|

|

|

|

|||||

|

|

|

PPL Corp.’s PPL shares have gained 4% in the last month against the Zacks Utility-Electric Power industry’s decline of 2.6%. The company continues to provide electricity and natural gas to its 3.6 million customers across the United States. In the same period, PPL has also outperformed the Zacks Utilities sector.

PPL is steadily investing to modernize infrastructure, cut its carbon footprint and enhance service reliability. The company plans to invest about $20 billion through 2028 to reinforce its grid and reduce outage risks. In parallel, PPL is focused on lowering emissions from power generation and advancing toward a net-zero energy system by 2050.

Another utility, Xcel Energy XEL, also has a long-term investment plan to further strengthen its electric distribution and transmission operations. Last month, XEL’s shares gained 3%, outperforming its industry.

PPL is trading above its 50 and 200-day simple moving averages (SMAs), signaling a bullish trend. The company has repositioned itself as a U.S.-focused energy company after the divestiture of the international operation.

The 50 and 200-day SMAs are key indicators for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of a stock’s uptrend or downtrend.

Should you consider adding PPL to your portfolio only based on positive price movements? Let us delve deeper and find out the factors that can help investors decide whether it is a good entry point to add the PPL stock to their portfolios.

PPL’s capital strategy centers on strengthening its generation, transmission and distribution network. Ongoing upgrades have already improved reliability and reduced outages. PPL plans to invest about $20 billion from 2025 to 2028 to further enhance operations and deliver safe, reliable and high-quality service to customers.

More than 60% of PPL’s capital investment plan is subject to “contemporaneous recovery,” which reduces the impact of regulatory lag on earnings for investments. The recovery of capital expenditures quickly allows the company to fund long-term projects easily.

Following multiple rate cuts, the U.S. Federal Reserve has lowered interest rates by 175 basis points, bringing them down from the 5.25-5.50% range to the 3.50-3.75% band, with additional cuts expected in 2026. Lower borrowing costs reduce the expense of new and refinanced debt for PPL, supporting improved margins and strengthening overall financial performance.

Demand for reliable clean energy is increasing across PPL’s service territory. The company’s long-term capital investment program is positioning it to meet this growth with new generation capacity. PPL plans to deliver 7,500 MW of zero-carbon renewable generation, 3,000 MW of natural gas-fired capacity, nearly 2,000 MW of energy storage and 1,500 miles of new high-voltage transmission lines to support system reliability and rising demand.

The company is also set to benefit from its ongoing cost-reduction efforts. PPL aims to lower operating and maintenance expenses by at least $175 million by 2026 compared with its 2021 baseline. The cost management initiatives will boost the margins of the company.

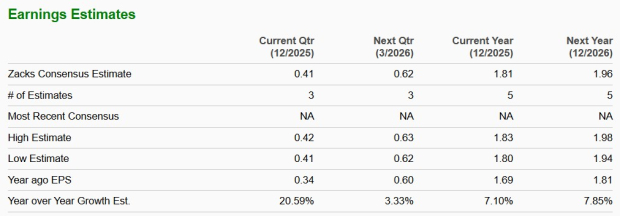

The Zacks Consensus Estimate for PPL’s earnings per share for 2026 has moved up 7.85% on the back of 5.24% year-over-year increase in sales estimates.

PPL’s long-term (three to five years) earnings growth is pegged at 7.34%.

The company has been distributing dividends to its shareholders for a long time and plans to increase dividends annually in the range of 6-8% at least through 2028, subject to the board’s approval.

PPL’s current quarterly dividend rate is 27.25 cents, resulting in an annual dividend of $1.09 per share. The current dividend yield is 3.07%, which is better than the industry’s yield of 2.77%. PPL has raised dividends for its shareholders four times in the past five years. Check PPL’s dividend history here.

Another utility, Dominion Energy D, also has a well-chalked-out capital expenditure plan to strengthen operation and boost its clean energy generation capability. Dominion Energy also pays a regular dividend to its shareholders. The current dividend yield of Dominion Energy is 4.4%, which is also better than the industry average.

Return on equity (“ROE”), a profitability measure, reflects how effectively a company is utilizing its shareholders’ funds in the operations to generate income.

PPL’s trailing 12-month ROE is 9.08%, lower than its industry’s 10.47%.

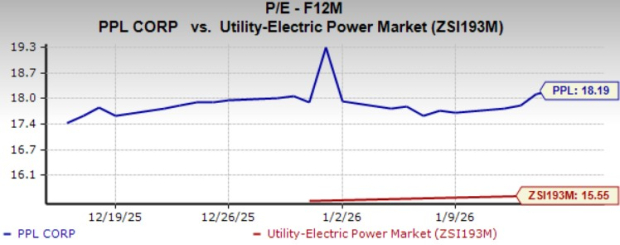

PPL is currently valued at a premium compared with its industry on a forward 12-month P/E basis. The current P/E F12M of the company is 18.19X compared with the industry’s 15.55X.

PPL is well-positioned to benefit from rising clean energy demand across its service territories and investing to expand operations accordingly. Its ability to recover more than 60% of capital expenditures in real time enhances financial flexibility and supports efficient funding of long-term projects. Lower interest rates further reduce project financing costs.

PPL also continues to create shareholder value through consistent dividend payments, while improving earnings estimates enhance its overall investment appeal.

PPL’s shares currently trade at a premium and its returns remain slightly below the industry average. So, the new investors should wait for a better entry point to add this Zacks Rank #3 (Hold) stock to their portfolio.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 |

Madison utility seeks new data center rate to shield regular customers

XEL

Milwaukee Journal Sentinel

|

| Jul-16 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 | |

| Jul-09 | |

| Jul-08 | |

| Jul-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite