|

|

|

|

|||||

|

|

|

Crown Castle Inc. CCI recently announced that it has terminated its agreement with DISH Wireless as the latter has defaulted on its payment obligations. With the exercise of its right to termination to safeguard its shareholders’ interests, CCI stands to recover more than $3.5 billion in remaining payments owed.

The dispute stems from strategic changes at DISH’s parent company, EchoStar. Last summer, Echostar announced that it was discontinuing its network business through the sale of its public spectrum licenses to AT&T and SpaceX. DISH further emphasized that, as a result of the actions taken by the Federal Communications Commission, the company is no longer obligated to honor remaining contractual payments.

While the above event is likely to impact the near-term revenues of CCI emerging from non-payment of contractual obligations, the same may not have a material impact on its long-term outlook. With DISH exiting the wireless network buildout business, the termination removes a tenant whose long-term viability had become increasingly uncertain. This frees up capacity on CCI’s towers for more creditworthy carriers, such as AT&T, Verizon and T-Mobile, which continue to invest in 5G networks.

The exponential growth in mobile data usage, higher availability of spectrum and the deployment of 5G networks at scale are driving significant network investments by carriers who aim to improve and densify their cell sites. Given Crown Castle’s unmatched portfolio of approximately 40,000 towers in each of the top 100 basic trading areas of the United States (as of the third quarter of 2025), it remains well-positioned to capitalize on this upbeat trend.

Although the DISH termination may pressure near-term revenues, it does not undermine Crown Castle’s long-term outlook, given the solid demand prospects. However, Crown Castle’s top-line growth is likely to be affected by the consolidation in the wireless industry. High customer concentration and the evolution of new technologies are other key concerns.

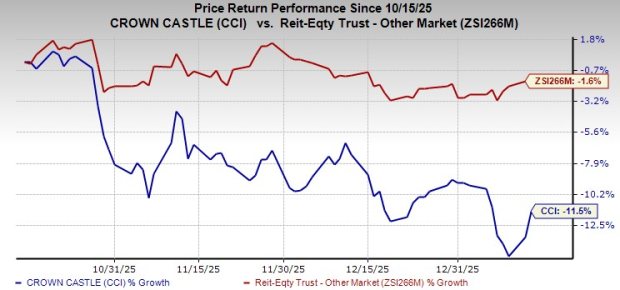

Over the past three months, shares of this Zacks Rank #4 (Sell) tower REIT have lost 11.5% compared with the industry’s fall of 1.6%.

However, analysts seem bullish on this stock, with the Zacks Consensus Estimate for 2025 FFO per share having been revised northward by 2.1% to $4.30 over the past three months. Estimates for 2026 have been moved up by 2.3% to $4.96 over the same period.

Some better-ranked stocks from the broader REIT sector are Prologis Inc. PLD and Host Hotels & Resorts HST, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for PLD’s 2025 and 2026 FFO per share is pinned at $5.80 and $6.08, respectively. This calls for year-over-year growth of 4.3% for 2025 and 4.7% for 2026.

The Zacks Consensus Estimate for HST’s 2025 and 2026 FFO per share is pegged at $2.05 and $2.04, respectively. This implies year-over-year growth of 4.1% for 2025 and a marginal fall for 2026.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-29 | |

| Jul-27 | |

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 |

Segro Shares Rise After Board Yields to Prologis's Final $18.7 Billion Takeover Bid

PLD

The Wall Street Journal

|

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite