology stocks’ prospects, including META. Higher tariffs are expected to hurt the digital advertising domain, currently dominated by Meta Platforms, Alphabet GOOGL and Amazon AMZN. These three are expected to absorb roughly 50% of the projected global ad spending by 2028.

However, higher tariffs and a prolonged trade war have the potential to hurt digital advertising spending, which doesn’t bode well for Meta Platforms. The company generates more than 90% of its revenues from advertising. Although tariffs will somewhat dent Alphabet and Amazon’s prospects, their dependence on advertising is much lower compared with META. Both Amazon and Alphabet offer cloud computing services that are expected to provide a cushion to AMZN’s and GOOGL’s prospects in the near term.

Since the Liberation Day tariff announcement on April 2, Meta Platforms shares have dropped 14%, underperforming Alphabet’s fall of 2.1% and Amazon’s drop of 11.2%.

So, what should investors do with the Meta Platforms stock on the backdrop of tariffs and increasing chances of a recession? Let’s dig deep to find out.

Meta Platforms’ focus on leveraging AI to improve user engagement has been a key catalyst. AI is heavily dependent on data, of which META has a trove, driven by its more than 3.35 billion daily users. Meta AI usage continues to increase, with more than 700 million monthly actives. The company’s initiative to add updates that will help Meta AI deliver more personalized and relevant responses is expected to boost engagement.

META’s decision to loosen control over content monitoring is expected to further boost user engagement. The Community Notes program replaces META’s third-party fact-checking program in the United States to promote more free speech across its platforms, Facebook, Instagram and Threads.

Meta Platforms focuses on improving advertisers’ return on ad spending. Its proprietary machine learning system, Andromeda, for retrieval in ad recommendation is powered by NVIDIA NVDA. The deployment of META’s deep neural network on the NVIDIA Grace Hopper Superchip across Instagram and Facebook applications has achieved more than 6% recall improvement to the retrieval system while delivering over 8% ad quality improvement on selected segments.

META’s growing focus on social commerce through Facebook, Instagram and WhatsApp is noteworthy. Meta Verified on Instagram, Facebook and WhatsApp is a popular initiative under which the company offers four subscription plans to help businesses build credibility. All plans include the verified badge, account support and impersonation protection. This boosts consumer trust and attracts new businesses to the platforms.

The Zacks Consensus Estimate for first-quarter 2025 earnings is pegged at $5.22 per share, down by 1.8% over the past 30 days, indicating a 10.83% year-over-year increase.

Meta Platforms, Inc. price-consensus-chart | Meta Platforms, Inc. Quote

META’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 13.77%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

However, META stock is not so cheap, as the Value Score of C suggests a stretched valuation at this moment.

In terms of the forward 12-month Price/Sales, META is trading at 7.9X, higher than its median of 7.83X and the broader sector’s 5.81X.

AI usage is making META a popular name among advertisers as well as users. However, Meta Platforms’ first-quarter 2025 results are expected to suffer from unfavorable forex (3% headwind to total revenue growth on a year-over-year basis).

Operating expenses are expected in the $114-$119 billion range, with headcount expected to increase within infrastructure, monetization, Reality Labs, Generative AI, regulations and compliance. Regulatory concerns in the United States and Europe, along with tariffs, make the stock a risky bet.

META is spending heavily on expanding AI infrastructure. For 2025, capital expenditure is expected between $60 billion and $65 billion, driven by its Gen AI initiatives and core business.

Although this bodes well for the company’s longer-term prospects, we believe the lack of monetization of new platforms like Threads is a concern.

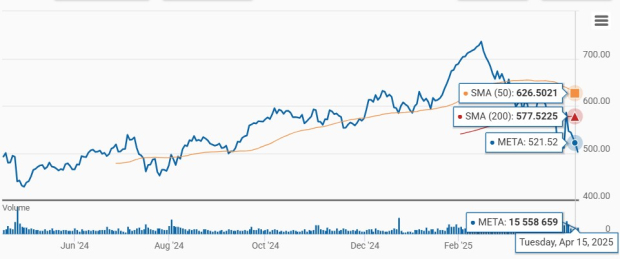

META shares are trading below the 50-day moving average, indicating a bearish trend.

META currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 14 min | |

| 16 min | |

| 34 min | |

| 39 min | |

| 46 min | |

| 57 min | |

| 58 min | |

| 58 min | |

| 58 min | |

| 58 min | |

| 58 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite