|

|

|

|

|||||

|

|

|

The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Boot Barn (NYSE:BOOT) and the rest of the apparel and footwear retail stocks fared in Q3.

Apparel and footwear was once a category thought to be relatively safe from major e-commerce penetration because of the need to try on, touch, and feel products, but the category is now meaningfully transacted online. Everyone still needs clothes and shoes to go outside unless they want some curious (or horrified) looks. But this ongoing digitization is forcing apparel and footwear retailers–that once only had brick-and-mortar stores–to respond with omnichannel offerings. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stagnate, so the evolution of clothing and shoes sellers marches on.

The 12 apparel and footwear retail stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was in line.

Luckily, apparel and footwear retail stocks have performed well with share prices up 17.9% on average since the latest earnings results.

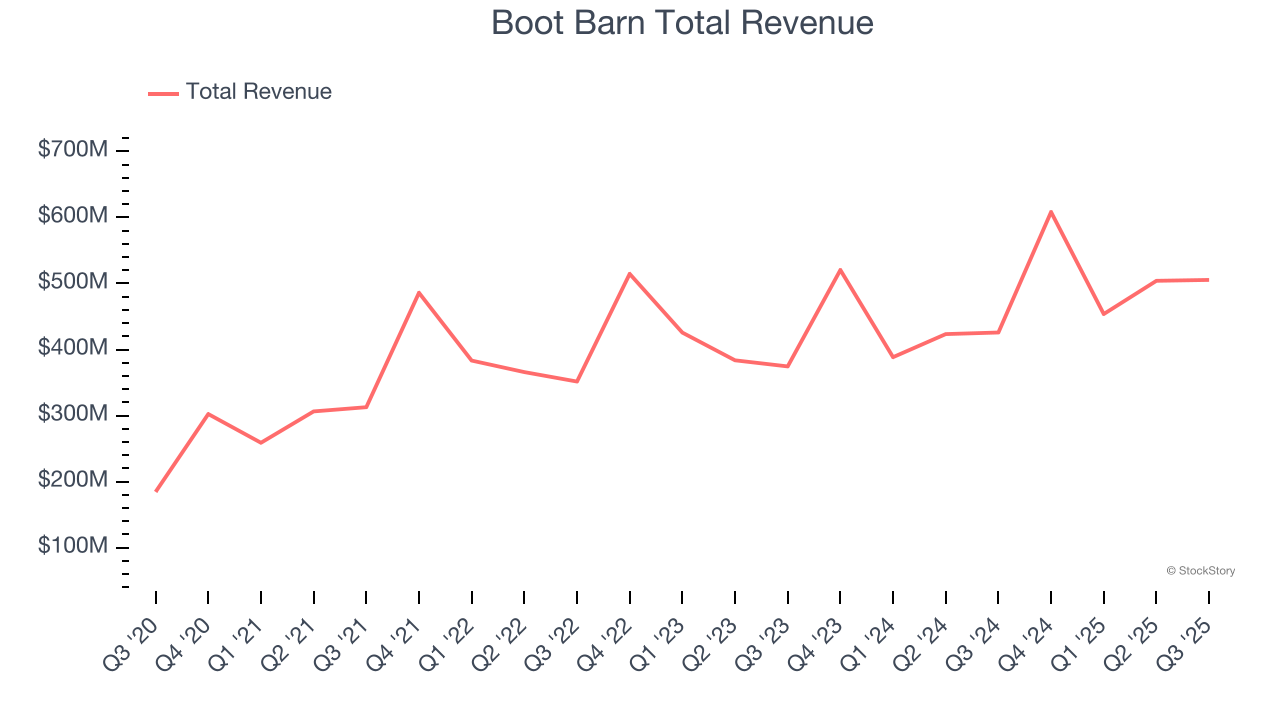

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE:BOOT) is a western-inspired apparel and footwear retailer.

Boot Barn reported revenues of $505.4 million, up 18.7% year on year. This print exceeded analysts’ expectations by 2.1%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ EBITDA estimates and full-year EPS guidance exceeding analysts’ expectations.

John Hazen, Chief Executive Officer, commented, "We delivered another strong quarter with high single-digit consolidated same-store sales growth and 19% total sales growth, demonstrating the continued resilience and broad appeal of our brand. This strength was evident across all major merchandise categories and geographies, with both our retail stores and e-commerce channels performing well. Importantly, we expanded our merchandise margin by 80 basis points, while maintaining disciplined expense control, which drove a 41% improvement in operating income and a 180 basis-point increase in operating margin to 11.2%. These results underscore the effectiveness of our strategic initiatives and our team's ability to execute in a dynamic retail environment.”

Boot Barn scored the fastest revenue growth but had the weakest full-year guidance update of the whole group. Unsurprisingly, the stock is up 2.7% since reporting and currently trades at $199.40.

Is now the time to buy Boot Barn? Access our full analysis of the earnings results here, it’s free.

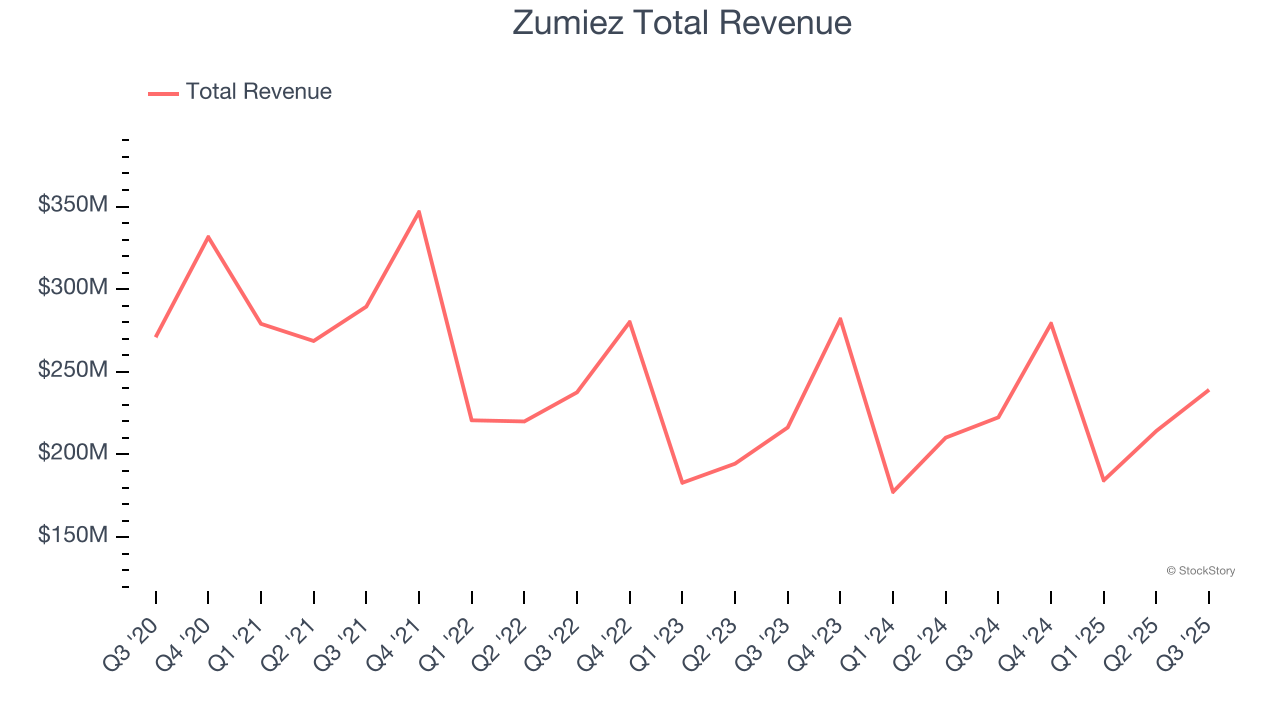

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ:ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Zumiez reported revenues of $239.1 million, up 7.5% year on year, outperforming analysts’ expectations by 2%. The business had an exceptional quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 7.3% since reporting. It currently trades at $25.28.

Is now the time to buy Zumiez? Access our full analysis of the earnings results here, it’s free.

Promoting a message of body positivity and inclusiveness, Torrid Holdings (NYSE:CURV) is a plus-size women’s apparel and accessories retailer.

Torrid reported revenues of $235.2 million, down 10.8% year on year, falling short of analysts’ expectations by 2%. It was a disappointing quarter as it posted full-year EBITDA guidance missing analysts’ expectations and a significant miss of analysts’ EBITDA estimates.

Torrid delivered the highest full-year guidance raise but had the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 4.2% since the results and currently trades at $1.23.

Read our full analysis of Torrid’s results here.

Founded as a purveyor of vintage items, Urban Outfitters (NASDAQ:URBN) now largely sells new apparel and accessories to teens and young adults seeking on-trend fashion.

Urban Outfitters reported revenues of $1.53 billion, up 12.3% year on year. This number topped analysts’ expectations by 2.6%. It was a very strong quarter as it also recorded an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ revenue estimates.

The stock is up 5.6% since reporting and currently trades at $72.11.

Read our full, actionable report on Urban Outfitters here, it’s free.

Founded as an outdoor and sporting brand, Abercrombie & Fitch (NYSE:ANF) evolved to become a specialty retailer that sells its own brand of fashionable clothing to young adults.

Abercrombie and Fitch reported revenues of $1.29 billion, up 6.8% year on year. This result beat analysts’ expectations by 0.9%. More broadly, it was a satisfactory quarter as it also produced full-year EPS guidance beating analysts’ expectations but EPS guidance for next quarter slightly missing analysts’ expectations.

The stock is up 51.7% since reporting and currently trades at $99.93.

Read our full, actionable report on Abercrombie and Fitch here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

| Jul-22 | |

| Jun-19 | |

| May-28 | |

| May-15 | |

| May-15 | |

| May-14 | |

| May-14 | |

| May-07 | |

| Apr-06 | |

| Apr-06 | |

| Apr-06 | |

| Mar-27 | |

| Mar-19 | |

| Mar-10 | |

| Mar-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite