|

|

|

|

|||||

|

|

|

Amazon’s AMZN cloud segment, Amazon Web Services (“AWS”), demonstrated resilient margin performance in the third quarter of 2025, signaling improving profitability dynamics that could drive additional stock appreciation. AWS generated operating income of $11.4 billion on revenues of $33 billion, translating to a 34.6% operating margin that reflects both robust demand and disciplined cost management.

The cloud segment's trailing 12-month operating margin reached 35.9%, stabilizing after earlier compression from heavy AI infrastructure investments. This margin trajectory appears sustainable as AWS scales its custom silicon strategy, particularly with Trainium2 chips achieving multibillion-dollar revenue status and growing 150% sequentially. The transition from training-intensive to inference-heavy workloads positions AWS to defend margins while competing aggressively on pricing.

Revenue reacceleration to 20% year-over-year growth, up from prior quarters, underscores strengthening momentum. The business added $2.1 billion in sequential revenues, reaching a $132 billion annualized run rate. More compelling is the $200 billion remaining performance obligations backlog with a 3.8-year weighted average term, providing multi-year revenue visibility.

December's re:Invent conference unveiled margin-enhancing innovations, including Trainium3 UltraServers delivering 4.4 times higher compute performance with 40% lower energy consumption, and Graviton5 processors offering superior price-performance economics. Database Savings Plans and Lambda Managed Instances further strengthen cost optimization capabilities for enterprise customers.

As AWS monetizes its substantial capacity investments while maintaining mid-30% margins, the combination of accelerating growth, expanding profitability, and visible long-term demand supports a constructive stock outlook.

Microsoft's MSFT Intelligent Cloud segment generated a 43% operating margin in the first quarter of fiscal 2026, maintaining profitability despite aggressive AI infrastructure scaling. Microsoft reported Azure revenue growth of 40% while operating income increased 27%, demonstrating the segment's ability to balance expansion with margin discipline. In contrast, Alphabet's GOOGL Google Cloud achieved a 23.7% operating margin in the third quarter of 2025, representing substantial expansion from 17.1% the prior year. Google Cloud delivered operating income of $3.6 billion, surging 85% year over year on revenue growth of 34%. While Microsoft benefits from established scale and higher baseline margins, Alphabet's Google Cloud shows an accelerating margin improvement trajectory as enterprise AI products generate billions in quarterly revenues. Both hyperscalers face elevated depreciation costs from data center buildouts, with Microsoft maintaining a superior margin structure and Google Cloud demonstrating faster margin expansion velocity.

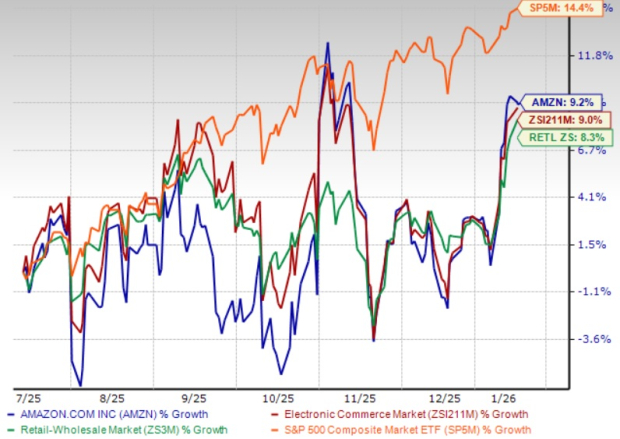

Amazon shares have returned 9.2% in the past six-month period compared with the Zacks Internet – Commerce industry and the Zacks Retail-Wholesale sector’s growth of 9% and 8.3%, respectively.

From a valuation standpoint, AMZN stock appears overvalued, trading at a forward 12-month price/earnings ratio of 31.16X, higher than the industry’s 25.64X. Amazon has a Value Score of D.

The Zacks Consensus Estimate for AMZN’s 2026 earnings is pegged at $7.85 per share, which has seen an upward revision of 0.1% over the past 60 days. This indicates a 9.46% increase from the figure reported in the year-ago quarter.

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

Amazon currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 4 hours | |

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite