|

|

|

|

|||||

|

|

|

Microsoft MSFT shares are gaining momentum as Office 365 subscription metrics signal accelerating demand across both commercial and consumer segments. The company's fiscal first-quarter 2026 results revealed Microsoft 365 Commercial cloud revenues advancing 17% while seat growth expanded 6%, driven primarily by small and medium-sized businesses alongside frontline worker deployments. This dual expansion of both users and revenue per user suggests the platform is successfully monetizing its installed base through higher-tier offerings.

The growth story extends beyond commercial markets. Microsoft 365 Consumer cloud revenues surged 26% as subscriptions climbed 7% to surpass 90 million, reflecting sustained traction in the personal productivity space. Revenue per user gains across both segments stemmed largely from Microsoft 365 E5 adoption and the emerging Copilot AI assistant, which achieved 150 million monthly active users across the company's product family. Copilot Chat usage specifically accelerated 50% quarter over quarter, demonstrating rapid enterprise acceptance of AI-enhanced productivity tools.

Microsoft strengthened its forward revenue visibility by announcing price increases effective July 2026, with monthly fees rising upto three dollars across subscription tiers. The company simultaneously extended promotional offers through June 2026 to drive Copilot adoption during renewal cycles. With 900 million monthly active users already engaging AI features across Microsoft's ecosystem and commercial remaining performance obligations reaching $392 billion, Office 365's subscription trajectory appears positioned for sustained expansion as organizations increasingly embed AI capabilities into their productivity infrastructure.

Microsoft's Office 365 expansion contrasts with divergent subscription strategies from Apple AAPL and Alphabet GOOGL-owned Google. Apple recently crossed 1 billion total subscriptions, reporting services revenues of $26.3 billion in its latest quarter, representing 14% growth. Apple's iCloud storage remains central to productivity monetization. Google Workspace maintains eight million paying business customers alongside three billion monthly users. Google raised prices 16% in January 2025, mirroring Apple's revenue-per-user expansion approach. Google holds 50.34% market share in productivity software versus Apple's ecosystem-focused model. Both Apple and Google implemented pricing increases to boost subscription margins, though Microsoft maintains stronger commercial penetration within dedicated enterprise productivity platforms.

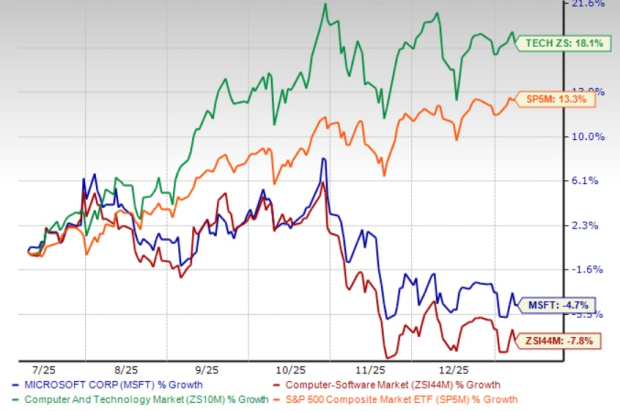

MSFT shares have lost 4.7% in the past six-month period, outperforming the Zacks Computer – Software industry's decline of 7.8% but underperforming the Zacks Computer and Technology sector's return of 18.1%.

From a valuation standpoint, MSFT stock is currently trading at a forward 12-month Price/Sales ratio of 10.5X compared with the industry’s 9.08X. MSFT has a Value Score of D.

The Zacks Consensus Estimate for MSFT’s fiscal 2026 earnings is pegged at $15.59 per share, up 0.3% over the past 30 days. The estimate indicates 14.3% year-over-year growth.

Microsoft Corporation price-consensus-chart | Microsoft Corporation Quote

Microsoft currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite