|

|

|

|

|||||

|

|

|

The Trade Desk is still growing at a market-beating pace despite its underperformance last year.

Design software giant Adobe continues to hold its own just fine against generative AI.

Digital payments processor PayPal is buying back its shares at a rapid pace.

Although growth investing has been the go-to strategy for ultimate investing returns since the artificial intelligence (AI) arms race began in 2023, it has also claimed some victims. There are several companies that are being actively disrupted, although not every one of them is an AI victim. This opens up the potential for a value investment, as these stocks have sold off below a reasonable valuation.

If you're looking to add a bit of value to your portfolio, I think investors should consider The Trade Desk (NASDAQ: TTD), Adobe (NASDAQ: ADBE), and PayPal Holding (NASDAQ: PYPL).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

The Trade Desk isn't a company that's being disrupted by artificial intelligence; it disrupted itself by deploying it! It rolled out its AI-powered ad-buying platform, Kokai, to mixed reviews. This caused some customers to leave the platform entirely and others to scale back usage. The Trade Desk is actively working on fixing this blunder, but it has taken a toll on its stock.

Additionally, Amazon has entered the advertising game and has captured a large part of the market that The Trade Desk was hoping to gain. Amazon's consumer information is far more accurate than anyone else's, as it has actual data for what consumers are shopping for.

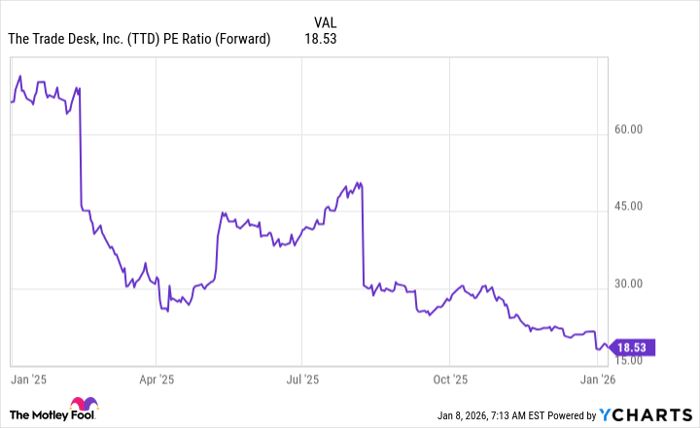

All of this has disrupted The Trade Desk's investment thesis, and its stock was one of the worst-performing S&P 500 components last year. The stock is down more than 70% from its all-time high, but investors should consider scooping up this longtime winner at a much more attractive price. The Trade Desk isn't that expensive now, trading at 18.5 times forward earnings.

TTD PE Ratio (Forward) data by YCharts. PE Ratio = price-to-earnings ratio.

For reference, the S&P 500 as a whole trades for 22.1 times forward earnings. You'd think that a company trading at a discount to the market would be growing more slowly, but that's not the case. In the third quarter, The Trade Desk's revenue rose 18% year over year. For 2026, Wall Street expects 16% growth. That's a recipe for a company that can bounce back, and it's one of my top value investments for 2026.

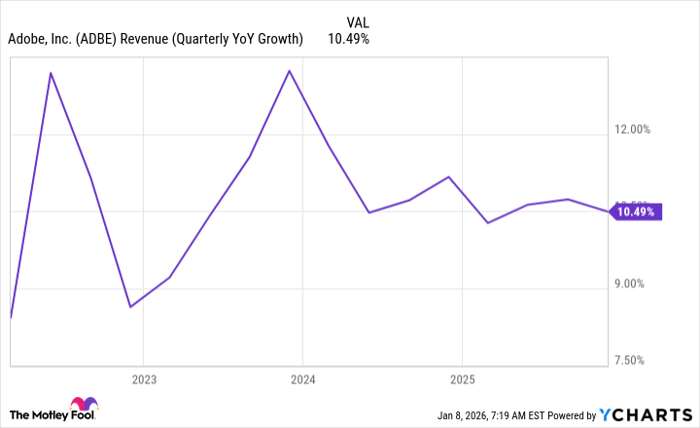

Adobe is a company that everyone is convinced will be disrupted by generative AI. With the various generative AI engines becoming more sophisticated in generating AI images, the assumption is that there won't be a need for Adobe's creative design software. However, Adobe has openly embraced the generative AI tools and has worked to integrate them into its platform.

In their eyes, there will always be a need for professionally designed images, even if they are assisted by generative AI tools. Adobe's products give the user ultimate control over the end product, which is key in shaping a brand. Since the AI revolution kicked off in 2023, Adobe's growth rates haven't really changed.

ADBE Revenue (Quarterly YoY Growth) data by YCharts. YoY = year over year.

This shows that it's doing just fine, growing even though everyone assumes that it's being disrupted. The market also has no faith in its stock, and it trades for a dirt cheap 14.4 times forward earnings. Adobe is a great value play to scoop up, and it could deliver solid returns.

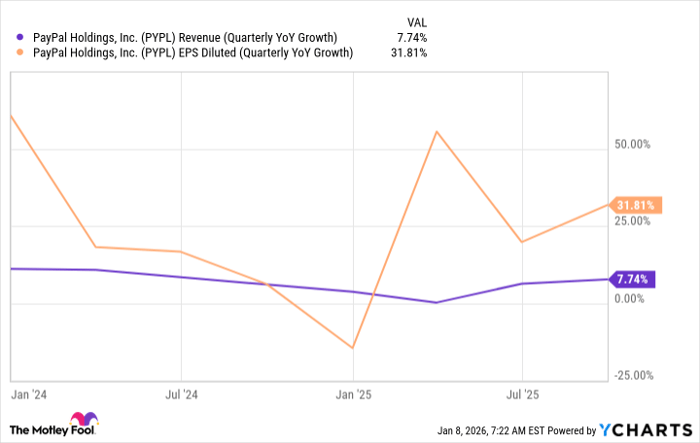

PayPal is the cheapest stock of the three, trading for just 10 times forward earnings. It is battling other payment processors and payment ecosystems to maintain its market share, and it's doing an OK job. Its growth isn't anything spectacular, but it continues to deliver mid- to high-single-digit growth each quarter.

However, PayPal is doing the smart thing and buying back all the stock it can at this depressed stock price. Because its stock is cheap, these share repurchases have an outsize effect, causing its diluted earnings per share (EPS) to rise at a much faster rate.

PYPL Revenue (Quarterly YoY Growth) data by YCharts. YoY = year over year. EPS = earnings per share.

If PayPal can keep this up, eventually it will become too cheap to ignore. As a result, I think PayPal is a great stock to buy now and wait for it to be fairly valued by the market.

Before you buy stock in The Trade Desk, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and The Trade Desk wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $482,451!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,133,229!*

Now, it’s worth noting Stock Advisor’s total average return is 968% — a market-crushing outperformance compared to 197% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 11, 2026.

Keithen Drury has positions in Adobe, Amazon, PayPal, and The Trade Desk. The Motley Fool has positions in and recommends Adobe, Amazon, PayPal, and The Trade Desk. The Motley Fool recommends the following options: long January 2027 $42.50 calls on PayPal, long January 2028 $330 calls on Adobe, short January 2028 $340 calls on Adobe, and short March 2026 $65 calls on PayPal. The Motley Fool has a disclosure policy.

| 15 hours | |

| 17 hours | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Apr-01 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-31 | |

| Mar-30 | |

| Mar-30 | |

| Mar-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite