|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Omnicell’s OMCL strength in its SaaS and Expert Services offerings should help sustain growth in the upcoming quarters. Efforts to expand into overseas markets instill optimism. However, adverse macroeconomic challenges and fierce rival pressure could hurt Omnicell’s performance.

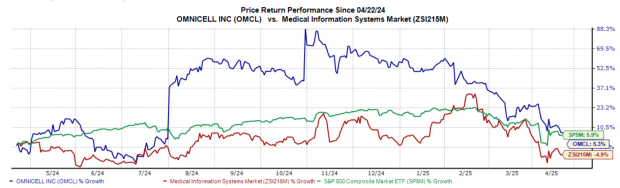

Currently carrying a Zacks Rank #3 (Hold), OMCL stock has delivered an impressive performance in the past year. Shares of the company have risen 5.3% against the industry's 4.9% decline. The S&P 500 composite has increased 5.9% in the said time frame.

The renowned healthcare technology company has a market capitalization of $1.39 billion. Omnicell’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 99.53%.

Robust Pipeline for SaaS and Expert Services Portfolio: Omnicell’s suite of SaaS and Expert Services includes a combination of robotics, smart devices, intelligent software and expert services. In recent years, Omnicell made key acquisitions such as Specialty Pharmacy Services (formerly ReCept), FDS Amplicare, and MarkeTouch Media, LLC to broaden their SaaS and Expert Services offerings. Omnicell also offers 340B solutions, which are related to the federal 340B Drug Pricing Program. By combining its 340B TPA (third-party administrator) services with Specialty Pharmacy Services, the company is creating growth opportunities for its customers.

In the fourth quarter, Omnicell launched OmniSphere, a next-generation, cloud-native software workflow engine and data platform intended to seamlessly integrate enterprise-wide robotics and smart devices. Earlier, in 2024, the company introduced Central Med Automation Service, a subscription-based solution for consolidated pharmacy services centers (CPSCs) and similar operations.

Within the segment, the EnlivenHealth brand is gaining momentum with cross-selling and upselling communication solutions to existing customers. Further, Central Pharmacy Dispensing Services continue to gain market traction, with several health systems choosing to automate their central pharmacy inventory and dispensing operations.

Planned Geographic Expansion: Another Upside: Outside the United States, healthcare providers are becoming increasingly aware of the benefits of automation. Additionally, there is a substantial demand for adherence packaging equipment outside the domestic market. The company’s international operations include its sales efforts centered in Canada, Europe, the Middle East, and the Asia-Pacific regions, and supply-chain efforts in Asia. Given the fact that the international market is less than 1% penetrated, with very few hospitals adopting medication control systems, Omnicell intends to expand into new markets, which it views as strategic.

Macroeconomic Challenges: The broader U.S. and global economies are facing elevated inflationary pressures, continued supply-chain disruptions, labor shortages and geopolitical instability. Simultaneously, OMCL is navigating the ongoing healthcare system capital budget and labor constraints, which have continued to affect its Point-of-Care product line. The challenging environment for some of the health system customers has also led to a 25.1% year-over-year decrease in the company’s fourth-quarter product revenues.

Competitive Landscape: Omnicell faces intense competition in the medication management and supply-chain solutions market. Even though it continues to gain market share from other providers, major competitors still pose threats as they spearhead several expansion programs. This increased competition could result in pricing pressure and a reduced margin, negatively impacting the company’s performance.

The Zacks Consensus Estimate for 2025 earnings per share has remained constant at $1.78 in the past 30 days.

The Zacks Consensus Estimate for 2025 revenues is pegged at $1.13 billion, suggesting a 1.5% rise from the year-ago reported number.

Some better-ranked stocks in the broader medical space are Masimo MASI, Boston Scientific BSX and Hims & Hers Health HIMS.

Masimo has an earnings yield of 3.4%, well ahead of the industry’s -3.2%. Its earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 14.4%. Its shares have risen 11.6% against the industry’s 10.5% decline in the past year.

MASI sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Boston Scientific, carrying a Zacks Rank #2 (Buy) at present, has an earnings yield of 3.1% compared with the industry’s 0.4%. Shares of the company have rallied 41% compared with the industry’s 6.4% growth. BSX’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 8.3%.

Hims & Hers Health, carrying a Zacks Rank #2 at present, has an earnings yield of 2.5% compared with the industry’s -6.8%. Shares of the company have rallied 118.7% compared with the industry’s 1.7% growth. HIMS’ earnings surpassed estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 40.4%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 26 min | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite