|

|

|

|

|||||

|

|

|

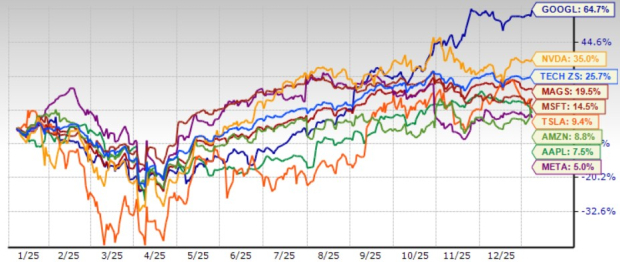

Alphabet GOOGL shares have jumped 64.7% in a year, making GOOGL the best-performing stock among the Magnificent 7 group. The shares have outperformed the Roundhill Magnificent Seven ETF (MAGS) that provides focused, equal-weight exposure to the Magnificent 7 stocks: Amazon AMZN, Apple AAPL, Meta Platforms, Microsoft MSFT, Nvidia, Tesla and Alphabet. While MAGS returned 19.5% in the trailing 12-month period, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla appreciating 8.8%, 7.5%, 5%, 14.5%, 35% and 9.4%, respectively.

GOOGL shares have outperformed the Zacks Computer and Technology sector, which appreciated 25.7% over the same timeframe. GOOGL’s outperformance can be attributed to its continuing AI push across its search, YouTube, and cloud computing platforms. An expanding focus on improving enterprise footprint is expected to boost prospects amid stiff competition in the cloud computing domain from the likes of Microsoft and Amazon. However, stiff competition along with Google Cloud’s capacity constraints and an uncertain macroeconomic environment has the potential to hamper prospects.

A Value Score of D suggests a premium valuation for Alphabet at this moment. GOOGL stock is overvalued, with a forward 12-month price/sales of 9.93X compared with the sector’s 7.45X and Apple's 8.32X.

Google continues to dominate the Search business with a roughly 90.83% share, followed by Microsoft’s Bing, with a 4.03% share, per the latest data from StatCounter. The company has been actively embedding AI, especially within Search, to enhance user experience, provide better AI-focused features and consequently improve ad performance. AI Overviews and AI Mode are driving overall queries and commercial queries, thereby driving monetization opportunities. The addition of shopping capabilities in AI Mode is now helping people shop conversationally in Search. Google has added new AI features in Search that help users build travel plans.

AI Max is helping businesses identify new customers by delivering the most relevant ad across surfaces. It is also expanding the reach and accessibility of advertisers by matching them against additional queries. GOOGL continues to infuse Generative AI (Gen AI) capabilities at every step of the marketing process. The availability of Imagen 4 in Asset Studio and Product Studio is helping businesses produce more and better creatives.

In November, Alphabet launched Gemini 3, its latest state-of-the-art reasoning model. It now powers Search, via AI Mode. Google AI Pro and Ultra subscribers in nearly 120 countries and territories in English can use Gemini 3 Pro by selecting “Thinking with 3 Pro” from the model drop-down menu in AI Mode. Introduction of Veo 3.1 and Veo 3.1 models in the Gemini API, Nano Banana Pro, and Gemini 3 Flash are noteworthy developments that are expected to boost Alphabet’s prospects in 2026.

Google Cloud is benefiting from Gen AI adoption due to leading models, including Gemini, Imagen, Veo, Chirp and Lyria. Gemini Enterprise is gaining adoption with more than two million subscribers across 700 companies. Alphabet’s expanding AI infrastructure is helping it win enterprise clients. GCP’s prospects remain robust, driven by strong demand for enterprise AI infrastructure, including TPUs and GPUs, enterprise AI solutions driven by demand for the latest Gemini and other AI models, and other services, including cybersecurity and data analytics.

The Zacks Consensus Estimate for 2025 earnings is pegged at $10.58 per share, up by 0.7% over the past 30 days, indicating 31.6% year-over-year growth. The consensus mark for 2025 revenues is pegged at $340.26 billion, indicating 15.3% year-over-year growth.

Alphabet Inc. price-consensus-chart | Alphabet Inc. Quote

The consensus mark for 2026 earnings is pegged at $11.04 per share, up 0.5% over the past 30 days, suggesting 4.34% growth from the 2025’s estimated consensus figure. The Zacks Consensus Estimate for 2026 revenues is pegged at $390.18 billion, implying 14.7% growth from 2025’s estimated figure.

Alphabet’s growing AI-powered search capabilities and significant investments in cloud computing bode well for its prospects next year. GOOGL expects capital expenditure between $91 billion and $93 billion for 2025, which is anticipated to increase further in 2026.

However, capacity constraints, despite the improving pace of server deployments and data center construction, are expected to hurt Alphabet’s prospects in 2026. This, along with higher depreciation expenses and related data center operations costs, including energy, is expected to hurt profitability. Higher sales and marketing expenses are expected to keep the margins under pressure. These factors, along with GOOGL’s premium valuation, are concerning for investors in the near term.

Alphabet currently has a Zacks Rank #3 (Hold), suggesting that investors should wait for a more favorable point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 5 hours | |

| 6 hours | |

| 13 hours | |

| 14 hours | |

| 14 hours |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| 14 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite