|

|

|

|

|||||

|

|

|

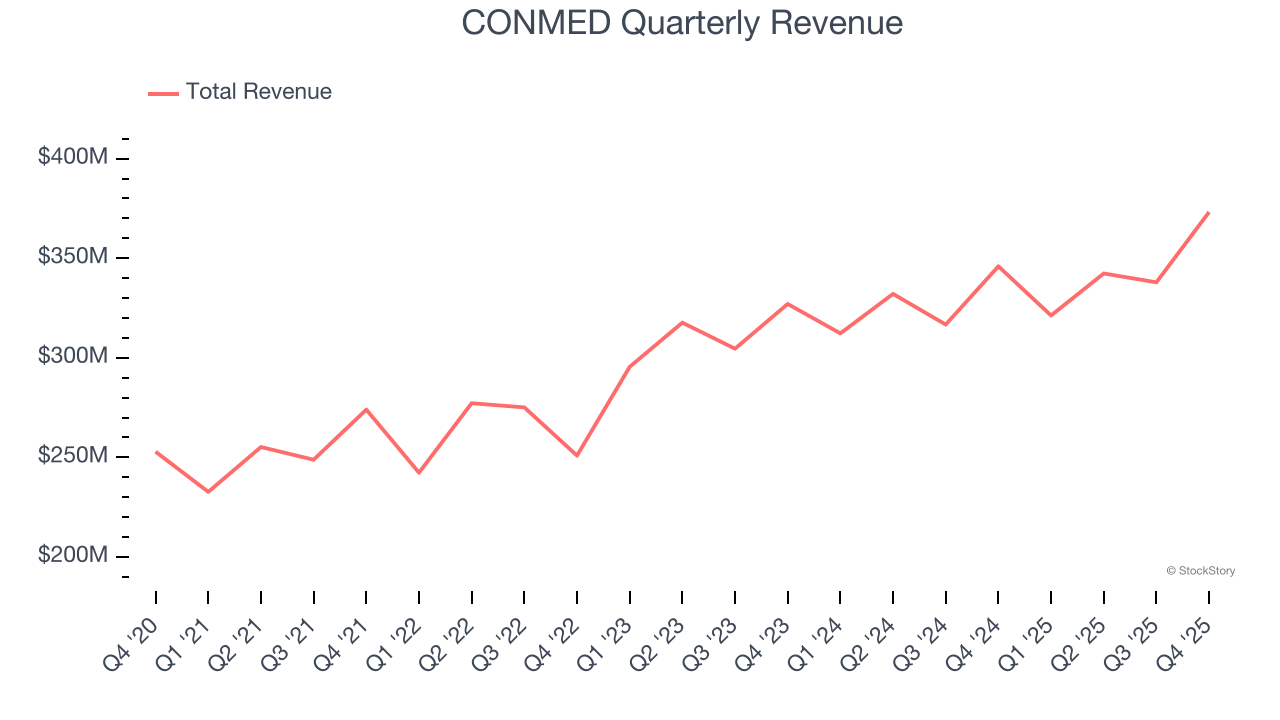

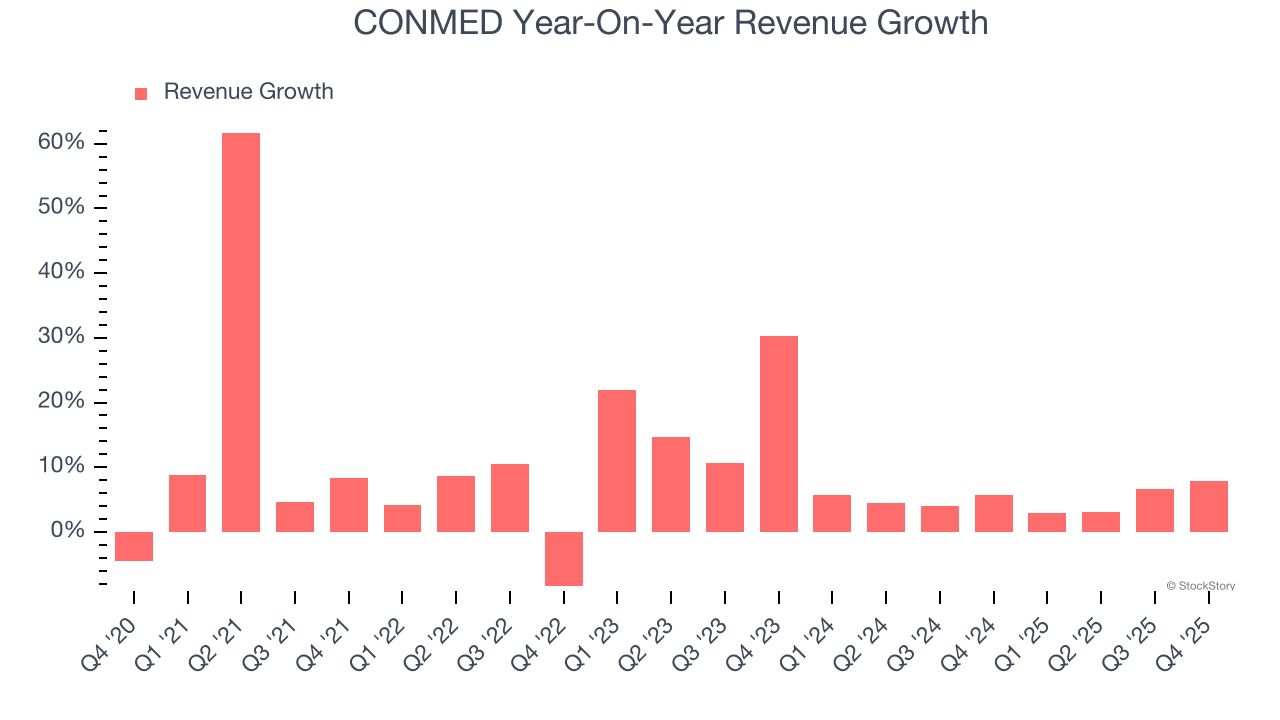

Medical tech company CONMED (NYSE:CNMD) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 7.9% year on year to $373.2 million. On the other hand, the company’s full-year revenue guidance of $1.36 billion at the midpoint came in 0.7% below analysts’ estimates. Its non-GAAP profit of $1.43 per share was 8% above analysts’ consensus estimates.

Is now the time to buy CONMED? Find out by accessing our full research report, it’s free.

With over five decades of experience in surgical innovation since its founding in 1970, CONMED (NYSE:CNMD) develops and manufactures medical devices and equipment for surgical procedures, specializing in orthopedic and general surgery products.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, CONMED’s 9.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. CONMED’s recent performance shows its demand has slowed as its annualized revenue growth of 5.1% over the last two years was below its five-year trend.

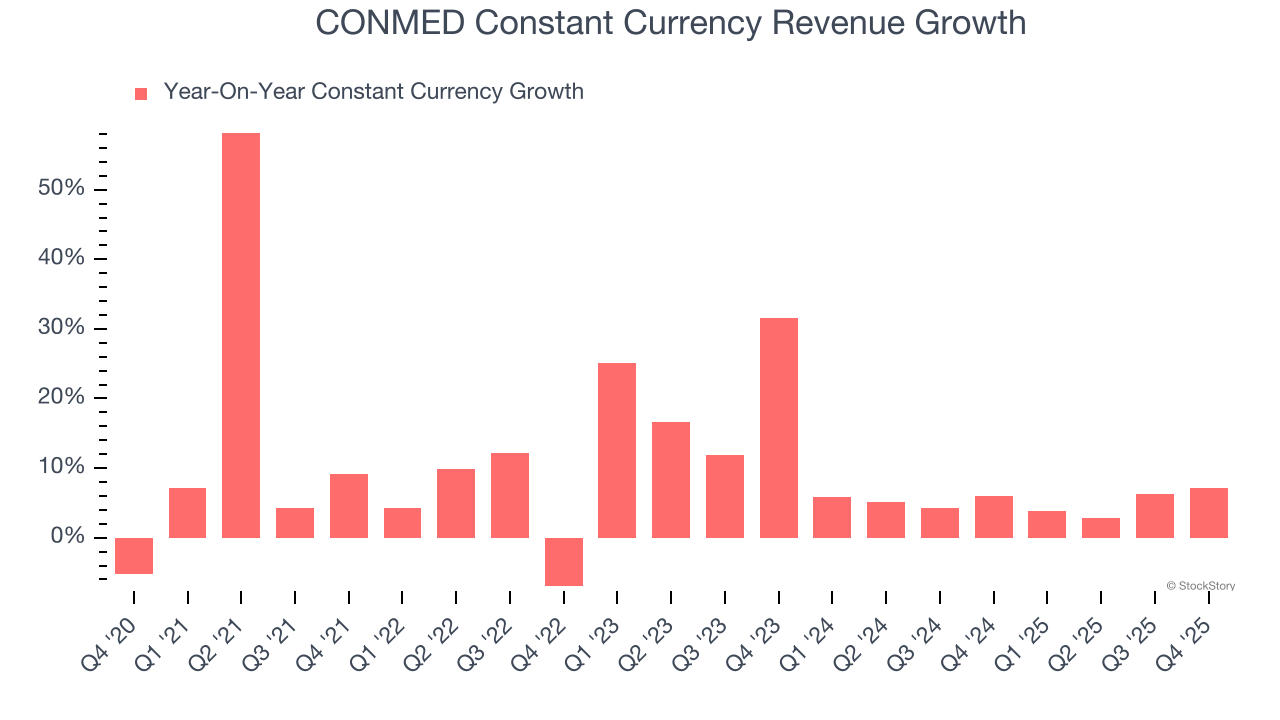

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.2% year-on-year growth. Because this number aligns with its normal revenue growth, we can see that CONMED has properly hedged its foreign currency exposure.

This quarter, CONMED reported year-on-year revenue growth of 7.9%, and its $373.2 million of revenue exceeded Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

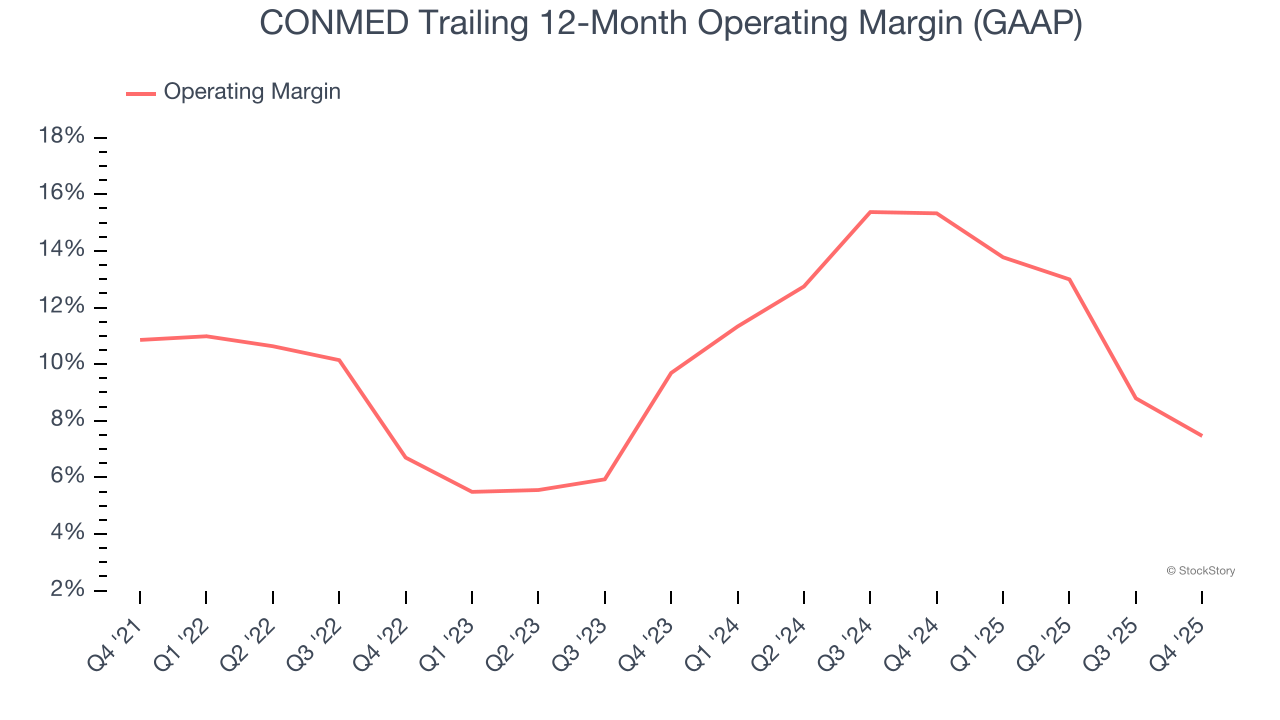

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

CONMED has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.1%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, CONMED’s operating margin decreased by 3.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, CONMED generated an operating margin profit margin of 9.8%, down 5.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

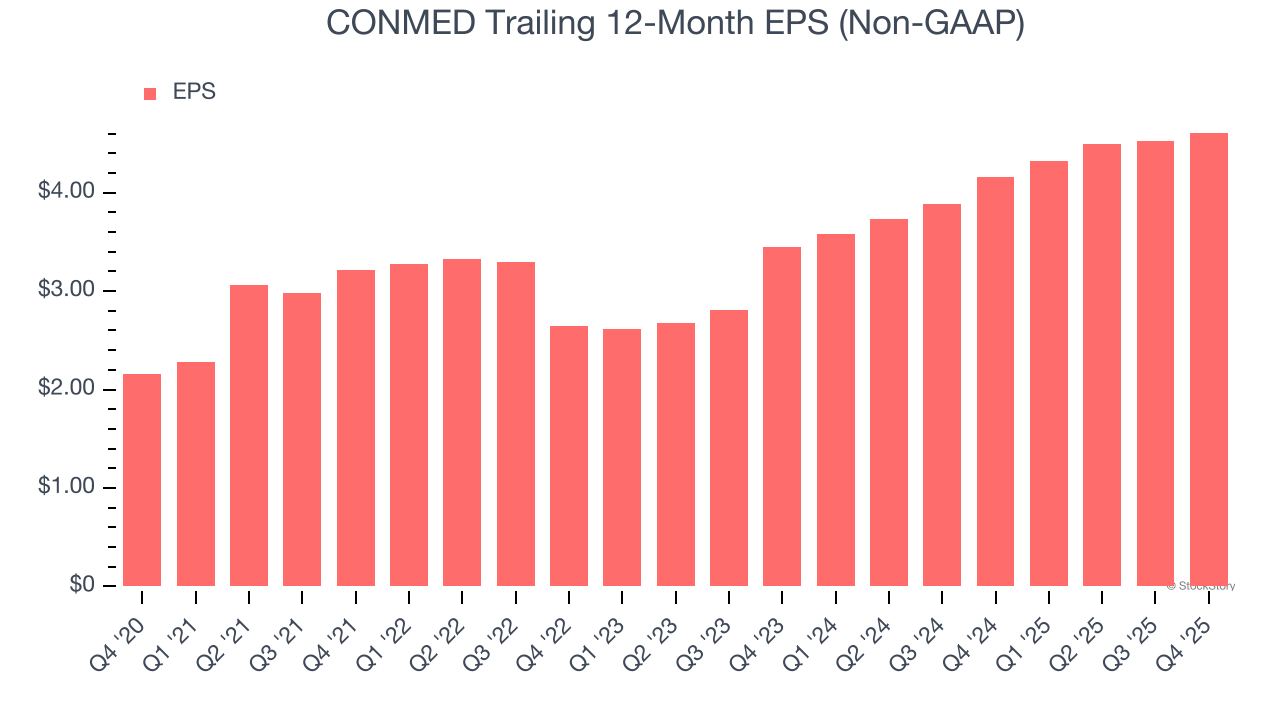

CONMED’s EPS grew at an astounding 16.4% compounded annual growth rate over the last five years, higher than its 9.8% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t improve and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q4, CONMED reported adjusted EPS of $1.43, up from $1.34 in the same quarter last year. This print beat analysts’ estimates by 8%. Over the next 12 months, Wall Street expects CONMED’s full-year EPS of $4.61 to shrink by 7.3%.

We enjoyed seeing CONMED beat analysts’ constant currency revenue expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock traded up 5.4% to $40.74 immediately following the results.

Big picture, is CONMED a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-29 | |

| Jul-29 | |

| Jul-22 | |

| Jul-20 | |

| Jul-13 | |

| Jul-13 | |

| Jul-10 | |

| Jul-02 | |

| Jun-17 | |

| May-20 | |

| Apr-30 | |

| Apr-30 | |

| Apr-29 | |

| Apr-29 | |

| Apr-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite