|

|

|

|

|||||

|

|

|

Helen of Troy Limited (HELE) reported mixed third-quarter fiscal 2026 results, with the top line beating the Zacks Consensus Estimate and the bottom line matching the same. Both net sales and earnings experienced year-over-year declines.

The company saw growth across select core brands, including OXO, Osprey and Olive & June, alongside an expansion in organic direct-to-consumer sales. Management indicated a renewed focus on consumer-centric priorities, including product innovation, brand engagement and commercial discipline, which it believes should help stabilize operations and support longer-term growth.

Helen of Troy Limited price-consensus-eps-surprise-chart | Helen of Troy Limited Quote

Helen of Troy posted adjusted earnings of $1.71 per share, which was in line with the Zacks Consensus Estimate. The bottom line declined 36% from $2.67 reported in the year-ago period due to lower adjusted operating income and elevated interest expense. These were partly offset by a reduction in adjusted income tax expense.

HELE reported net sales of $512.8 million, which beat the Zacks Consensus Estimate of $505 million. The top line decreased 3.4% from $530.7 million posted in the year-ago period. This decline was caused by a $57.1 million or 10.8% decrease in Organic business. The decline reflected weaker demand for insulated beverageware, hair appliances, prestige hair care products, thermometers, humidifiers and water filtration products. The decrease in Organic sales was partially offset by a $37.7 million or 7.1% contribution from the acquisition of Olive & June and strong demand for travel, technical and lifestyle packs within the Home & Outdoor segment.

International sales fell 8.1% to $119.6 million, due to evolving market dynamics in China.

The consolidated gross profit margin contracted 200 basis points (bps) to 46.9% compared with 48.9% in the prior year. The decrease was primarily caused by the adverse impact of higher tariffs and a less favorable year-over-year inventory obsolescence impact. These factors were partially offset by the positive impact of the Olive & June acquisition and lower commodity and product costs. We estimated a 47.2% gross margin.

The consolidated SG&A ratio increased 160 bps to 35.6% due to higher annual incentive compensation expense, increased outbound freight costs, the impact of the Olive & June acquisition and unfavorable operating leverage resulting from lower net sales.

The adjusted operating income declined 24.6% to $66.3 million, while the adjusted operating margin decreased 370 bps to 12.9%. We expected an adjusted operating margin of 13.2% for the quarter.

Net sales in the Home & Outdoor segment declined 6.7% to $229.6 million, primarily due to competitive pressures, lower retailer replenishment amid softer demand and reduced club, online and closeout channel sales. These headwinds were partially offset by tariff-related price increases, strong demand for travel and lifestyle packs, solid holiday-driven brick-and-mortar sales and new insulated beverageware launches.

Net sales in the Beauty & Wellness segment fell 0.5% to $283.2 million due to a $39.7 million, or 13.9%, drop in Organic business sales. This was primarily due to softer consumer demand and heightened competition in the Beauty category, tariff-related disruptions in China and a weaker illness season. These declines were partially offset by a $37.7 million, or 13.2%, contribution from the acquisition of Olive & June.

Helen of Troy ended the fiscal third quarter with cash and cash equivalents of $27.1 million and total short and long-term debt of $892.4 million. Net cash provided by operating activities for the first nine months of fiscal 2026 was $59.8 million. The free cash flow for the same period was $28.8 million.

The company now expects fiscal 2026 consolidated net sales revenues to be between $1.76 billion and $1.77 billion compared with its prior outlook of $1.74 billion to $1.78 billion.

By segment, Home & Outdoor net sales are projected to be between $812 million and $819 million, while Beauty & Wellness net sales are expected to range from $946 million to $954 million, including an incremental contribution of $106 million to $109 million from the Olive & June acquisition.

The sales outlook indicates the company’s expectation of continued softness in consumer spending, particularly in discretionary categories, along with heightened macroeconomic uncertainty, a more promotional retail environment and increasing consumer strain.

Management now anticipates fiscal 2026 GAAP loss per share of $35.57 to $36.07 and adjusted EPS to range from $3.25 to $3.75. Previously, the company expected fiscal 2026 GAAP loss per share to be in the range of $29.40 to $29.90 and adjusted EPS between $3.75 and $4.25.

Headwinds include pressures from a more promotional retail environment and continued consumer trade-down behavior, and lower gross margin caused by higher tariffs, weaker-than-expected retail price realization and an unfavorable product mix resulting from selective pricing actions. The outlook also incorporates the company’s decision to preserve key growth investments to support its workforce, future revenue expansion and new product development, along with higher year-over-year incentive compensation expense and the impact of unfavorable operating leverage stemming from lower revenues.

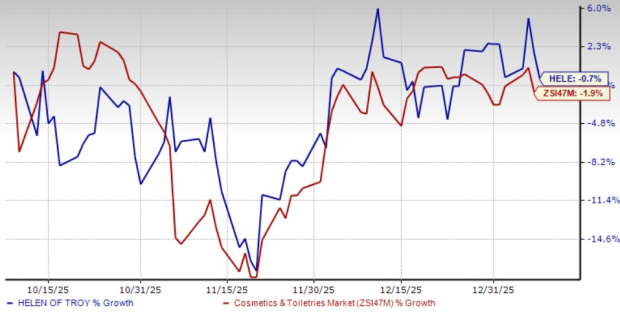

This Zacks Rank #3 (Hold) company has lost 0.7% in the past three months compared with the industry’s decline of 1.9%.

Mama's Creations, Inc. (MAMA) manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures. MAMA delivered a trailing four-quarter earnings surprise of 133.3%, on average.

The Estee Lauder Companies Inc. (EL) manufactures, markets and sells skin care, makeup, fragrance and hair care products worldwide. It holds a Zacks Rank #2 (Buy) at present. EL delivered a trailing four-quarter earnings surprise of 82.6%, on average.

The Zacks Consensus Estimate for Estee Lauder’s current fiscal-year sales and earnings implies growth of 4.6% and 43.1%, respectively, from the year-ago figures.

McCormick & Company, Incorporated (MKC) manufactures, markets and distributes spices, seasoning mixes, condiments and other flavorful products to the food industry. It holds a Zacks Rank #2 at present. MKC delivered a trailing four-quarter earnings surprise of 2.2%, on average.

The Zacks Consensus Estimate for McCormick’s current fiscal-year sales and earnings implies growth of 1.6% and 2.4%, respectively, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-10 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-08 | |

| Jul-02 | |

| Jul-01 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite